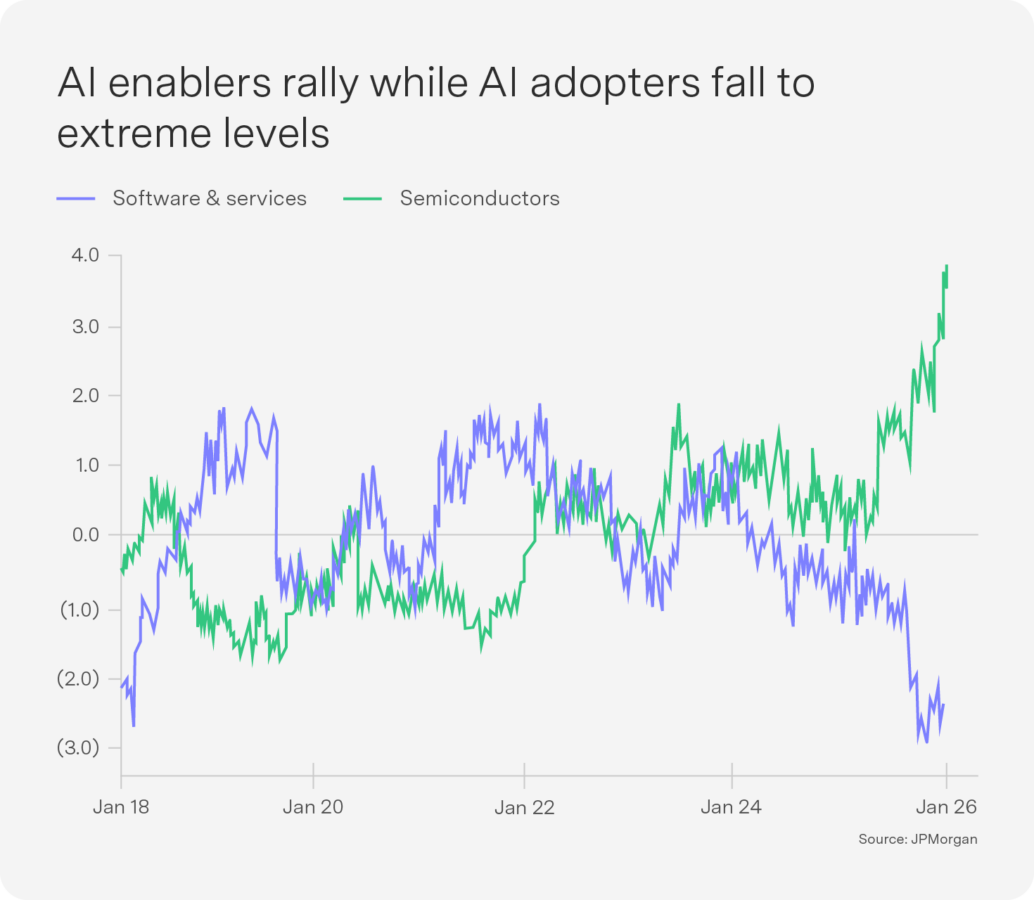

Semiconductor surge and software slump – the great AI divide

Market participants are increasingly discriminating between AI “enablers” – the infrastructure providers supplying the picks and shovels of the AI revolution – and AI “adopters” – software companies that must now prove their ability to monetise these capabilities. Companies like Nvidia and Broadcom continue to command premium valuations supported by structural demand, while traditional software-as-a-service (SaaS) providers such as Palantir and Crowdstrike face mounting scrutiny as investors question whether AI tools will render existing platforms obsolete, particularly as SaaS company growth rates have declined sequentially every quarter since their 2021 peak. The anxiety around software incumbents jumped when Anthropic released a productivity tool targeting in-house legal departments, triggering a sell-off that temporarily erased an estimated $300 billion in market capitalisation across publicly traded software companies, including Salesforce, ServiceNow and Adobe. This effect was later also felt by the security software sector when Anthropic released an AI tool for hunting software bugs.

The hyperscalers have also seen their share price fall as investors worry about monetising the huge investment required for infrastructure, particularly data centres. Capital expenditure (capex) is projected to exceed $600 billion in 2026, creating sustained tailwinds for infrastructure providers like Nvidia and Broadcom. Fortunately, the “Big 4” hyperscalers (Amazon, Microsoft, Meta and Google) are demonstrating disciplined capital allocation. These companies are generating incremental AI-related revenues – primarily through surging demand for cloud services – and their investment cycle is being funded through record-high free cash flow. Looking beyond large language models, AI is expanding into “physical AI” – the integration of advanced language models with robotics and industrial automation. Amazon’s warehouse automation and Google’s Waymo autonomous vehicle platform are early manifestations of this next wave of AI. Apple is ramping up work on three new wearable devices: smart glasses; a pendant; and AirPods with expanded AI capabilities. Netflix’s share price retreated on concerns that it might overpay for Warner Brothers, but it recovered after they dropped their bid.

Artificial intelligence is, at its core, a labour-displacing technology, making it strongly pro-profit and anti-labour. Governments are pivoting to AI sovereigns, creating technology companies as national assets – so antitrust policies are unlikely to return to protect labour. As companies rush to build out data centres and businesses invest in power-generating capacity, the accelerating capex will generate jobs, partially offsetting labour displacement by AI. Profits are also likely to broaden when ordinary firms apply AI to reduce costs, expand margins and pursue growth. The technical correction in mega-cap technology stocks has meaningfully improved riskadjusted entry points, but we prefer our technology access through emerging markets for now.

A supply-side budget in plain sight: Analysing the Budget 2026/2027

This is very clearly a supply-side budget, with National Treasury looking to use taxation as an instrument of economic growth. It is the most comprehensive reset of the tax system in a decade in South Africa. Long may this innovative policy thinking continue. Before delving into the tax proposals, let us examine the fiscal picture more closely. The GDP numbers are well known and confirm the economy’s anaemic recovery over the next two years, as real GDP growth is projected at 1.6% in 2026, rising to 2.0% by 2028. An important footnote here: The 2026 number is actually below the Budget estimate last year of 1.9%, where the pressure of making the denominator work with the VAT removal arguably forced a few heroic GDP assumptions. With inflation forecast to remain in the 3% range over the next few years, there is a semblance of macroeconomic stability akin to the Mbeki years.

