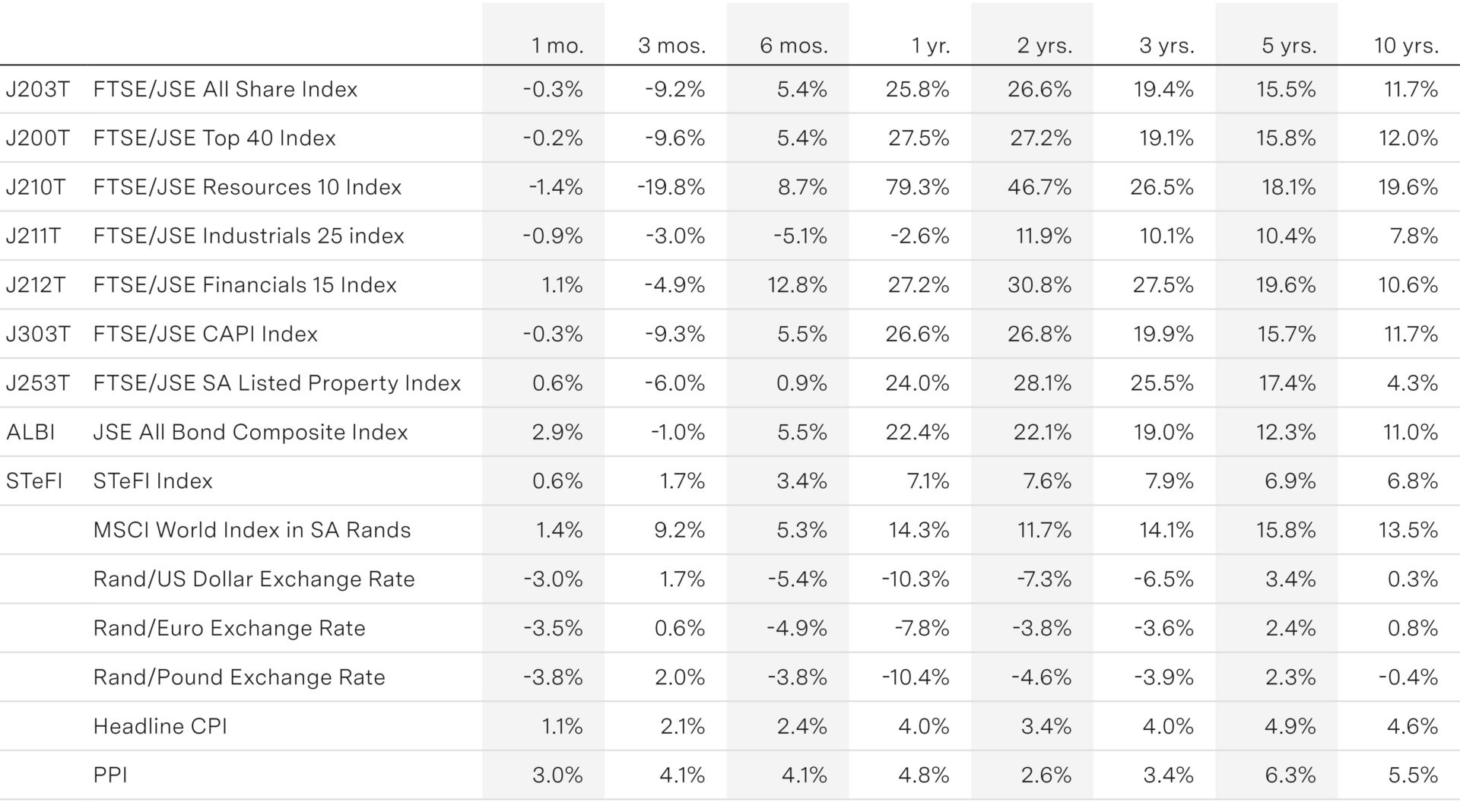

Debasement trade crumbles as Fed prepares to hike

Gold has fallen more than 25% from its peak and bitcoin more than 50% as strong US jobs data and the Fed’s reaffirmation of its inflation target pile pressure on assets that had rallied on fears of currency debasement. May US payroll growth came in well above the highest forecast, with substantial upward revisions to prior months. To put the number in context, St Louis Fed economists estimate that monthly job creation of 30 000–85 000 is sufficient to avoid pushing unemployment higher. At 172 000, May’s print was double the top of that range. For the Fed, the figures settle the question of labour market softening, allowing it to turn its full attention to the inflation side of its dual mandate. Half of the Fed’s 18 members now anticipate at least one rate increase this year, and a third project two or more – a clear shift from the prior easing bias, notwithstanding the Middle East deal and lower oil prices. Markets were debating whether the Fed was quietly acquiescing to an implicit 3% inflation target after five years above the 2% threshold, but incoming chair Kevin Warsh vowed to restore price stability and confirmed the 2% inflation target remains key to the Fed’s mandate.

Markets reacted sharply to the strong payrolls and later to the hawkish Fed. Yields surged, the dollar strengthened and traders moved to fully price in an additional 25 basis points of tightening. The combination of a hawkish Fed, a stronger dollar and rising bond yields has weighed heavily on the debasement trade, which reflects a cluster of demand drivers: higher geopolitical uncertainty, longterm inflation uncertainty and concerns about debt debasement driven by large fiscal deficits across major economies. One measure of this trade is non-bank investors’ allocation to gold and bitcoin relative to their holdings of equities, bonds and cash. After a steady build-up from mid-2023, that allocation has been pulling back since the start of the Iran conflict and has now retreated to levels last seen in March 2025 (see Chart).

For emerging markets, a hawkish Fed will cap the emerging market rally. Lower oil prices will partially remove one headwind for emerging markets, but a more restrictive Fed introduces a new one through a stronger dollar and tighter global liquidity, reducing the profitability of the carry trade.

