AI adoption expanding and SpaceX reveals plans for biggest ever IPO

Technology stocks drove markets in May, with the Nasdaq reaching new highs. Strong demand for AI infrastructure pushed up semiconductor stocks, while initial public offering (IPO) filings from SpaceX as well as OpenAI’s pre-IPO preparations added further momentum, with space and satellite stocks soaring. Despite its expected market valuation of $1.75tn–$2tn, which would make it the eighth- or ninth-largest US company, SpaceX’s weight on entering the S&P 500 is projected at only 0.5%–0.75%, because index weight is determined by public float, not by total market cap alone. The S&P 500 normally requires 12 months of public trading before a new listing is eligible for inclusion – for SpaceX, however, this seasoning period is being reduced to six months. The Nasdaq has gone further still, amending its inclusion rules to require as little as 15 days of trading, with float eligibility extended to up to three times the standard free float, which would significantly accelerate SpaceX’s index inclusion.

AI infrastructure demand appears real rather than speculative. The combined cloud backlog of Amazon, Microsoft and Google has doubled over six months to $1.5 trillion in sales commitments (not pipeline). That said, the speed and scale of investment warrant close scrutiny, with AI hyperscaler capex expected to rise from $800bn in 2026 to $1.1tn in 2027. At this trajectory, next year’s increase could approach the telecom extremes of the late 1990s, when capex absorbed nearly all operating cash flow. With the cost of building required AI data centres estimated at over $3tn, hyperscalers are increasingly turning to debt markets. Google is now the eighth-largest bond issuer in Europe, and others are expected to follow. Despite Magnificent Seven earnings growth outpacing the rest of the S&P 500 in Q1 2026, with earnings-per-share growth at its strongest level in two years, the group has de-rated meaningfully to 10-year valuation lows. This low rating reflects market concerns about future depreciation from the heavy capex cycle.

Our primary reason for downweighting emerging markets (EMs) to neutral is macro vulnerability, principally from exposure to higher oil prices. A new concern has since emerged, however: extreme concentration in recent EM relative returns. The entirety of EM outperformance since early September is attributable to just three AI-infrastructure-linked stocks: TSMC in Taiwan and Samsung and SK Hynix in Korea. Valuations here are a serious warning sign. Taiwan’s market capitalisation now exceeds China’s, despite its economy being less than 5% the size. We maintain a neutral EM stance and, for AI exposure, favour the broader AI opportunity set available through US markets.