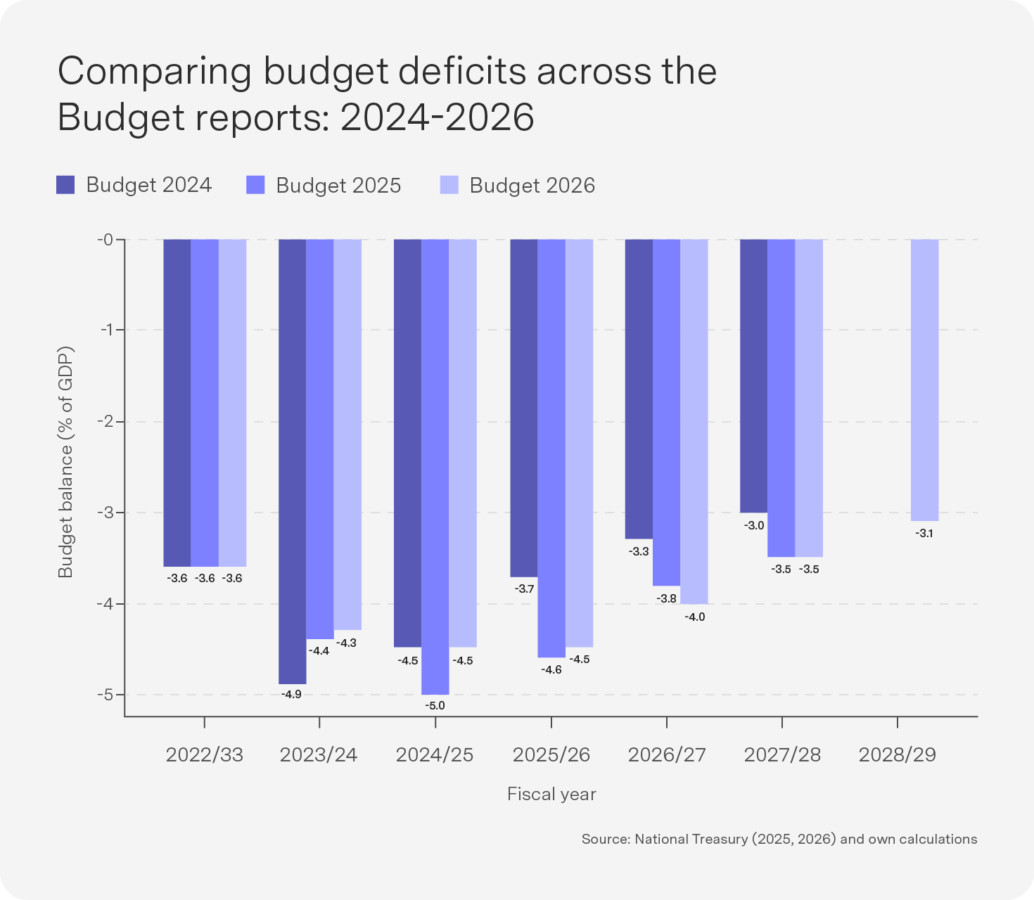

The task of reducing the deficit remains Herculean, however, as illustrated by the various debt metrics. In terms of the deficit-to-GDP ratio – shown across the last three Budget years below – the consolidated budget deficit is projected to narrow from 4.5% of GDP in 2025/26 to 3.1% by 2028/29. Look more closely, though, and a few adjustments relative to the previous two Budgets become apparent: a slight reduction in this year’s projected deficit, from 4.6% to 4.5%, which is positive but not outstanding; and in the next fiscal year, the budget deficit will actually be higher than projected last year (4% versus 3.8%). This speaks to a moderate fiscal consolidation plan that is broadly on track, rather than a significant fiscal deficit reduction plan. This probably explains why there has been a reference to the fiscal anchor but not a firm commitment as yet.