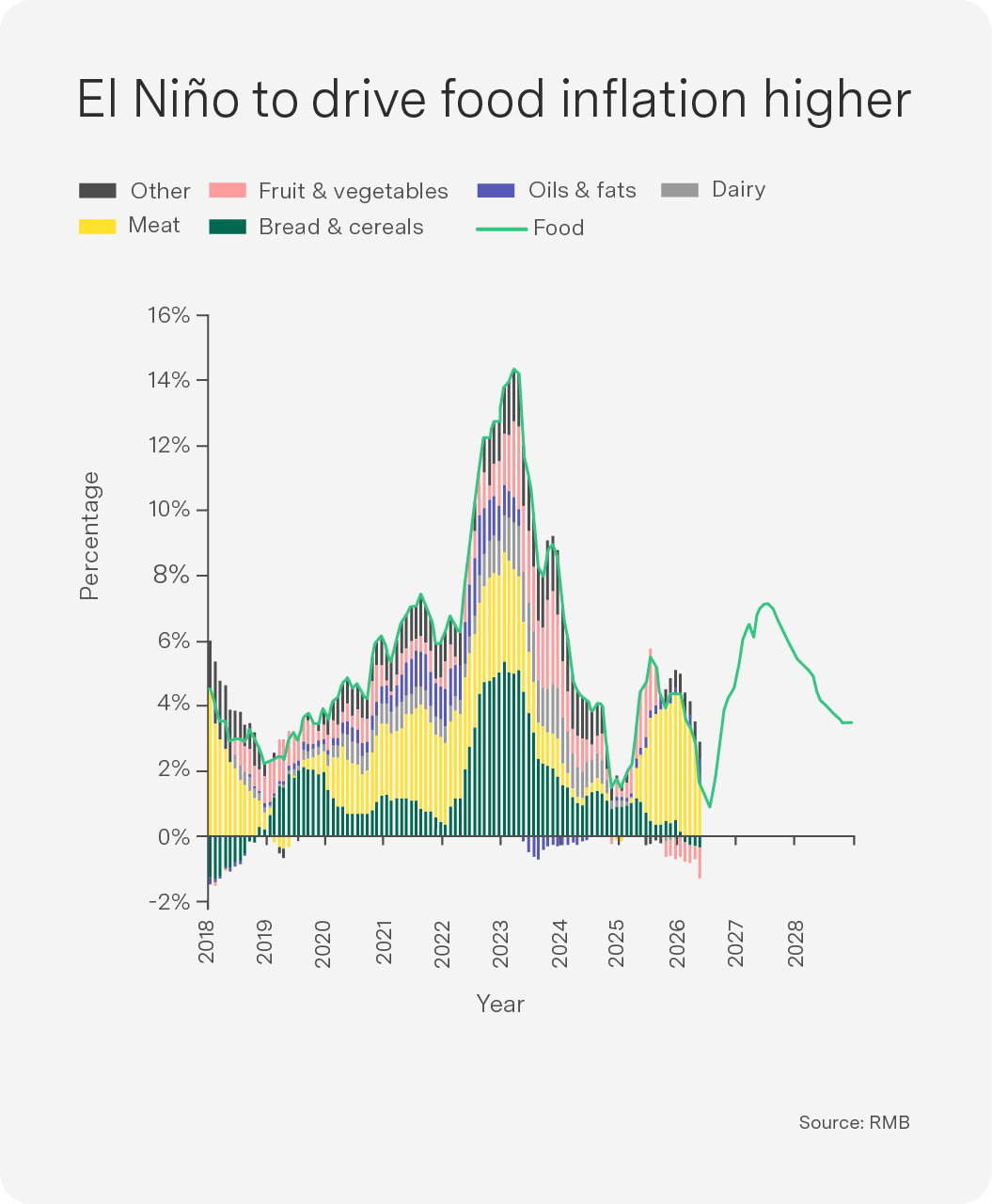

The new El Niño Price Index

Global and local concern about the impending El Niño weather shock is on the rise. Coined originally by Peruvian fishermen who noticed that their coastal waters became unusually warm in December – El Niño in Spanish means ‘the child’ – it refers to the ‘Christ child’ over the Christmas period. El Niño is a naturally recurring climate pattern, usually appearing every two to seven years. However, it now occurs in a hotter world – which means climate disruptions around the world are much more severe than before.

Put simply, warm water accumulates in the “wrong” part of the Pacific Ocean, disrupting normal wind and rainfall patterns across the tropics and subtropics. Climate agencies usually classify an El Niño event when sea surface temperatures in the key Niño-3.4 region are at least 0.5°C above average and are expected to remain elevated for several months. These conditions cause unusual changes in wind, cloud formation and atmospheric pressure, but climate change now elevates these changes, so there is a higher probability of hotter extremes, drought in some regions, floods in others and a more volatile global agricultural system. El Niño has in many ways become climate change’s reminder to us of the severe economic and social costs of rising temperatures on the planet.

The latest forecasts suggest that South Africa may be heading into precisely this risk window. International and local forecasts point to a high probability of El Niño developing through 2026 and potentially persisting into 2027. For South Africa, the timing is crucial, as farmers begin planting summer crops around October. Rainfall in the October to March period determines germination, crop development and final yields. A dry start followed by heat stress in December, January and February will threaten yields from these crops. In our case, El Niño is typically associated with hotter and drier conditions across the summer rainfall regions. This does not mean every El Niño automatically creates a drought. Pre-El Niño soil moisture, existing dam levels, the exact timing of rainfall and the severity of the event all matter as well – so we cannot predict the magnitude of this El Niño’s impact on agriculture as yet.

