Global markets whipsaw as Trump’s tariffs trigger unprecedented uncertainty

President Trump’s sweeping 2 April Liberation Day reciprocal tariffs triggered a global market rollercoaster and unprecedented backlash. The tariffs – ranging from 10% to 50% on most US trading partners, with some rates on China reaching as high as 125% – sparked immediate turmoil in global markets.

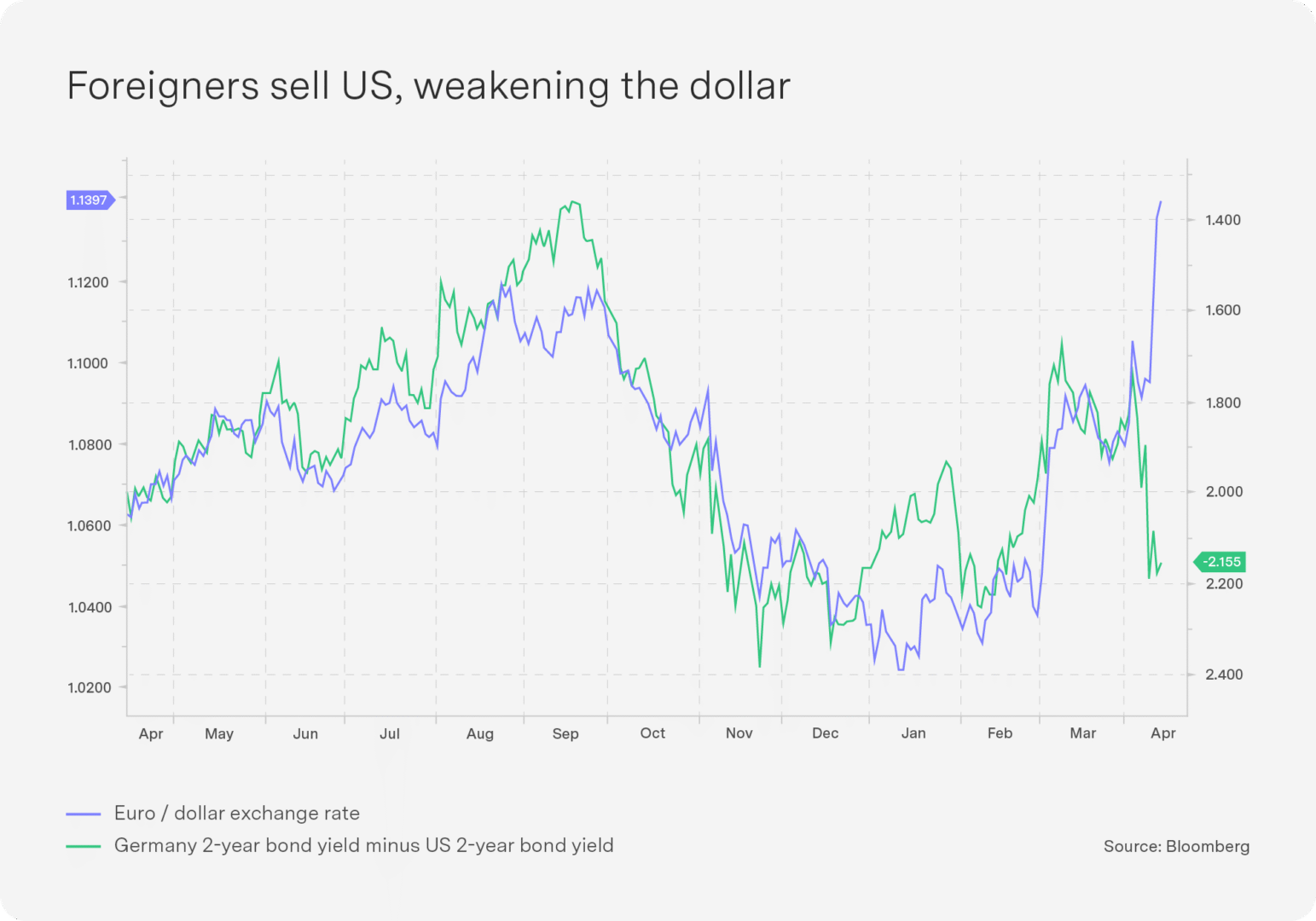

Only 13 hours after the 9 April implementation date , Trump suspended tariffs on nearly all countries but China. During this period, a flat 10% tariff is being applied to most imports, while counter-retaliatory tariffs on Chinese goods were hiked to 145% as the US-China trade war escalated. This “blink” announcement came after US stock markets suffered historic losses, US technology stocks fell more than 20% and $6.6 trillion was wiped out in two days. However, Trump’s blink appears most influenced by turmoil in the US bond market. Yields on 10-year Treasuries soared, marking the biggest three-day jump since 2001. Trump admitted he was watching the bond market closely and acknowledged investor anxiety: “People were getting a little bit yippy, a little bit afraid,” he said. The rapid spike in Treasury yields signalled a crisis of confidence. As investors – including Japanese private investors and foreign sovereign wealth funds such as China’s – sold US bonds, the cost of US government borrowing soared. Combined with outflows to European assets, this bond sell-off forced the dollar to weaken out of line with bond differentials (see chart).