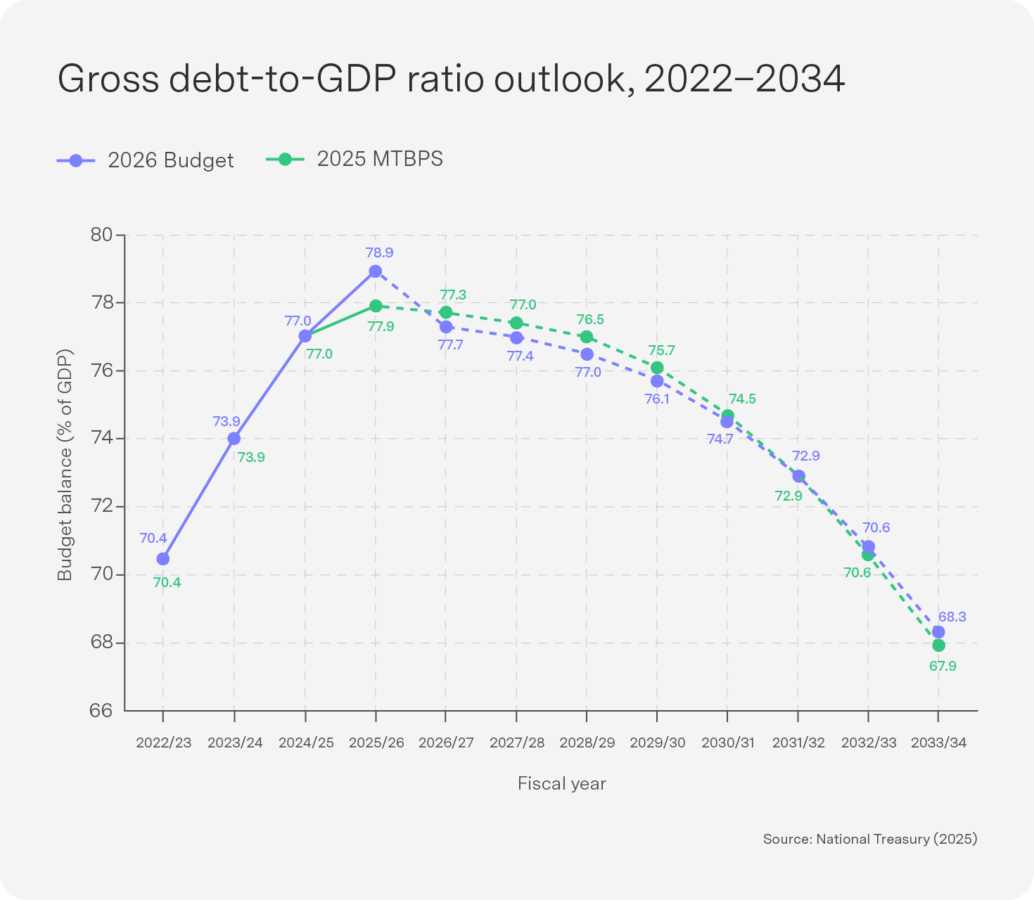

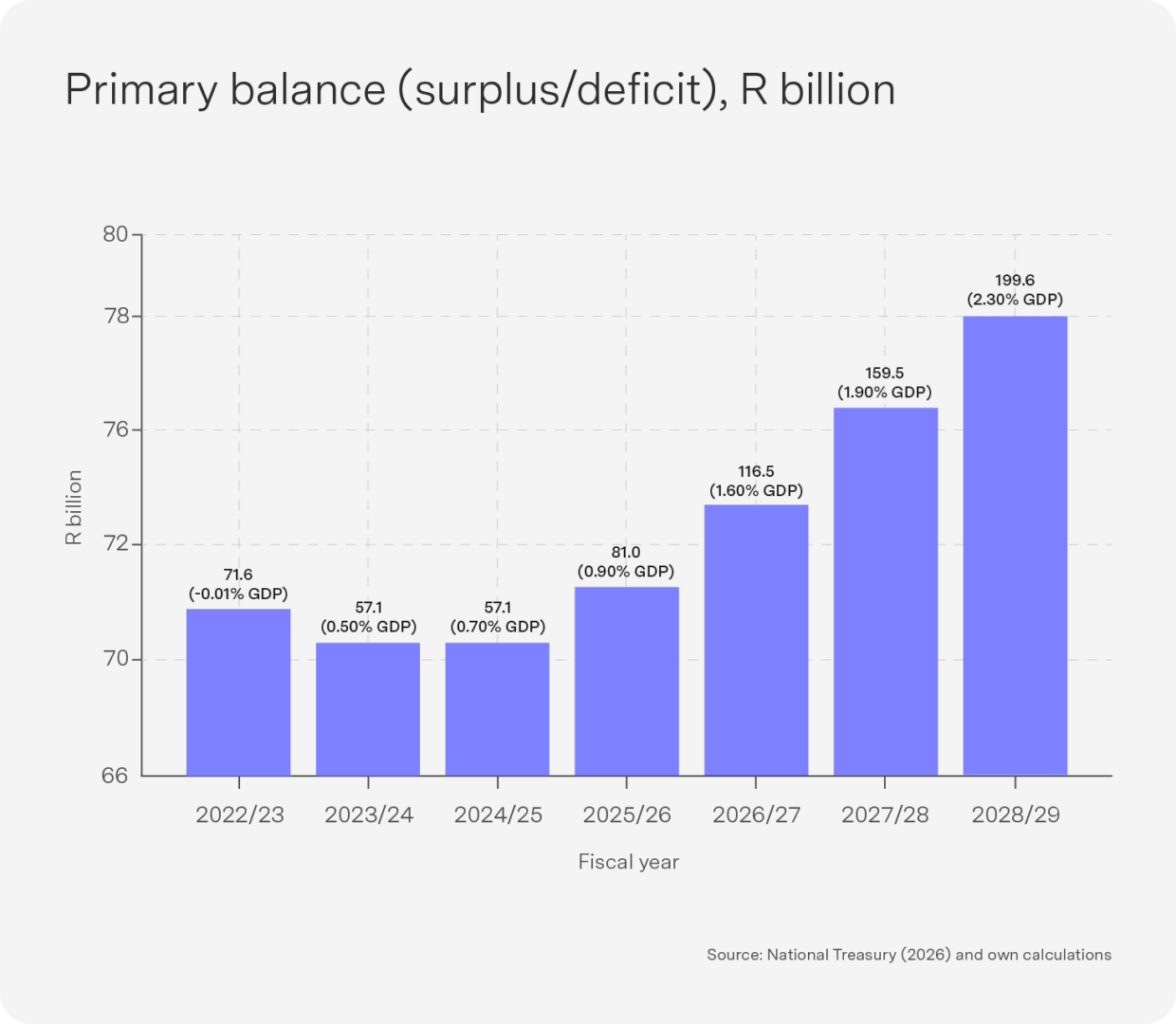

In turn, the debt-to-GDP ratio is set to increase somewhat sharply in the coming fiscal year, from the Medium-Term Budget Policy Statement estimate of 77.9% to 78.9%. As is clear, however, the consolidation plan is quickly retained as debt-to-GDP levels (assuming GDP growth rates are met) quickly fall back into the planned fiscal consolidation path. In essence, this is because lower inflation and thus lower (nominal) GDP have mechanically raised our debt-to-GDP ratios, which is expected. The Treasury team also referenced the reordering of their cash holdings given upcoming large redemptions as another factor in this 1 percentage point increase in debt-to-GDP levels. The primary fiscal surplus, which measures revenue less non-interest expenditure, has continued unabated, however, meaning that revenue is greater than non-interest expenditure. The Budget confirmed this, as did the Minister in his speech. There has thus been a rise in the primary fiscal surplus from 1.6% to 2.3% as a share of GDP over the three-year period of the medium-term economic framework. However, this surplus is again partly reliant on a Gold and Foreign Exchange Contingency Reserve Account bail-in over the next two years of about R76 billion. Most crucially, though, debt servicing costs will come down despite the overall stock of debt-to-GDP rising next year, suggesting careful cash flow management on the part of National Treasury. Debt service costs are set to decline from 21.3 cents for every rand of revenue to 20.4 cents over the next three fiscal years. This is a key change in course that should allow for some breathing room on the expenditure side.