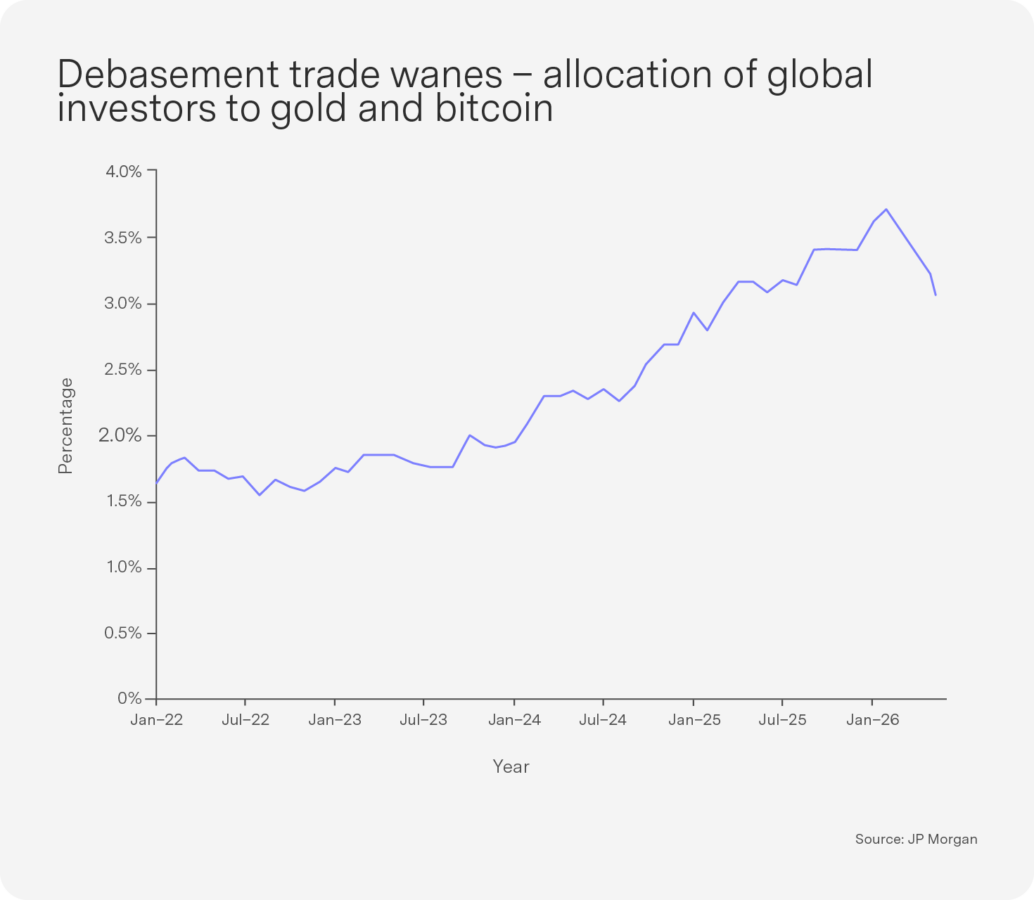

South Africa’s summer crop belt produces maize, soybeans, sunflower seed, sorghum, groundnuts and dry beans. Maize is the anchor crop in the food value chain – a staple food for households and a key input for animal feed. Maize production volumes and final prices thus serve as a central price signal for food when thinking about the consumer price index (CPI). Specifically, white maize matters directly for human consumption, while yellow maize matters indirectly through animal feed for poultry, pork, beef, dairy and egg farming.

El Niño drought conditions could shock white maize prices and, via the yellow maize channel, the price of poultry, beef, pork, eggs, dairy, cereals and more. The average South African household spends a disproportionate share of their income on food. Conservatively, these ‘El Niño-sensitive’ products constitute about 12% of the average household consumption in South Africa – but notably a huge 65% of all food consumption. And these percentages would be appreciably higher for poor households. So a large El Niño weather shock is likely to cause a significant El Niño food price shock downstream. More careful modelling is required to track an El Niño price index.

The import channel, already susceptible to elevated oil prices, is also vulnerable. When domestic production is weak, South Africa imports maize, wheat, rice, vegetable oils and animal-feed inputs. Putting the not-insignificant detail of the oil price aside, we may also be hit by imported inflation if our domestic production and a number of other major producing regions are affected by El Niño at the same time.

But local experts – notably our very own agriculture guru, Wandile Sihlobo – argue that we may have some short-term buffers. Firstly, South Africa has just come off two strong agricultural seasons, so grain stocks are healthy. Secondly, evidence shows high soil moisture as a consequence of recent good rains, a key mitigant to delayed crops. Finally, dams in many parts of the country are not starting from crisis levels, as has been the case in previous El Niño events, so there is a water reserve.

The El Niño event is a very important reminder that supply shocks now drive the decision-making of central banks around the world. In the event of an El Niño price shock through the domestic and external supply channels, the South African Reserve Bank (SARB) will have to consider raising rates to avoid second-round price effects, deanchor inflationary expectations and embed wage demands. This will of course threaten the newly minted inflation targeting range.

The policy response from the monetary authorities is dependent on the severity of El Niño. In a mild scenario with good stock levels and limited crop damage, the SARB may look beyond these temporary food-price pressures. In a severe scenario, however, with maize prices rising and food inflation becoming sticky, the SARB would delay rate cuts – and in an extreme case, possibly even implement a hike. In this new world of monetary policy, simply raising rates to curb domestic demand and allow consumption to recover through lower inflation is a rarer occurrence than it used to be. Supply shocks seem to be the new order of the day, raising rates to curb prices, but sacrificing growth. Climate change appears to be turning weather events into a regular monetary-policy variable.