Fuelling the fire: What the oil price shock means for South Africa

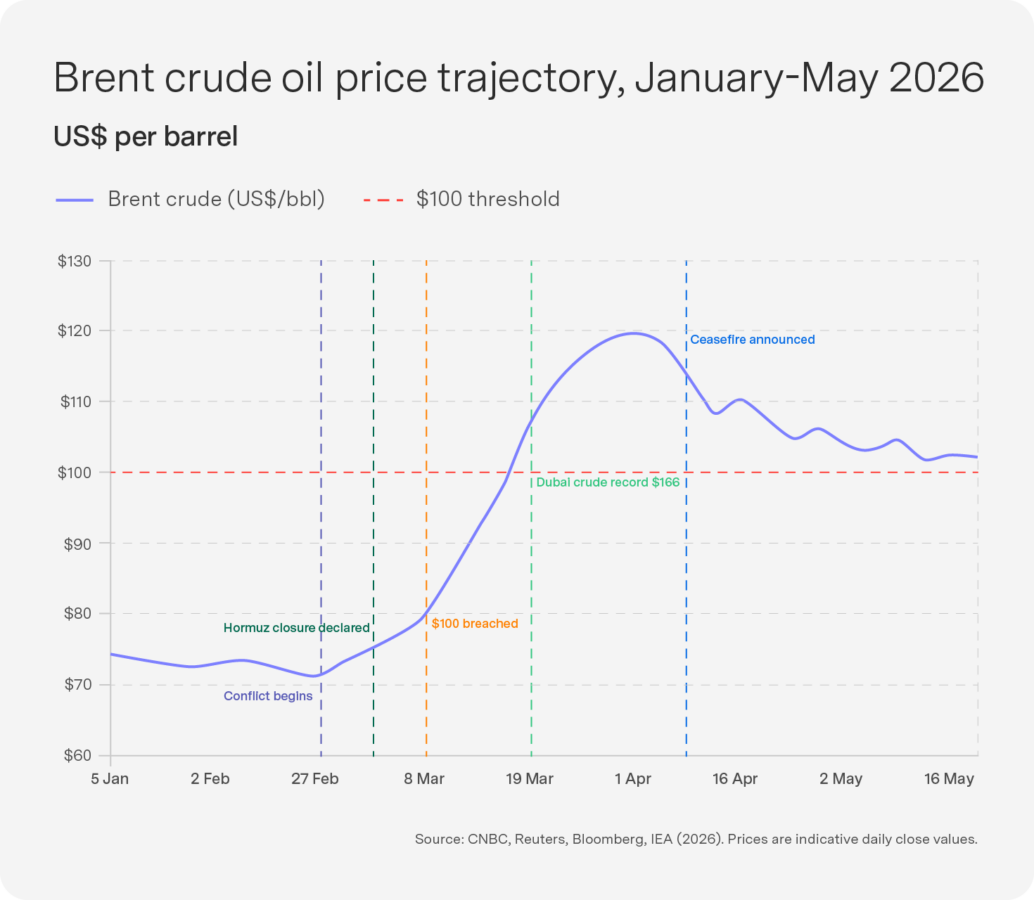

On 28 February 2026, the US and Israel launched coordinated strikes against Iran. Iran retaliated and, on 4 March, declared the Strait of Hormuz – through which approximately 25% of the world’s seaborne oil trade passes – closed to commercial traffic. The price response was immediate and historically extreme. Brent crude oil jumped from $71 per barrel on 27 February to nearly $120 at its peak, a surge of over 55% in a matter of weeks. March alone recorded a 51% monthly gain, one of the largest single-month oil price increases ever recorded. Tanker traffic through the Strait dropped 70% almost overnight. A ceasefire was announced on 8 April, but the Strait has remained functionally disrupted for weeks. As of writing, Brent has settled in the $100–$105 range, permanently elevated relative to pre-war levels.

For South Africa, this hike in oil prices has had a strong and almost instantaneous impact on the domestic economy. Why? First, because South Africa imports virtually all its crude oil, making us one of the most oil-dependent economies in the developing world. Oil accounts for roughly 21% of our total primary energy supply, with transport consuming 61% of all petroleum products. Secondly, our fuel price is set monthly on an import-parity basis – meaning domestic prices track Brent crude and the rand/dollar exchange rate almost mechanically. The Middle East (and Nigeria) have historically supplied the bulk of our crude. When Middle Eastern supply is disrupted, we feel it almost immediately – as we did in May with brutal clarity.

The shock effectively hits through two primary channels. First, through firms and their production costs, where diesel is the fuel of commerce, powering everything from freight trucks and construction equipment to agricultural machinery and generators. The more than R6.00 per litre increase in diesel effective 6 May, taking it to over R30/l, was a seismic input cost event. Sectors most exposed include mining, agriculture, logistics and retail – with many in our low-growth environment already operating on thin margins. With 80% of goods moved by road, these costs pass through to the shelf within weeks.