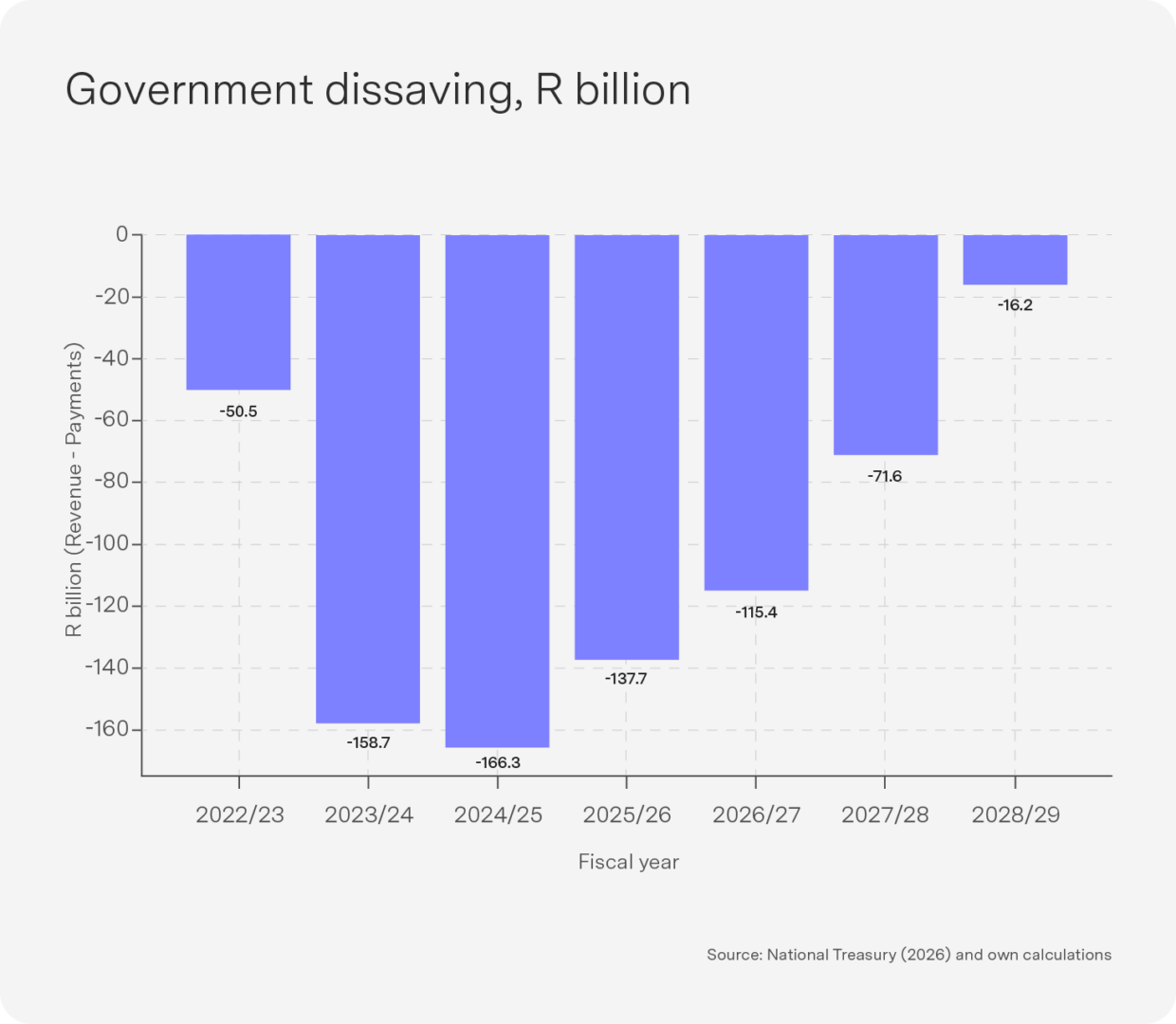

Fiscal prudence in the Budget focused variously on locating irregular claimants from the social grants system, removing the public transport network grant and early retirement programmes in the public sector. But this may not be enough – and may lie at the heart of the steady but hardly spectacular deficit and debt stabilisation programme. So despite National Treasury best efforts at fiscal responsibility, government dissaving continues (i.e. current non-investment expenditure by the state exceeds its current revenue). Simply put, government still does not have sufficient revenue to pay for operational expenditure over the next three years – the wage bill, interest payments, transfers, procurement and so on. Government dissaving, though declining, will remain part of our fiscal landscape for the foreseeable future. The conundrum faced by the fiscal authorities is clear: Deeper cuts in the public sector through the wage bill would be politically explosive and could result in poorer service delivery. At the same time, the economic-growth get-out-of-jail card is simply not high enough to provide sufficient fiscal space. The task of reducing the deficit remains Herculean, however, as illustrated by the various debt metrics. In terms of the deficit-to-GDP ratio – shown across the last three Budget years below – the consolidated budget deficit is projected to narrow from 4.5% of GDP in 2025/26 to 3.1% by 2028/29. Look more closely, though, and a few adjustments relative to the previous two Budgets become apparent: a slight reduction in this year’s projected deficit, from 4.6% to 4.5%, which is positive but not outstanding; and in the next fiscal year, the budget deficit will actually be higher than projected last year (4% versus 3.8%). This speaks to a moderate fiscal consolidation plan that is broadly on track, rather than a significant fiscal deficit reduction plan. This probably explains why there has been a reference to the fiscal anchor but not a firm commitment as yet.