Top-performing Sygnia funds

The weaker rand helped global stocks over the month of June, with defensive funds showing a strong return, including healthcare, property and Berkshire Hathaway.

Emerging markets continue to be the best performer over 12 months, with close to double the performance of the second-ranked fund. South Africa has the next four positions across all asset classes, including bonds, property and equities.

.

1-month absolute performance as at 29 June 2026

- Sygnia Itrix Health Innovation Actively Managed ETF 7.7%

- Sygnia Life Berkshire Hathaway Portfolio 6.8%

- Sygnia Health Innovation Global Equity Fund 6.1%

- Sygnia Listed Property Index Fund 4.6%

- Sygnia Itrix Global Property ETF 3.9%

12-month absolute performance as at 29 June 2026

- Sygnia Itrix MSCI Emerging Markets 50 ETF 58.3%

- Sygnia Listed Property Index Fund 30.8%

- Sygnia Enhanced All Bond Fund 22.0%

- Sygnia Transnational Equities Fund 21.8%

- Sygnia All Bond Index Fund 21.4%

US: Trump escalates tariff war despite stubbornly high inflation

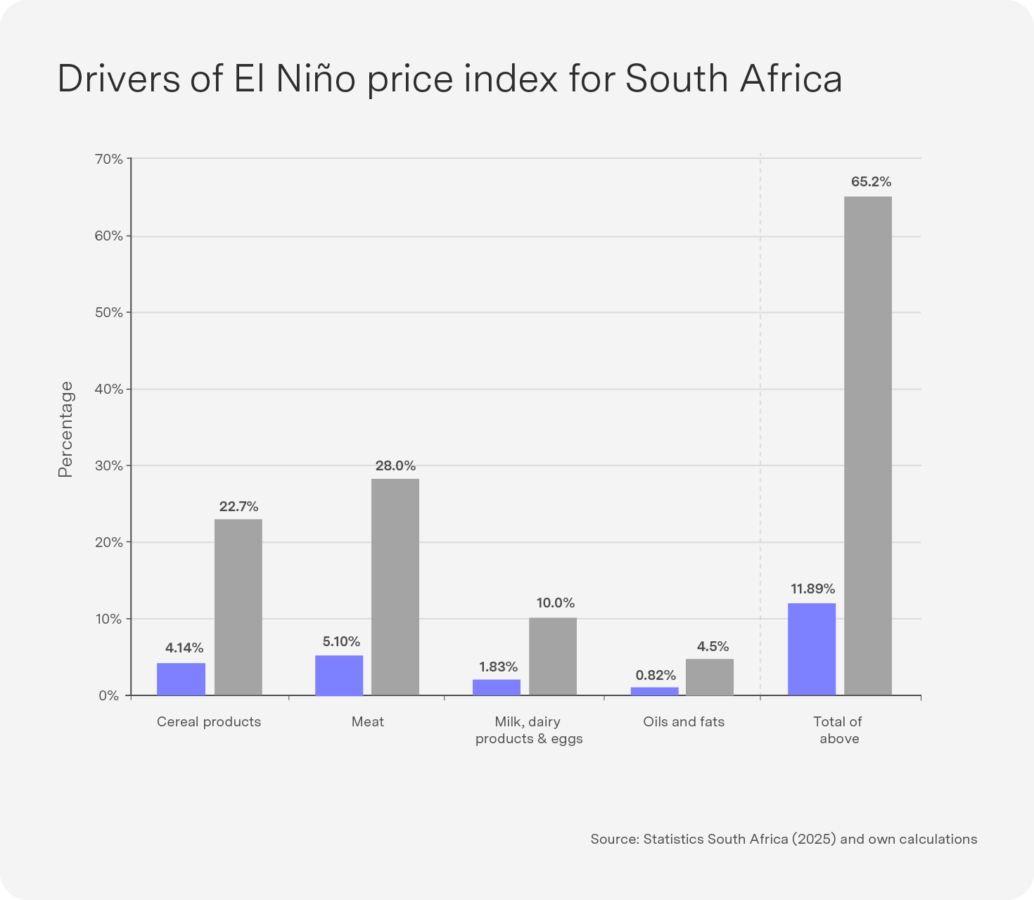

US inflation data for May offered little comfort to the interest rate outlook, with core inflation remaining elevated across multiple measures. The Fed’s preferred “supercore”, services inflation excluding housing, is rising sharply. The Atlanta Fed’s sticky-price gauge, which tracks goods and services whose prices adjust slowly and are difficult to reverse, has risen above 3%. Both the trimmed mean, which strips out outliers in either direction, and the median CPI moved higher (see Chart). It is little surprise that markets are pricing in a US rate hike as early as October.

While the Middle East conflict continues to dominate headlines, markets may soon refocus on trade policy. After courts invalidated tariffs imposed under the International Emergency Economic Powers Act and Section 122 earlier this year, the Trump administration is pivoting to Sections 301 and 232 as its primary legal instruments. Two new Section 301 investigations are underway: the first targets structural excess capacity across 16 economies, while the second covers forced-labour enforcement across 60 economies (South Africa included), where the US Trade Representative has floated tariffs of 10%–12.5%. Both investigations are broader in scope and faster moving than the China-focused measures of 2017–18. They do, however, carry legal risk: courts have shown a willingness to hold the administration to the statutory text of trade law rather than defer to the administration’s interpretation. If approved, the tariffs could exacerbate already stubborn inflation.

Strongest El Niño in 30 years has begun

New risks loom even as oil prices are falling, with the US Climate Prediction Center confirming that the El Niño conditions that emerged in May have continued to strengthen and are expected to peak over the northern hemisphere winter. Forecasters warn it could rival the major outbreaks of the early 1980s and late 1990s.

El Niño is a naturally recurring climate pattern that occurs every two to seven years, characterised by a warming of the Pacific Ocean that alters global weather patterns. The effects vary sharply by region: southern Africa and southeast Asia face prolonged drought and severe disruption to agriculture, while the Andean region of South America may bear the brunt of flooding. Top rice exporter India has already been hit by a delayed start to its monsoon season. South African corn, Malaysian palm oil and Australian wheat are all expected to be affected. Maize is an anchor crop and staple food for South African households and a central price signal for food inflation (see Chart), and the South African Reserve Bank may be forced to raise rates again due to El Niño-driven food inflation. The World Bank warned that El Niño could push food prices just as farmers are contending with the impact of the Iran war on fertiliser and fuel costs. Emerging market economies are more vulnerable to El Niño conditions given their dependence on agriculture and the high food shares in their CPI baskets.