The blink also triggered a sharp rebound, however, with the Dow Jones surging by 2 000 points within minutes. More than 50 countries are now in trade talks with the US, but the administration’s tariff approach – described as a “crime against economics” – has made consensus elusive. There has been positive news on trade deals with Japan, Korea and India but mixed messages on China and the European Union (EU). The EU has threatened its own strong countermeasures, including digital taxes on US tech giants if negotiations fail. A retreat to 60% tariffs on China and the current 10% universal tariff is already estimated to slow global GDP by 0.7%.

Even with the bounce after the pause, the S&P 500 had its worst run during a president’s first 100 days since Gerald Ford took office in 1974 after Richard Nixon’s resignation. The White House’s shifting stance and reliance on executive orders under emergency powers, bypassing Congress, have undermined confidence in US markets, and the long-term consequences of this episode are likely to reverberate well beyond the current 90-day pause.

What does the Trump tariff tantrum mean for South Africa?

On 2 April, US President Donald Trump announced a series of tariff increases the US intended to impose on 60 countries across the global economy. In one speech, he changed the global trading system of low tariffs and free trade that had existed for over 70 years. The initial announcement was a base tariff rate of 10% on all economies, with additional “reciprocal” tariff hikes ranging from 11% to 50% for many US trading partners. This has morphed into a tariff war between China and the US – their current tariff rates on each other’s products are 125% and 145% respectively. A series of exemptions was provisionally applied to some exports into the US, most notably for microelectronics components.

Trump has also allowed a 90-day reprieve so that bilateral negotiations can take place.

To understand the effect of the tariff hikes on South Africa’s economy, it is first necessary to understand the size and shape of our trade relations with the US. South Africa exported $13 billion worth of goods to the US in 2023 – about 3.64% of our GDP. To put that in perspective, South Africa’s total exports to the rest of the world makes up 33% of our GDP. Our exports to the US account for about 7% of total exports, making the US our second-largest trading partner after China. Trump is particularly fixated on those economies that run trade surpluses with the US. South Africa’s is over $8 billion, meaning we export more than we import from the US. This appears to be at the core of Trump’s negotiation strategy with South Africa, and his administration is focused on exacting concessions for specific US products to increase their market access in South Africa. While South Africa’s membership in the African Growth and Opportunity Act (AGOA) gives us preferential access to the US market, our AGOA exports constitute about 20% of our total exports to the US. Thus, most of SA’s exports to the US are not AGOA-related.

Under Trump’s 90-day reprieve, South Africa is tariff-exempt on platinum, gold, chrome, copper, manganese and aluminium. Rough calculations suggest that 49% of all South African exports to the US will be exempt, a significant reprieve for our existing trade relations with the US. It does, however, put a spotlight on those products in the remaining 51% of our export basket, where the automobile industry and agricultural exports are likely to be hit by higher tariffs. It is thus the impact of tariffs on these industries that should be the focus of our discussion and policy response.