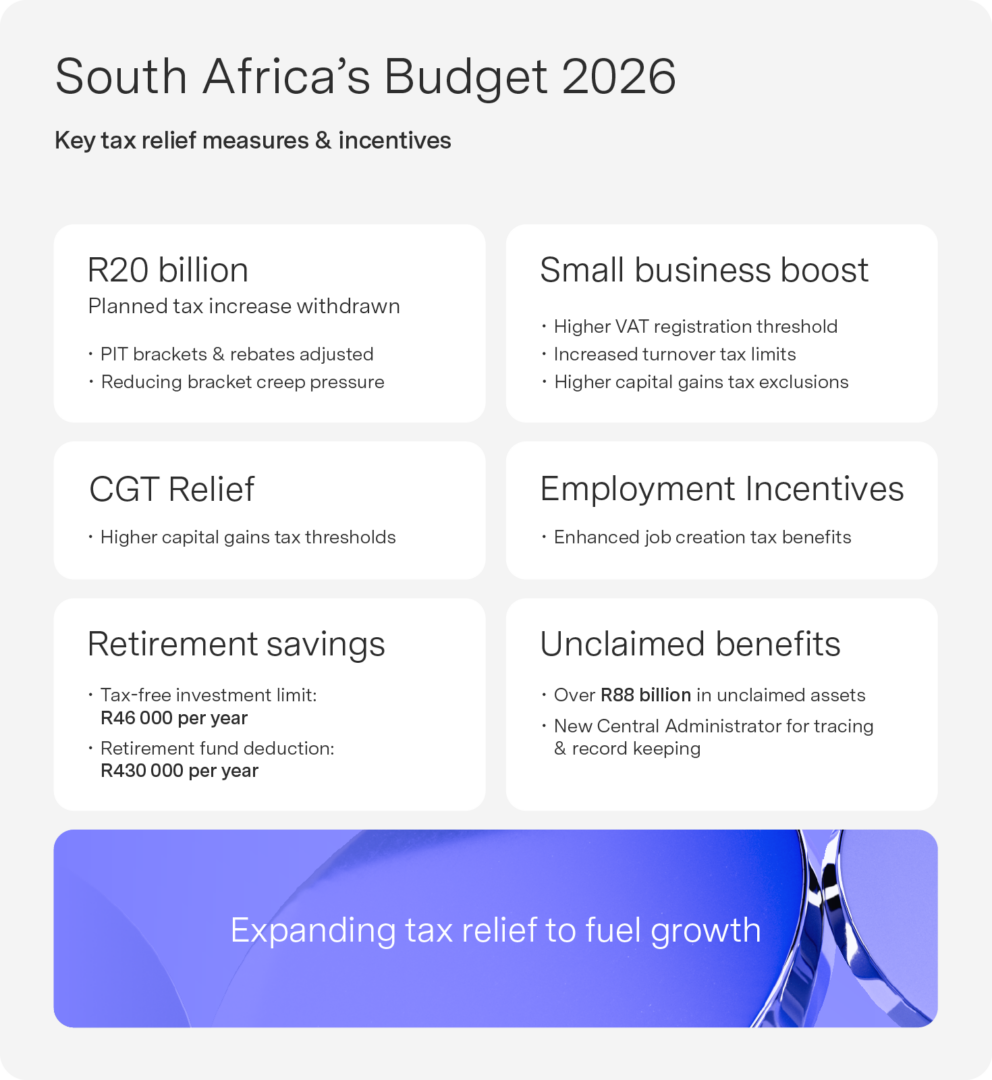

The Minister announced a significant change in policy in the tax regime, signalling the intent to create breathing room for firms and individuals. A raft of tax adjustments will incentivise growth, productivity and savings in one of the strongest tax reforms since democracy. This was a genuine policy change and not simply a function of the revenue windfall realised through SARS efficiency and the minerals windfall. The headline tax message was the cancellation of the previously pencilled-in R20bn tax increase (via bracket creep) intended to fund expenditure in the absence of a VAT increase last year. Allied to this was the adjustment of personal income tax brackets, rebates and thresholds, reducing bracket creep pressure and increasing household disposable incomes. While this relief is not expansionary in a Keynesian sense given it is only 3.5%, it remains meaningful. The serious tax relief is in the explicit supply-side incentives in a range of small business tax relief measures, such as higher VAT registration, turnover tax and capital gains tax (CGT) thresholds and CGT exclusions. The donations tax cap and a series of employment-related tax benefits have also increased. With little fiscal space for investment expenditure, the National Treasury team did the next best thing – widening and deepening the tax relief package available to South Africans.

The key financial services proposals are for the annual tax-free investment limit to increase from R360 000 to R460 000 per year and for the limit on retirement fund deductions to increase from R350 000 to R430 000, allowing individuals to invest more each year on a tax-free basis. This is a clear attempt to incentivise retirement savings amongst South Africans. In addition, the NT team have put financial assets holders on watch with respect to unclaimed benefits. The Minister noted that the more than R88 billion of unclaimed financial assets and benefits will be subject to oversight and management from a central administrator responsible for record keeping and tracing.

Ultimately this Budget will be remembered for its continued focus on fiscal consolidation, making all the right moves in terms of expenditure commitments and rationing. Most importantly, perhaps, this budget will be remembered for placing supply-side incentives at the front and centre of fiscal policy in South Africa through significant tax relief for individuals and companies.

Top-performing Sygnia funds

The global property market roared back to life in February due to easing interest rates, improved debt liquidity and renewed investor confidence in commercial real estate fundamentals. Japan is in the top five following Sanae Takaichi’s historic election victory. South Africa still dominates the top five spots over 1 and 12 months on the back of a weaker dollar and strong commodity prices, with emerging markets the only global fund over 12 months.