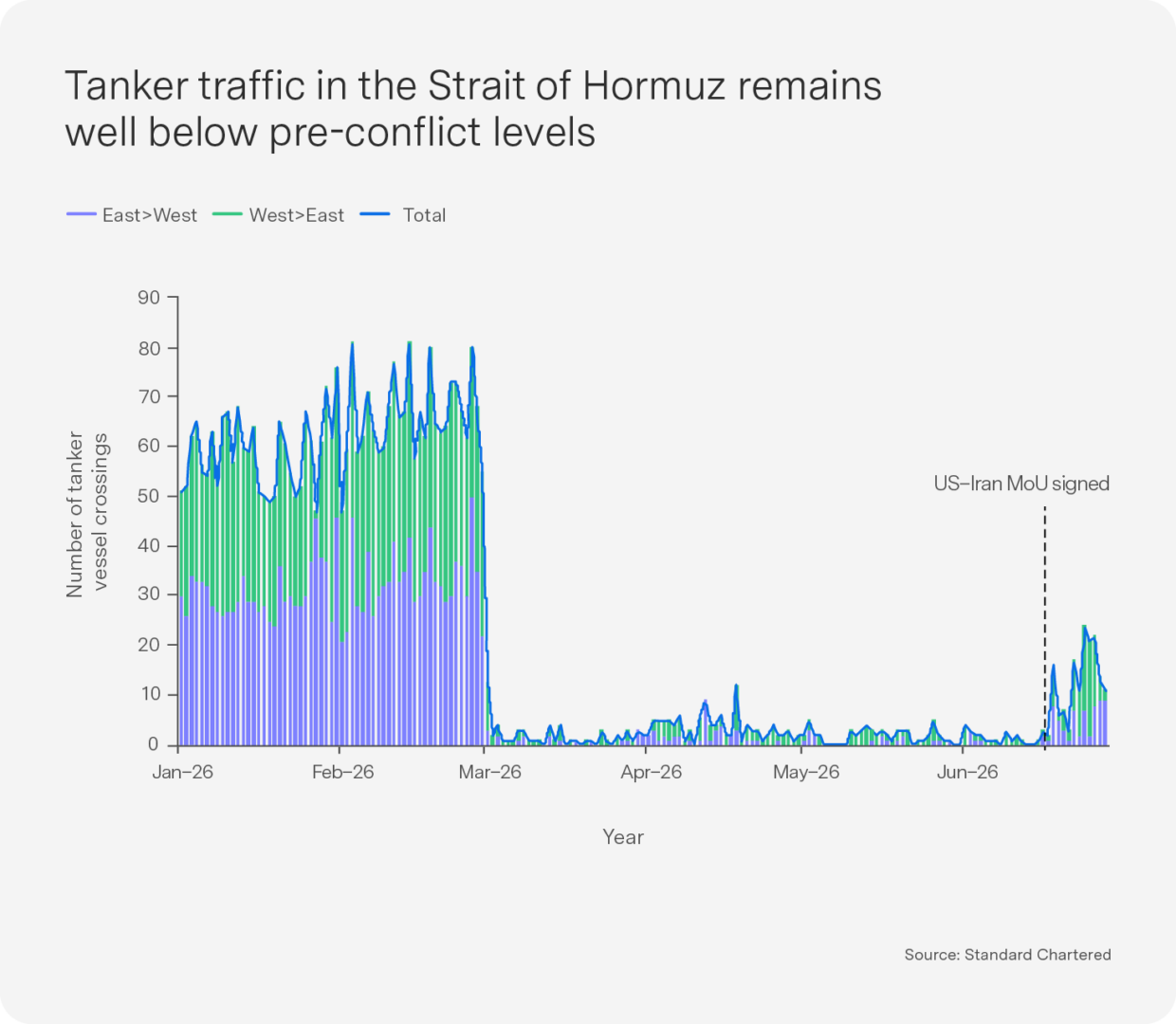

Outlook: Oil price falls but inflation remains elevated

The announcement of a memorandum of understanding (MoU) between Iran and the US caused the oil price to fall dramatically but has not altered our baseline forecasts. The oil price will remain elevated throughout 2026 relative to 2025 as geopolitical risks persist:

- A nuclear deal with Iran will be difficult to achieve without Trump agreeing to weaker terms than those secured under Obama’s 2015 Joint Comprehensive Plan of Action (which Trump scrapped).

- Reports of strikes in Lebanon continue, and it remains far from certain whether Israel and Hezbollah can sustain their temporary ceasefire.

- Red Sea traffic remains well below pre-conflict levels (see Chart) and is likely to remain below as insurance costs remain high; damaged facilities remain offline, and the UAE, for example, has declared its intention to reduce its Hormuz exposure to zero.

The World Bank has trimmed its 2026 global growth forecast to 2.5%, down from 2.6% in January, citing the economic drag from the Middle East conflict. Emerging market and developing economies are now anticipated to grow at 3.6%, a 0.4% downgrade. The US is the notable exception, holding steady at 2.2% – unchanged from January and marginally ahead of its 2.1% outturn in 2025.

Despite the conflict, growth has proven more resilient than feared. Global fiscal policy remains accommodative, effective US tariff rates have fallen and wealth effects remain positive, with markets at highs and the ongoing AI investment boom providing further support.

Central banks are navigating an increasingly difficult environment, however. Core inflation remains elevated and El Niño is expected to add further upward pressure through higher food prices, while future tariffs may lead to import inflation. With the US labour market now demonstrating renewed resilience, the Fed is likely to begin hiking sooner than anticipated to manage core inflation – a meaningful headwind for global equity markets. Emerging economies will continue to face a drag from higher energy and food prices as well as a hawkish Fed. We thus remain cautiously overweight global equities, neutral emerging markets and underweight South Africa.

Key indicators