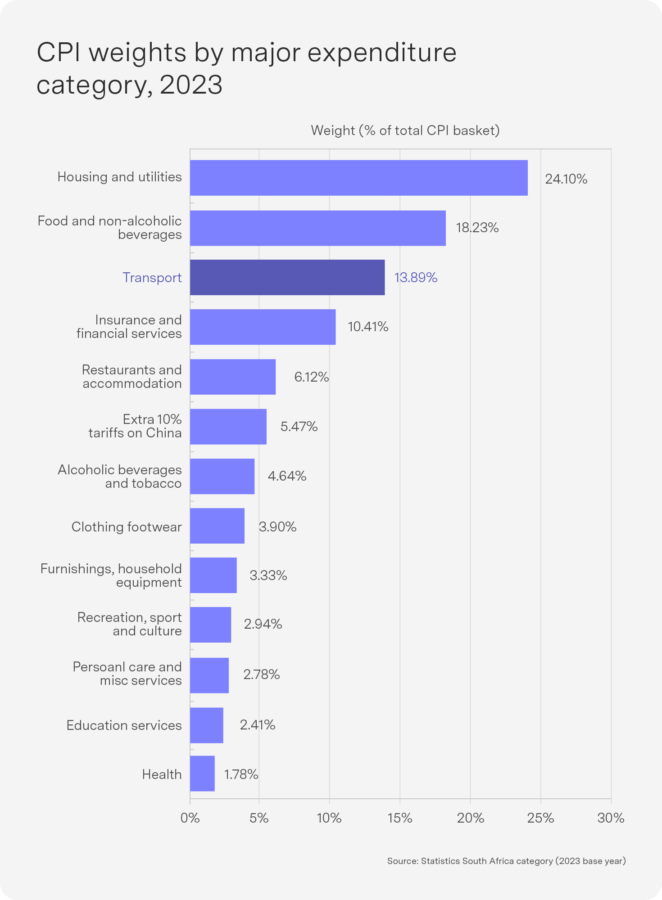

The second channel of impact of the oil price hike is households. The proportion of income spent by South African households on transport is some of the highest in the developing world. Data show that the average household commits 14% of its expenditure to transport – one of the four largest household spending categories in South Africa. A notable legacy of spatial apartheid, this average contribution understates the burden on lower-income households, who commute by taxi and bus and spend a disproportionately higher share of their income on transport. With petrol at R26.52 per litre and diesel at R32.09, real household disposable income is being directly eroded. Importantly, without the government’s emergency R3 per litre levy relief – at a fiscal cost of roughly R6 billion per month – final fuel prices would be materially higher still.

The evidence for the fuel price’s pass-through effect is historically consistent: Petrol price increases in South Africa feed through directly to non-fuel consumer prices and then to economic growth. The modelling evidence suggests that a 1% fuel price increase reduces South African economic output by approximately 0.38% in the short term. Applied to a 25% fuel price shock, the implied drag on GDP is close to 1 percentage point – which is of course material for an economy already projected to grow at only 1.6% in 2026. The concomitant impacts of lower growth rates on employment are self-evident.

So while the South African Reserve Bank (SARB) entered 2026 in arguably its best position in two decades, with inflation exactly on the new 3% target in February; the repo rate cut by 150 basis points since September 2024 to 6.75%; and further cuts widely expected, the Iran war has reversed this trajectory. The SARB’s March 2026 Monetary Policy Committee (MPC) statement projected headline inflation accelerating to around 4% in Q2 2026. Markets have shifted from pricing in two cuts to pricing in up to two 25-basis-point hikes by the end of 2026. The May MPC meeting, scheduled for 28 May, is crucial: The fuel pass-through from the 6 May price adjustment is expected to push CPI to approximately 4.2% – above SARB’s recently set 2%–4% inflation target. SARB thus faces a textbook supply-shock dilemma for which the response, given SARB’s inflation sensitivity, is likely to be highly cautionary.

South Africa entered 2026 with genuine momentum: A primary fiscal surplus, the new 3% inflation target credibly anchored, a credit rating upgrade and the end of load shedding, with structural reforms visibly progressing. Now, though, our growth projections for 2026 hang in the balance and depend on how long the regional supply disruption lasts – or how quickly an agreement between Iran and the US can be struck. Under a ceasefire-holds scenario, Brent is likely to settle in the $80–$90 range, with inflation peaking around 4% to 4.5%. In this scenario, one SARB hike is possible, with growth revised down to around 1.0%–1.2% but the recovery trajectory surviving into 2027. Under a prolonged-conflict scenario and sustained $100+ oil, multiple rate hikes will follow, GDP could fall below 1% and we will back onto a long road to recovery. South Africa’s hard-won macroeconomic gains now depend on events entirely beyond our control. The fuel price hike has not yet definitively spoilt the growth recovery, but it has put it in serious jeopardy. Peace cannot come soon enough.

Ultimately, our research suggests that the JSE’s delisting challenge is not a single phenomenon with a single cause but is the compounded outcome of firm-level fragility, macroeconomic instability, regulatory cost accumulation and structural shifts in how capital is allocated both domestically and globally. Most troublingly, the JSE appears to be losing precisely the kinds of firms – smaller, younger, innovation-oriented – that in other economies are the engines of job creation, technological upgrading and long-term productivity growth.