1-month absolute performance as at 26 February 2026

- Sygnia Itrix Global Property ETF 8.1%

- Sygnia Itrix MSCI Japan ETF 6.6%

- Sygnia Itrix MSCI Emerging Markets 50 ETF 6.3%

- Sygnia Divi Index Fund 5.8%

- Sygnia Itrix Top 40 ETF 5.5%

12-month absolute performance as at 26 February 2026

- Sygnia Itrix Top 40 ETF 54.7%

- Sygnia Top 40 Index Fund 53.9%

- Sygnia Listed Property Index Fund 40.4%

- Sygnia Itrix MSCI Emerging Markets 50 ETF 39.3%

- Sygnia Divi Index Fund 39.0%

US: Improving employment, strong growth and sticky inflation

The US Supreme Court recently ruled that President Trump’s reciprocal tariffs were unlawful, opening the possibility of $175 billion in refunds. Trump responded by applying a flat 10% global tariff and an intention to increase this to 15%. On average, tariffs will drop slightly, but countries whose tariffs were higher than 15% are the clear winners – like China, Brazil and South Africa – while countries like Australia and the UK (with lower original deals) could see a hike to the 15% baseline. Uncertainty has increased, and the European Union has frozen ratification of its US trade accord. Similarly, Japan may renege on its $550bn US investment pledges. Back home, the Democrats are pushing for taxpayer refunds ahead of midterms. Though uncertainty has increased, we do not expect an escalation given the midterm focus and cost of living concerns.

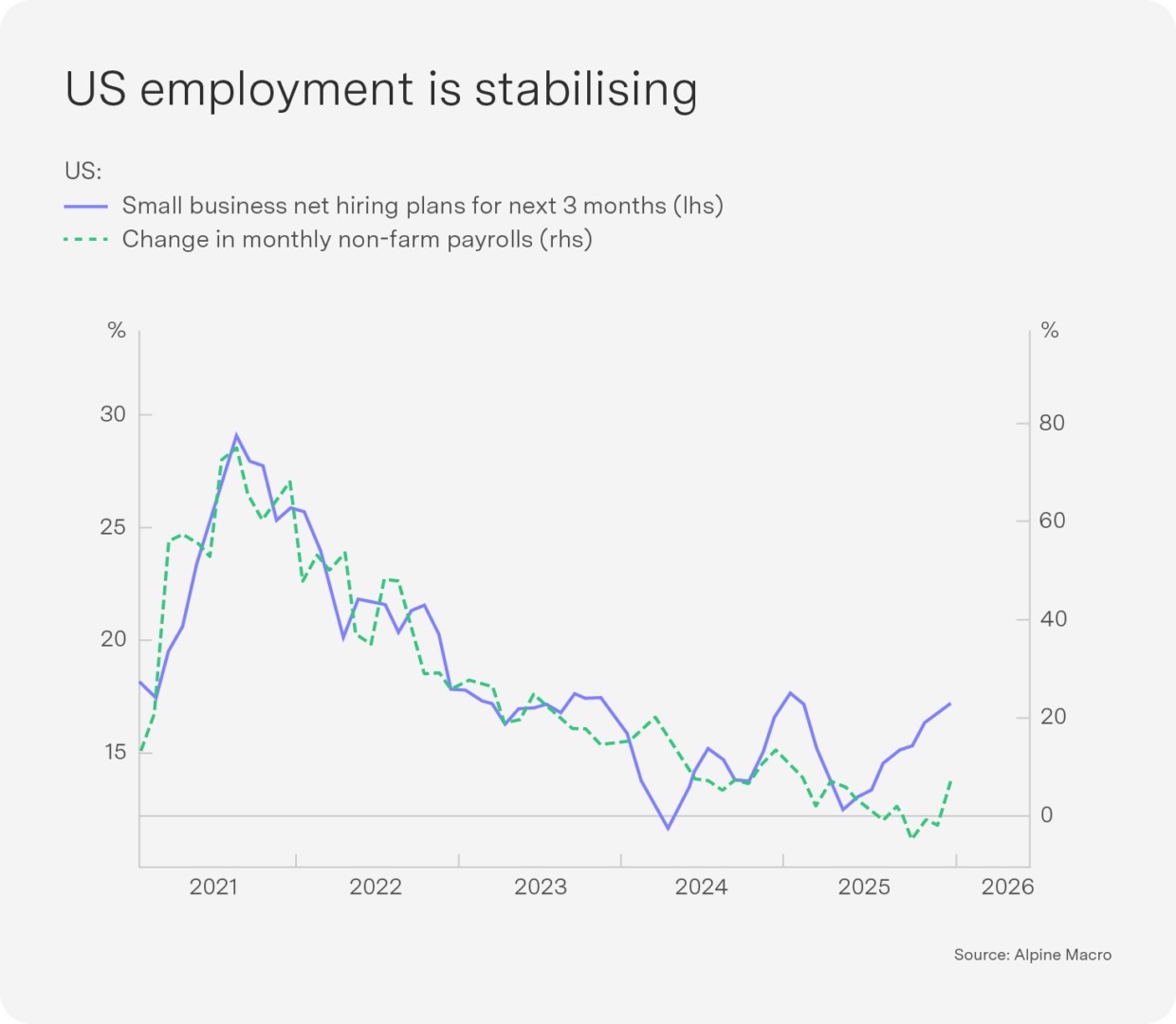

The US economy is showing genuine strength. The Atlanta Fed’s GDPNow model projects Q1 GDP growth above 4%, and January’s non-farm payrolls came in at roughly double expectations, with the unemployment rate falling further than forecast to 4.3%. It is not surprising, then, that inflation has been stubborn. The US core personal consumption expenditure index rose higher than expectedto 3.0% year-on-year in December. With employment recovering (as indicated by the small business net hiring plans in Chart 2) and inflation persisting, the Fed has little reason to move, and rates are likely to be on hold for at least the next six months. While Kevin Warsh, Trump’s nomination as the next Fed chair, is expected to push for rate cuts, Fed governor Michael Barr and San Francisco Fed president Mary Daly have both stated that increased AI productivity could actually lead to higher rates, a sentiment supported by vice chair Philip Jefferson.