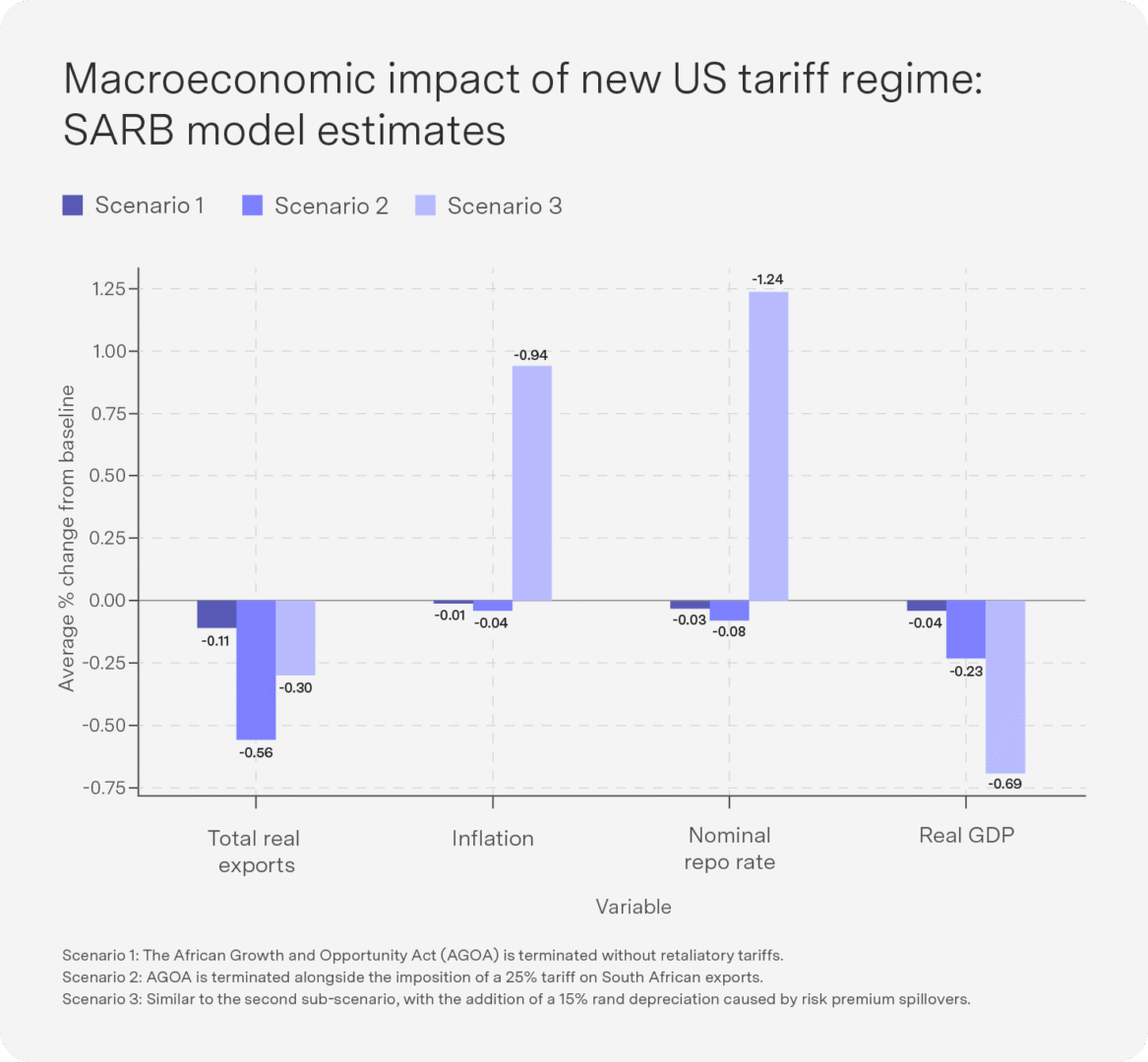

The macro model (see chart) shows the South African Reserve Bank’s (SARB) latest Monetary Policy Review estimates. Using the assumption of the cancellation of AGOA and a 25% tariff adjustment (Scenario 2) suggests a decline in exports by 0.56%, deflation of 0.04%, a nominal repo rate reduction of 0.08% and a drop in real GDP by 0.23 percentage points. Under this model, a projected 1.8% growth rate for 2025 declines to 1.57%. While this may not seem like a large drop, it would be significant given South Africa’s already anaemic growth rates. It is interesting to note, however, that deflation and a repo rate decline further from baseline are also likely outcomes.

A quick analytical sidebar: Politicians run the risk of losing an election if they focus only on national and macro trends and ignore sub-national trends.

For example, if poverty levels decline nationally, specific regions or sub-groups may nevertheless experience an increase in poverty – an election could be lost by ignoring these sub-national trends. As a country, we run the risk of ignoring the sector-specific outcomes of the new tariff regime. I am particularly concerned about the automobile and agriculture sectors, where economic strife may unfold in specific regions or smaller towns – such as the Eastern Cape auto corridor and the small citrus towns of the Western Cape.

In trying to obviate these potential real economic losses, policymakers must get ahead of the curve. To do so, they must assist affected companies to access foreign markets outside of the US – in particular those that have not been traditional export markets. The Middle East and Asia are obvious examples for South African agricultural exports. Furthermore, state support directed at ensuring the tariff hikes are buffered in some way – through supply-side support measures, for example – must be carefully planned and targeted to benefit those exporters that need it most. The hard work of protecting our exports must now begin in earnest!

Top-performing Sygnia funds

1-month absolute performance as at 29 April 2025

- Sygnia Itrix FANG.AI Actively Managed ETF 6.7%

- Sygnia FANG.AI Equity Fund 5.7%

- Sygnia Itrix MSCI Japan ETF 5.7%

- Sygnia Itrix Eurostoxx50 ETF 5.1%

- Sygnia Listed Property Index Fund 4.9%

The FANG.AI funds were the top performer during the month of April, showing the resilience of these global companies despite the turmoil in the US. European and Japanese equities are both in the top five as investors continue to worry about the conflict between the US and China.

South African assets dominate the top five positions over 12 months, though Berkshire Hathaway has shown incredible performance at the top despite the weak dollar and US markets, showcasing the company’s resilience and diversification.