Top-performing Sygnia funds

Technology stocks continued to dominate in May on the back of strong earnings revisions, semi-conductor shortages and listing hype. This drove 4th IR, FANG and EM into the top spots for the month. Over 12 months, South African stocks have continued to dominate across equity markets and property markets due to their very strong run before the Iran war.

1-month absolute performance as at 28 May 2026

- Sygnia Itrix MSCI Emerging Markets 50 ETF 11.5%

- Sygnia Itrix FANG.AI Actively Managed ETF 8.4%

- Sygnia FANG.AI Equity Fund 6.9%

- Sygnia Itrix 4th Industrial Revolution Global Equity Actively Managed ETF 5.0%

- Sygnia 4th Industrial Revolution Global Equity Fund 4.8%

12-month absolute performance as at 28 May 2026

- Sygnia Itrix MSCI Emerging Markets 50 ETF 65.0%

- Sygnia Itrix Top 40 ETF 27.5%

- Sygnia Transnational Equities Fund 27.3%

- Sygnia Top 40 Index Fund 26.6%

- Sygnia Itrix 4th Industrial Revolution Global Equity Actively Managed ETF 25.1%

United States: Consumers running on fumes, inflation reviving

The US economy got off to a strong start in 2026 as a record $316 billion in tax refunds and an accelerating capex cycle boosted growth and corporate profits in the first quarter. The labour market has also held up better than feared, with April non-farm payrolls coming in well above expectations.

The problem is inflation: producer prices rose 6% year-on-year in April, the fastest pace since 2022 and above every estimate in Bloomberg’s economist survey. Consumer prices followed, with headline CPI rising 3.8% year-on-year (estimate: 3.7%). One-, two- and five-year CPI swaps have returned to the levels reached after President Trump’s “Liberation Day” tariff announcements last year. Stripping out the war’s direct price impact, the underlying inflation trend is already rising and broad-based, with every major category contributing. Bond markets reacted sharply, and US 30-year Treasury yields broke above 5% for the first time since 2007.

