- News & InsightsWhich RA is most cost-effective?

Which RA is most cost-effective?

26 Jan, 2017

Patrick Cairns - Moneyweb

Investors are increasingly being made aware that the fees that they pay have a very meaningful impact on what they get out at the end.

In recent years a lot of talk about retirement funding has focused on cost. Investors are increasingly being made aware that the fees that they pay have a very meaningful impact on what they get out at the end.

This has become such an important issue that some providers are now able to promote themselves purely on the basis of what they charge. There has been something of a ‘race to the bottom’ in terms of who can offer the lowest fees.

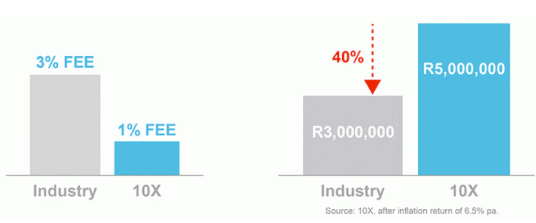

On its website, low-cost provider 10X makes a case for how important this is. Using the example of someone who saves R3 000 every month for 40 years into a retirement annuity (RA), and earns a return of 6.5% above inflation, 10X provides the following illustration:

In other words, just paying 2% more in fees when you are earning the same return can eat away almost half of your investment in 40 years.

It therefore makes sense for investors to be asking just how low fees can go. And how big a difference is there between the low cost providers and the rest?

The first important thing to note is that 10X is not exaggerating when it suggests that some investors could be paying 3% per annum on their RAs. In fact, in some cases they could even pay more than that. Some products offered by life insurance companies also charge layers of fees that are very difficult for investors to untangle.

However, a number of asset managers are now offering their own RA products in which the fees are much more transparent, and much lower. Thankfully the industry has also adopted the Effective Annual Cost (EAC) standard, which requires complete disclosure.

Using the EAC it is also possible to look across the industry and make direct comparisons between providers. Moneyweb has done this to compare what an investor would be paying if they chose to invest directly with a number of different providers – specifically those who are offering low cost options and two large active asset managers.

For the sake of the analysis, Moneyweb considered an investment amount of R500 000. In all cases, the underlying investment was placed in the RA provider’s own high equity Regulation 28-compliant portfolio and the latest available expense ratios were used.

The relative costs are displayed in the below tables and shown as an annual percentage of total assets invested. Providers don’t all report charges in the same way, so the terminology differs from one to the other, but the effective annual cost is what investors can expect to pay.

Note: 10X charges fees on a sliding scale depending on the amount invested. For amounts over R1 million the total charge would be 1.00% and for amounts over R5 million it falls to 0.82%.

*Note: Two options are provided for Sygnia, as the costs differ significantly depending on which underlying product the investor chooses. The unitised life fund includes a fund of hedge funds component that significantly increases the overall cost.

*

Note: When investing directly with Coronation, the investment management fee includes the administration fee. This would be expressed separately if investing via a LISP platform.

The lowest cost option is through Sygnia using its unit trust fund as the underlying investment. However, the other low cost options, including Sygnia’s unitised life fund, all come at similar cost.

10X is slightly cheaper than the rest at this level, and does become meaningfully cheaper when larger amounts are invested.

It’s also noteworthy that the products offered by Allan Gray and Coronation are not significantly more expensive. If an investor is looking to spread their RA between passive and active managers, they can therefore do so without paying exorbitant fees.

Share

- Facebook

- Twitter

- LinkedIn

- Email