12-month absolute performance as at 29 April 2025

- Sygnia Life Berkshire Hathaway Portfolio 31.2%

- Sygnia Listed Property Index Fund 26.2%

- Sygnia Itrix Top 40 ETF 25.4%

- Sygnia Itrix FANG.AI Actively Managed ETF 22.0%

- Sygnia Top 40 Index Fund 21.8%

US: Strong momentum will delay a recession, but exceptionalism is waning

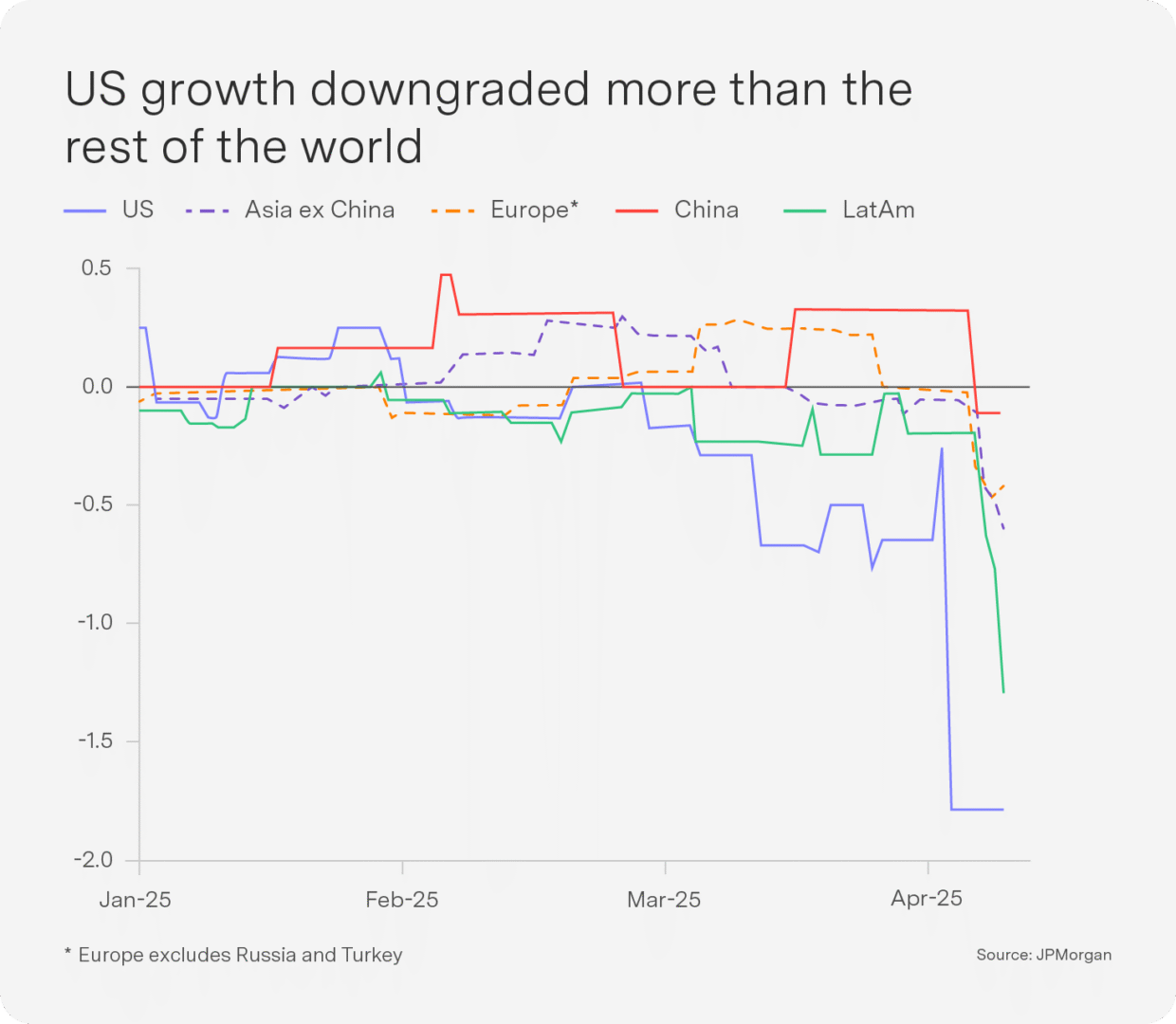

The US economy entered 2025 with solid momentum, buoyed by robust service sector activity – accounting for over 75% of economic output – that provided a buffer against shocks. However, escalating trade wars and new tariffs are shifting the outlook toward a pronounced slowdown. Recent forecasts show that US growth is set to slow sharply in 2025 – more sharply than in the rest of the world (see chart). The latest round of tariffs, including retaliation from trade partners, is expected to knock around 1.5% off US growth, leaving the US economy expanding at just above 1%. While a full-blown recession is not the base case, the risk is clearly rising.