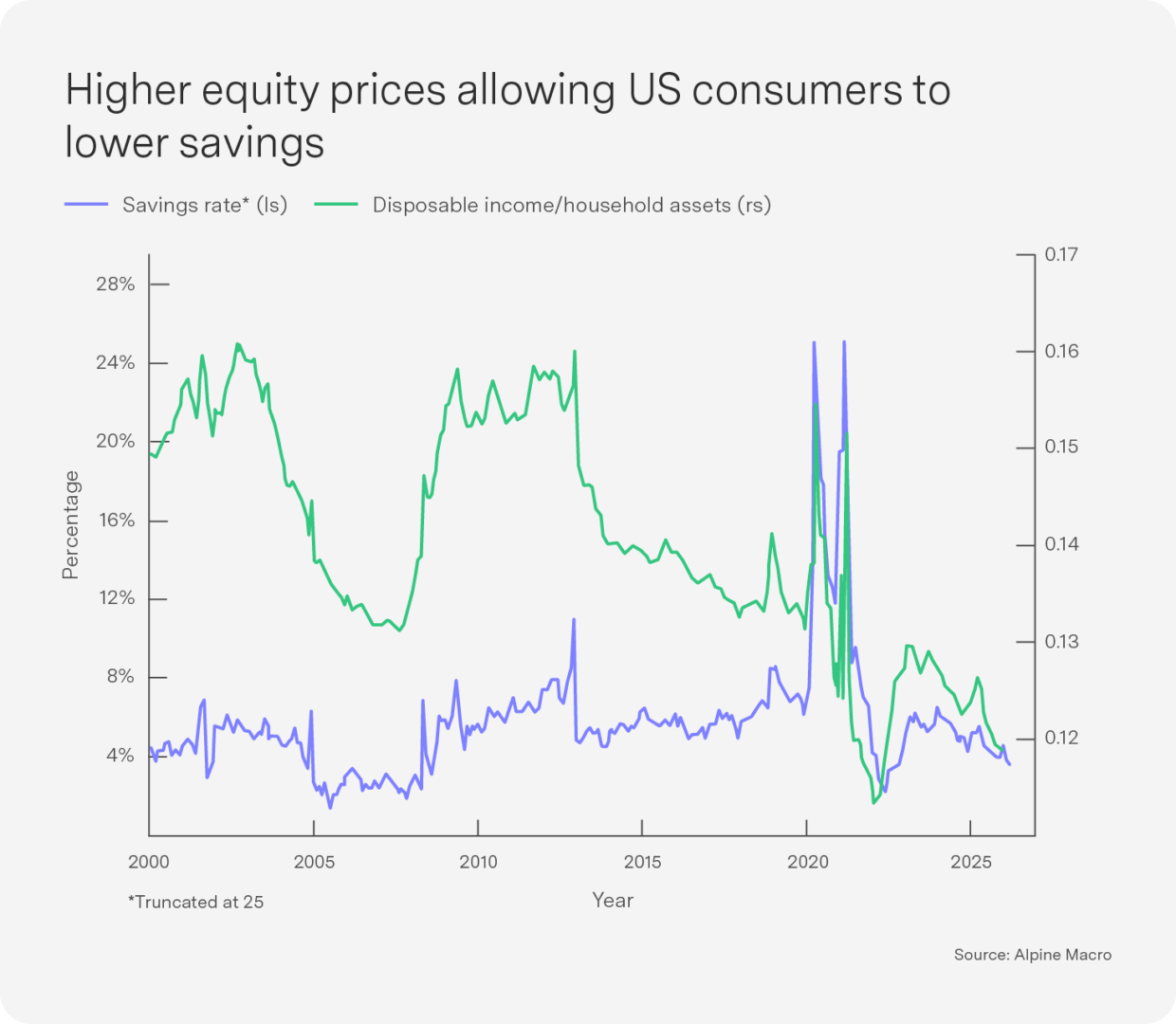

The consumer is still spending, but the buffer is shrinking. The savings rate fell to its lowest level in three years in March. The wealth effect has so far provided cover: the bull market in equities has given asset-owning households the confidence to run down savings without alarm (see chart). But this dynamic has a limit. A sharp, sustained drop in equity prices – driven by a monetary tightening cycle or a significant deterioration in forward earnings – would quickly remove that confidence and leave consumers exposed. For now, there is no clear sign of either development, but the margin for error is narrowing.