Japan: Takaichi’s historic triumph triggers bond tremors

Prime Minister Sanae Takaichi’s Liberal Democratic Party won the largest election margin of any Japanese party since World War II, a stunning mandate that sent the Nikkei surging over 5% to record highs. Markets are now positioning for the “Takaichi trade”: renewed selling pressure on ultra-long Japanese government bonds, a weaker yen and rising equity markets as investors price in looser fiscal policy ahead.

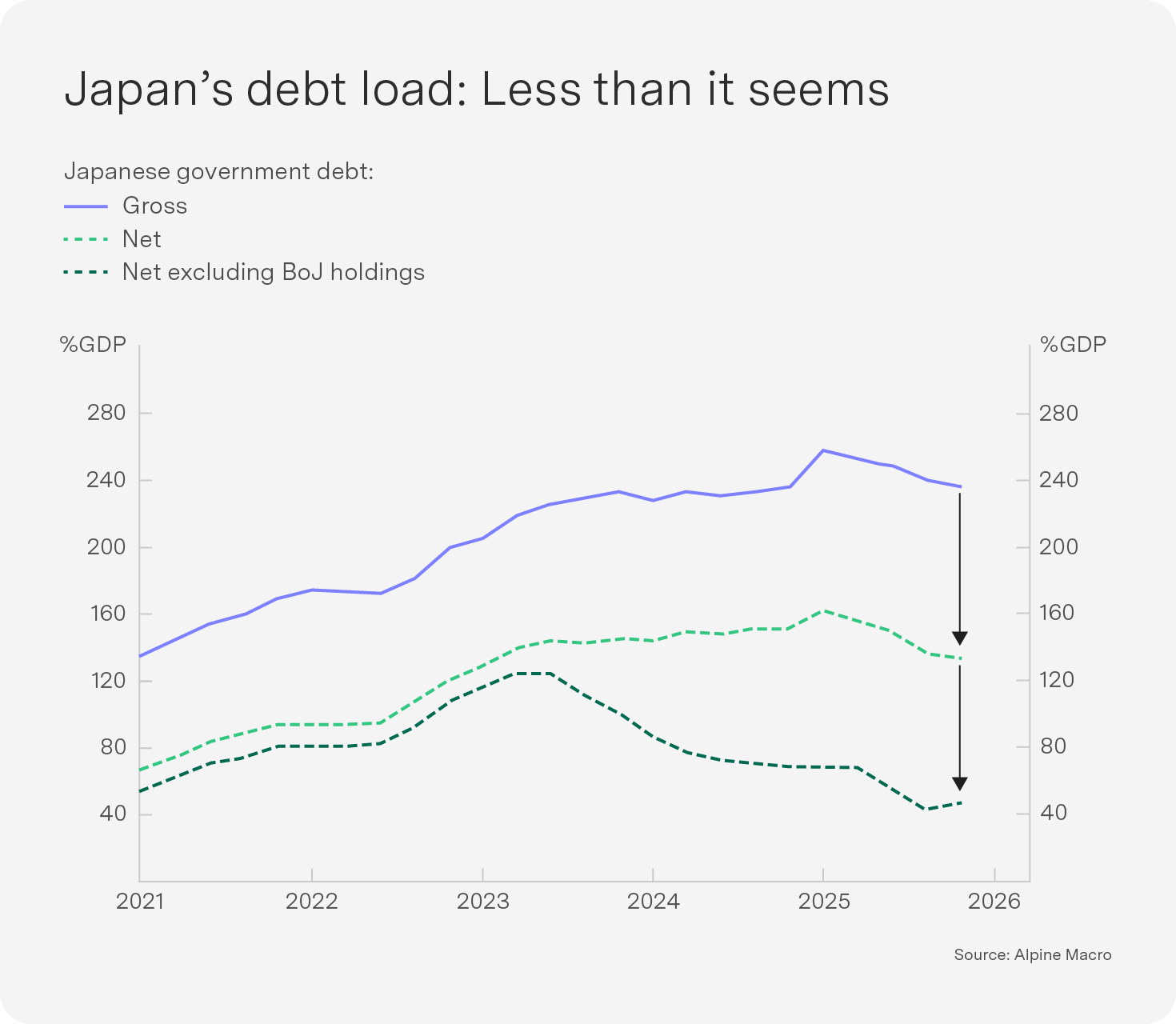

Despite the Takaichi trade, Japanese bonds and the yen should stabilise. Wage growth is cooling, real wages are rising at around 0.6% – roughly in line with productivity growth – and the yen remains grossly undervalued. As interest rate differentials between Japan and the US continue to narrow, the currency should appreciate against both the dollar and the euro, which will further assist inflation. Fears over Japan’s debt are also overstated. While its gross public debt is the highest in the developed world at 237% of GDP, this figure is misleading. Japan’s government holds substantial assets, bringing net debt down to 134%. Factor in the Bank of Japan’s holdings of nearly half of all outstanding government debt, and the ratio drops further still, to just 47%. Japan also runs a large current account surplus, meaning its private sector generates enough savings to fund the fiscal deficit with room to spare. Relative to other G7 nations, Japan is well placed to ease fiscal policy modestly without triggering a debt crisis.

China: Global diversification and zero tariffs for SA

While China’s official foreign exchange (forex) reserves have hovered around $3 trillion for nearly a decade, its overall international investment position has continued to expand through other channels (outward foreign direct investment, portfolio investment and overseas lending (see Chart 4)). Beijing has actively encouraged this diversification across public and private sectors. Private firms have shifted production abroad to build more resilient supply chains, while policy banks and state entities have stepped up overseas lending and investment under the Belt and Road Initiative. Xi Jinping announced on 14 February that China will provide zero-tariff treatment to 53 African nations starting 1 May, 2026, strengthening economic ties and expanding the Belt and Road Initiative. South Africa will benefit directly from this policy.