The US is worst hit by its own policies because over two-thirds of US manufacturing firms are also importers, making them especially vulnerable to higher input costs on the back of tariffs. Supply chains will take years to realign, and businesses already face profit-margin compression. Concerns about weak sales are rising, which often signals an impending softening in the labour market. US policies that restrict companies’ ability to produce or sell abroad are also weighing on corporate profitability.

Some of the tariff-related costs will be passed on to consumers, keeping inflation higher for longer and limiting the Federal Reserve’s ability to cut rates on an absolute basis and relative to the rest of the world. The Fed chair has warned that the tariffs are “significantly larger than anticipated”, likely to result in higher inflation and slower growth. Trump’s public criticism of the Fed for not cutting rates added to market unease.

The US dollar has fallen to a three-year low against major trading partners, reflecting both weaker growth prospects and higher policy uncertainty and, ultimately, the erosion of US economic exceptionalism

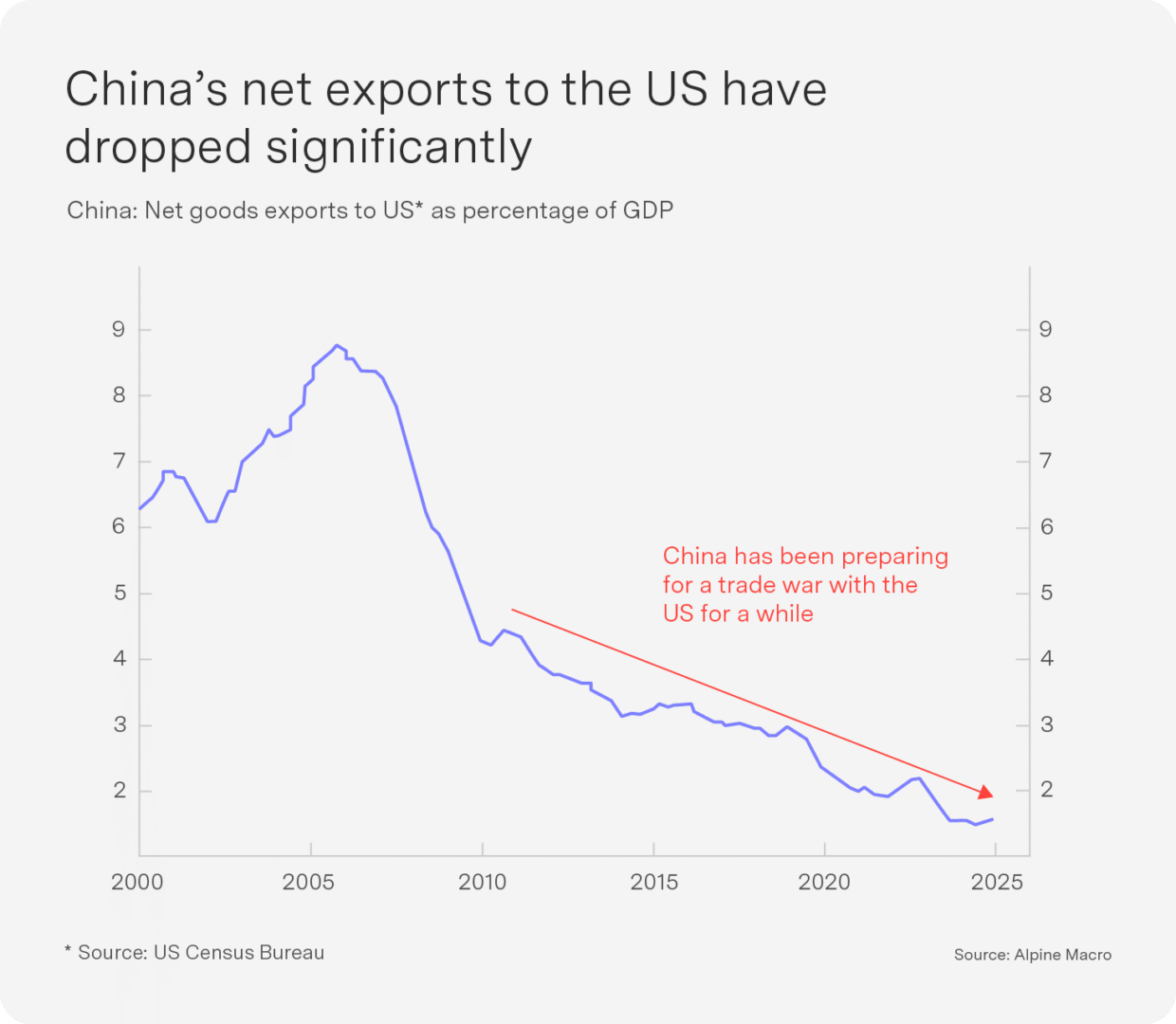

China: Emboldened to hold firm against the US

Beijing regards Trump’s tariff escalation as being more detrimental to the US economy than to its own and is prepared to continue its aggressive countermeasures, including selling US Treasury bonds. Key points underpinning China’s confidence include:

- China’s net exports to the US have fallen from 9% of its GDP twenty years ago to 1.6% now (see chart), a loss that can be offset through fiscal stimulus measures.