China: Taiwan emerges as the defining risk in US-China relations

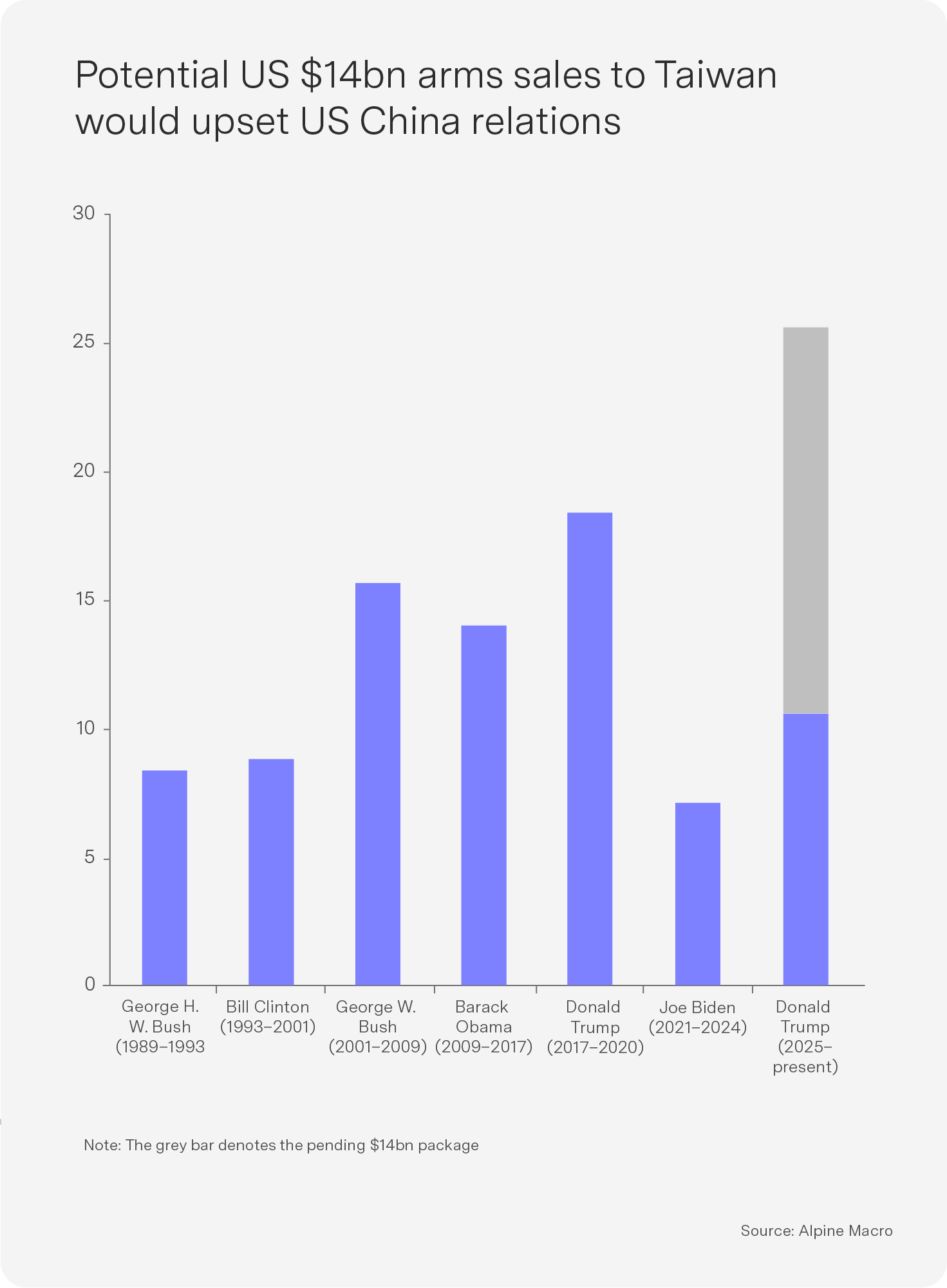

The Xi-Trump summit produced little concrete progress on Iran, AI or Taiwan, though Taiwan quickly dominated proceedings. “The Taiwan issue is the most important issue in China-US relations,” Xi said, according to Xinhua. “If mishandled, the two nations will experience collision or even clashes, pushing the entire China-US relationship into a highly dangerous situation.” Trump maintained the US’s long-standing posture of strategic ambiguity regarding Taiwanese independence, but he paused the pending $14 billion US arms sale to Taiwan, risking bipartisan backlash in Washington to appease Beijing. The renminbi’s behaviour is telling. Despite China’s heavy dependence on Iranian energy imports, the renminbi has strengthened against the dollar since the war began – reflecting rising geopolitical status rather than economic resilience.

On other fronts, the summit delivered modest outcomes. The tariff truce was extended, China agreed not to interfere with the US blockade of Iran and committed to withholding arms from Tehran and to purchase at least $17 billion in US agricultural products annually through 2028. Trump indicated he may ease some Iran-linked sanctions on China, significant given that China is Iran’s largest oil buyer. China’s domestic economy remains under pressure. April data showed broad-based deceleration: investment resumed its decline, and booming exports are no longer sufficient to offset weakening domestic consumption. Further government support is likely.

Outlook: The Strait still dominates, but inflation is becoming broad-based

Negotiations between the US and Iran have swung sharply from day to day, alternating between optimism over a potential deal and threats of destruction, with markets increasingly desensitised to each development. Core sticking points remain Iran’s uranium stockpile, control over the Strait of Hormuz and the ongoing US naval blockade of Iranian ports.

When the Strait eventually reopens, Gulf producers will have a powerful dual incentive to pump aggressively: financing domestic reconstruction and undermining Iran’s oil revenues. Gulf countries account for the vast majority of the estimated 4.3 million barrels per day of global excess production capacity. The United Arab Emirates, which produces 3.2 million barrels per day, has already moved decisively, announcing its departure from OPEC on 11 May. Even so, it will take time for refineries, ports and terminals to return to full operation.