China’s external balance sheet is thus increasingly being built through quasi-private and state-linked channels rather than official reserve accumulation. Part of this has been funded by reducing holdings of US Treasuries – now around 2% of outstanding US debt, down sharply from nearly 14% in the early 2010s. This shift has significantly reduced China’s vulnerability to potential US sanctions. While China’s gold holdings have grown in the official forex reserves, its allocation is dwarfed by China’s other global holdings.

Outlook: Strong growth tempered by high valuations and rising risks

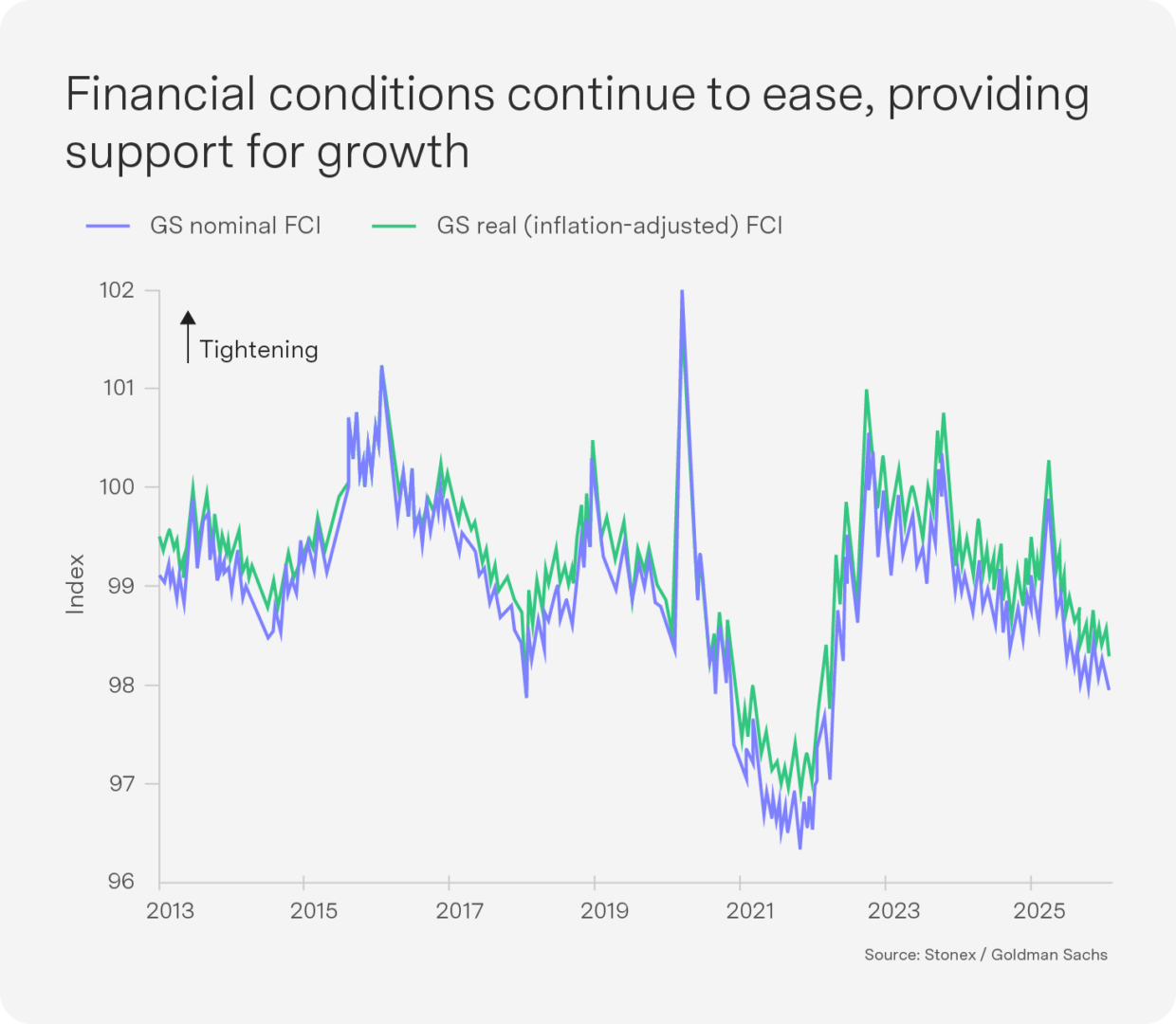

A move to more balanced growth is now taking place, in which a cooling in consumer spending is accompanied by a pickup in job growth and non-tech business spending. Stable growth and easy liquidity conditions (see Chart 6) have kept us overweight equities, but valuations are stretched and risks are rising.

The United States and Israel launched coordinated missile strikes against Iran, killing Supreme Leader Ayatollah Ali Khamenei. The large-scale attacks targeted Iran’s military infrastructure with the stated aim of preventing the country from developing a nuclear weapon. Iran responded with retaliatory missile strikes on targets across the Middle East. President Trump stated that bombing operations would continue through the week. In response to the escalating conflict, OPEC+ agreed to increase oil production to help offset potential supply disruptions, though a geopolitical risk premium in global oil markets is expected to persist.

In Europe, the withdrawal from US security dependence is driving a permanent step-up in defence spending and industrial capacity. This creates compelling top-down investment themes, but Europe’s deep structural weaknesses – overregulation, fragmented capital markets and chronically low-trend growth – are not going away anytime soon and will continue to drag on broader opportunities.

In the US, new tariff regimes and midterm elections are introducing a near-term source of volatility. If the consensus view holds (80% probability of the Democrats taking the House), the midterm outcome will result in domestic gridlock, which may force Trump to pivot to a renewed focus on global initiatives.

We remain overweight emerging markets and South African equities, with the expectation of a weaker dollar, Asian technology investment and China resilience.

Key indicators