- A significant portion of China’s exports to the US, such as rare earth minerals critical for technology manufacturing, have no easy substitutes, giving China powerful leverage.

- China can deploy non-tariff measures such as anti-foreign sanctions and the blacklisting of US companies.

- Chinese stocks have relatively low exposure to overseas revenue (around 15–16%) compared to other major markets, insulating them from global trade shocks.

- Over one-third of Chinese sales to the US are from companies partially owned by American firms.

- Chinese businesses have direct or indirect control of 70% of global supply chains by industry category or product lines.

- While the US pushes other countries toward bilateral trade agreements, China is strengthening its ties with other countries and the EU.

China has raised tariffs on US goods to 125%, while US tariffs on Chinese imports are now at 145%. China’s official statements condemn US tariffs as unilateral coercion that violates international trade rules, while Beijing’s “never yield” stance signals readiness to sustain the trade conflict.

China remains open to negotiations but expects a willingness to address Chinese concerns, especially regarding American sanctions and Taiwan.

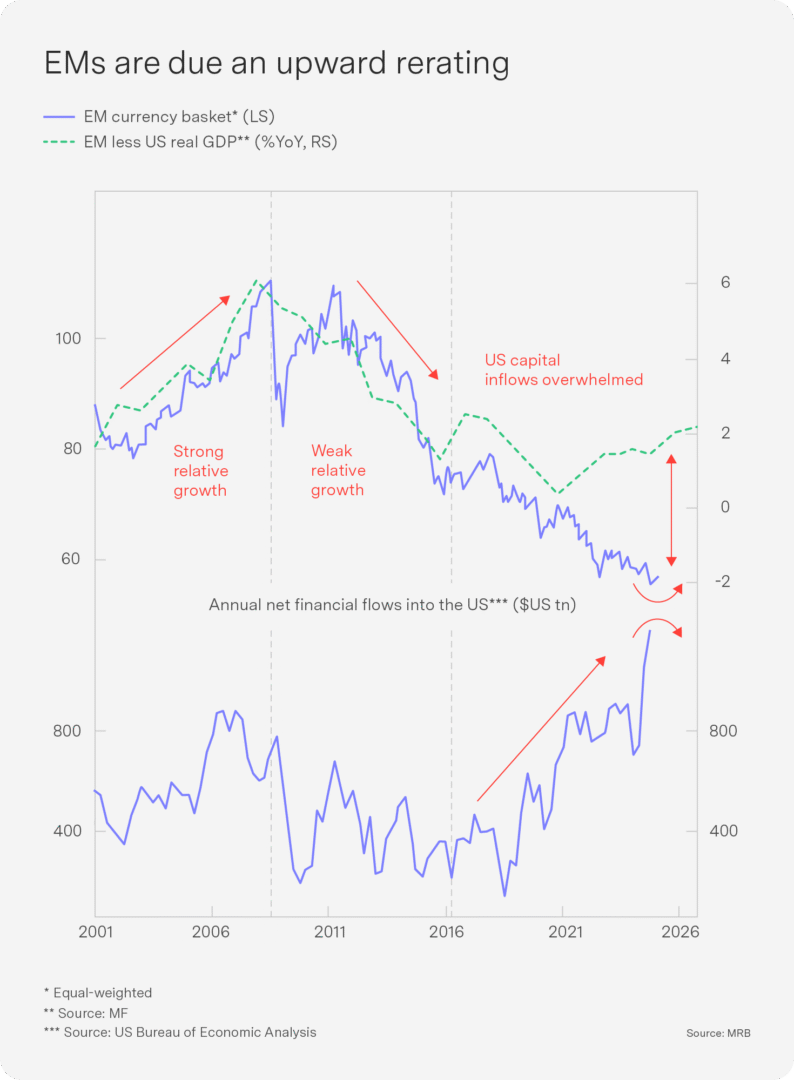

Emerging markets relatively cushioned by policy

Several factors are supporting emerging market (EM) resilience amid the global economic uncertainty:

- EM GDP growth has kept pace with the US over the past decade, though EM currencies have generally underperformed, acting as a future cushion for EM investors against shocks (see chart).

- As US growth forecasts are revised lower, EMs are expected to experience relatively stronger growth. EMs (excluding China) are forecast to grow at about 4.3% for 2025, outpacing advanced economies.

- EMs generally have more policy flexibility, with many central banks having already tightened and inflation falling, making it possible to support growth with lower policy rates if necessary.

Unless the US enters a recession, which is not the base case, relative growth and capital flows should remain positive for EMs. We have increased our exposure to EMs at the expense of the US.