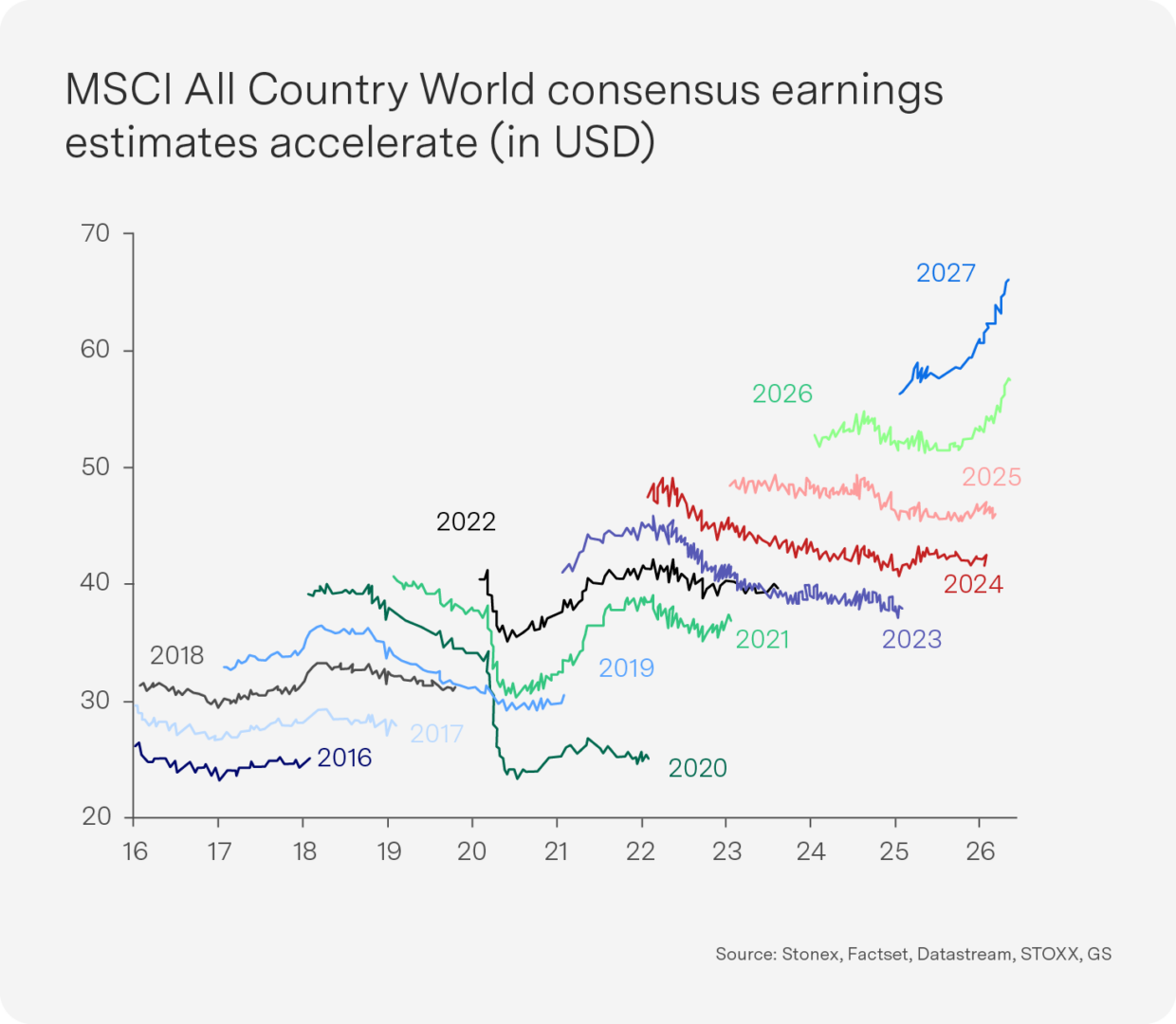

Markets have differentiated sharply, rewarding AI winners and punishing oil importers. US equities have been notably insulated from the oil shock, supported by strong earnings, the absence of Fed rate hikes and by tax relief from the One Big Beautiful Bill Act. This price rally has been matched by rising consensus earnings forecasts (see chart).

Key indicators