Outlook: Remain cautious

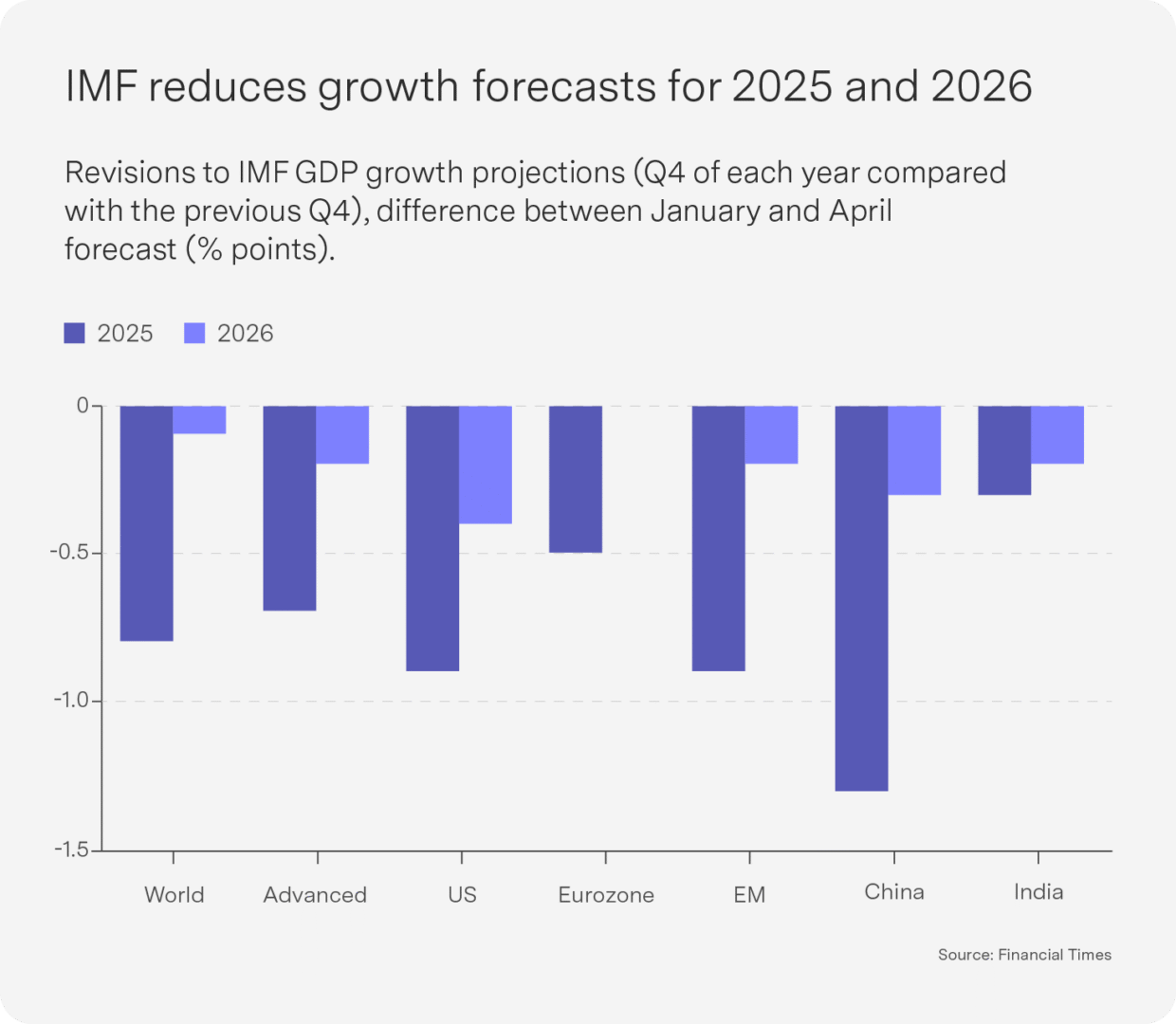

The International Monetary Fund cut its projection for global growth (see chart) this year by 0.5% to 2.8%, making it the slowest expansion since Covid-19 and the second-worst figure since 2009; however, 2026 was only downgraded by 30 bps. The latest economic data remain strong and show no signs of global recession. In the short term, several factors support ongoing economic momentum:

- Companies are accelerating shipments to get ahead of potential tariff hikes, temporarily boosting trade volumes and economic activity.

- US households have strong balance sheets, supporting spending and demand.

- The banking sector remains sound, with no liquidity issues; excesses were largely worked off during the 2022 mini-recession.

- Fiscal policy is set to become more supportive in the US, Germany and China, adding further economic resilience. This is likely to weigh on the dollar.

- Falling energy prices are helping offset some of the inflationary impact from tariffs.

But this is backward-looking: the future hinges almost entirely on the outcome of tariff negotiations in the hands of one man, President Trump. Despite total US-China trade peaking in 2022, it still approaches $700 billion annually, making this trade relationship globally significant and ensuring that tariff talks will continue to dominate the economic outlook.

There should be little political appetite for draconian new tariffs after the current 90-day reprieve. Trump’s disapproval rating among independents has soared to 56%, and he cannot afford to trigger a recession or a market crash ahead of the 2026 midterms, which would likely result in heavy Republican losses and leave him politically exposed. That said, forecasting Trump’s actions is near impossible, and the risk of damaging protectionism remains elevated. If a swift resolution to the tariff war is not reached, the current economic momentum will dissipate rapidly.

Even if a resolution is found, Q2 growth will slow as the global trade front-running tariffs comes to an end. Bookings for shipping containers from China to the US are down 45% in April year-on-year, and the effects of a slowdown in investment and hiring due to the current uncertainty will become evident shortly. While the year may end higher, we expect a soft patch in the middle. We have further reduced exposure to equities and remain cautious.

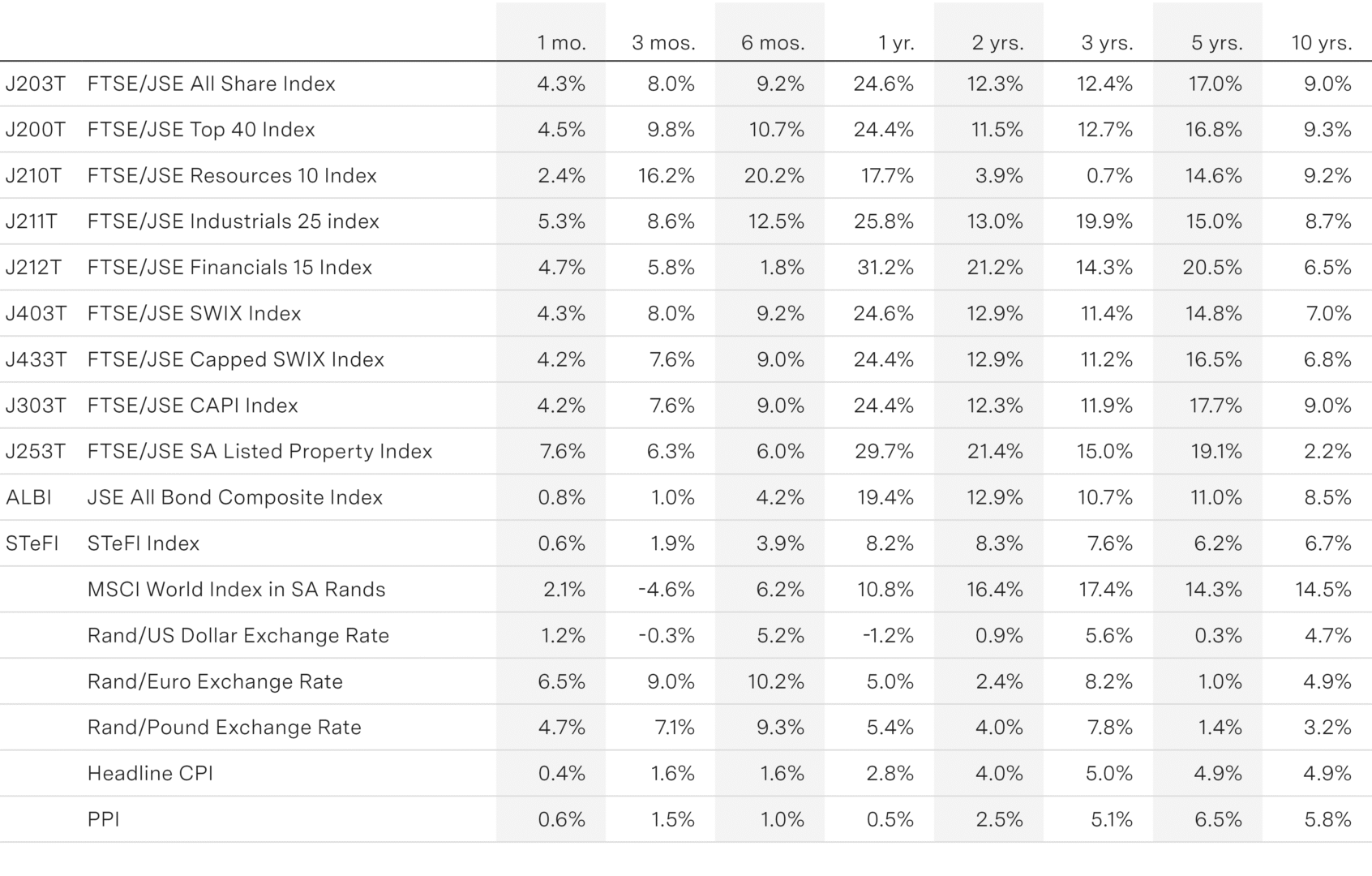

Key indicators