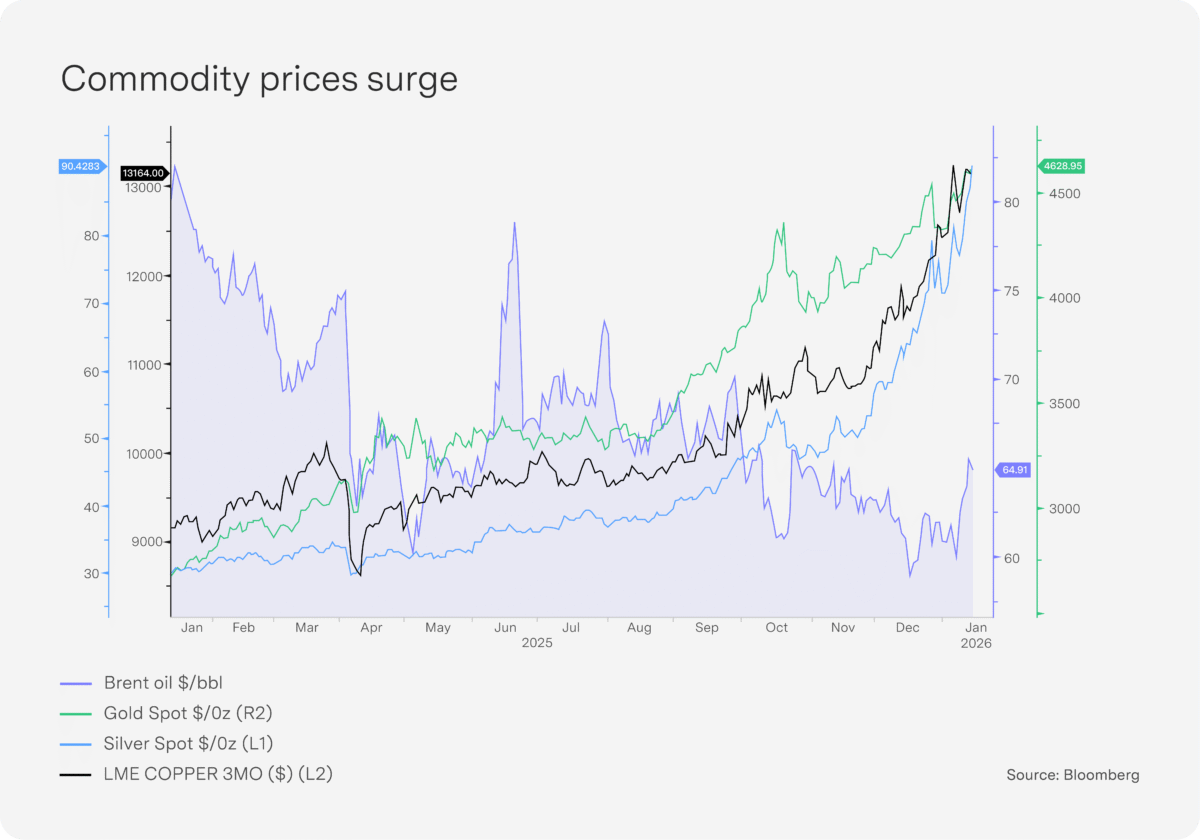

Commodity markets surge on geopolitical tensions and policy uncertainty

Metal and energy prices surged in January as investors navigated multiple global crises. Gold, silver, platinum, copper and tin reached new highs, while oil rebounded sharply. The rally stems from attacks on Federal Reserve (Fed) independence, tariff threats and escalating geopolitical tensions.

Fed under pressure: The Trump administration challenged the Federal Reserve’s independence, prompting a weaker dollar and a flight to commodities. Fed Chair Jerome Powell faces potential criminal charges about a headquarters renovation project. Former Fed chairs Janet Yellen, Ben Bernanke and Alan Greenspan condemned this as an “unprecedented attempt to use prosecutorial attacks to undermine [Fed] independence” and warned it could trigger inflation and economic instability. Separately, media reports indicate that the Supreme Court justices are sceptical of Trump’s arguments against Lisa Cook, suggesting she may remain on the Federal Open Market Committee and easing some concerns about Fed independence.

Oil rallies on Iranian crisis: Brent crude climbed above $70 per barrel amid Middle East supply fears. Mass protests have erupted across Iran. Trump suggested “very strong options”, including military action, and he announced a 25% tariff on any nation trading with Iran, directly affecting China and India – Iran’s top trading partners. Risks of a US strike on Iran are likely to sustain risk premia on oil prices after the arrival of the US aircraft carrier USS Abraham Lincoln and three warships in the Middle East.

Resource control disputes: Two separate conflicts have highlighted the growing importance of resource control.

- Greenland: Greenland holds strategic rare-earth deposits and military base locations. After threats to buy, annex or invade Greenland, Trump backed down on using force and retreated on proposed tariffs against European nations who opposed him. Trump still wants Greenland and claimed a “framework of a future deal”, but the Danes said the Greenland issue is not up for debate.

- Venezuela: Following the US’s capture of Nicolás Maduro, Venezuelan leader María Corina Rodríguez gave her Nobel Peace Prize to Trump while negotiating exclusive US oil access. Access to Venezuelan oil would enable President Trump to substitute Canadian heavy crude imports with a comparable alternative, while enforcing his proposed 100% tariffs on Canada. Challenges remain, however, as Maduro loyalists retain influence and reviving output to pre-2019 levels of about 2 million barrels/day would require major Western investment – unlikely given the political uncertainty. The action also risks escalating US-China tensions, as China is South America’s top trading partner. The combination of geopolitical instability, trade policy uncertainty and challenges to central bank independence has created an unusually volatile environment for the dollar and commodity markets. Notably, though, the liquid bond market is not showing material signs of inflation from either the commodity price increases or fiscal largesse associated with the debasement trade, suggesting that most of January’s events were sabre rattling and distractions – if that is the case, the less liquid commodity markets should expect a pullback.

The year of living dangerously? Looking ahead to 2026

Who would have thought that the year would begin with a regime change in Latin America openly engineered by the USA – with the fairly direct promise of more to come from the Trump presidency? If we consider this new “Donroe” doctrine of the US with the current pressure on the Fed Chair’s job and at least one of his fellow Board members, together with the “how high will it go” uncertainty of the ongoing Trump tariffs, 2026 will undoubtedly be significant for the world economy.

For a small, open economy such as South Africa, where we are essentially price takers, such uncertainty offers both opportunities and constraints for economic growth and financial markets.

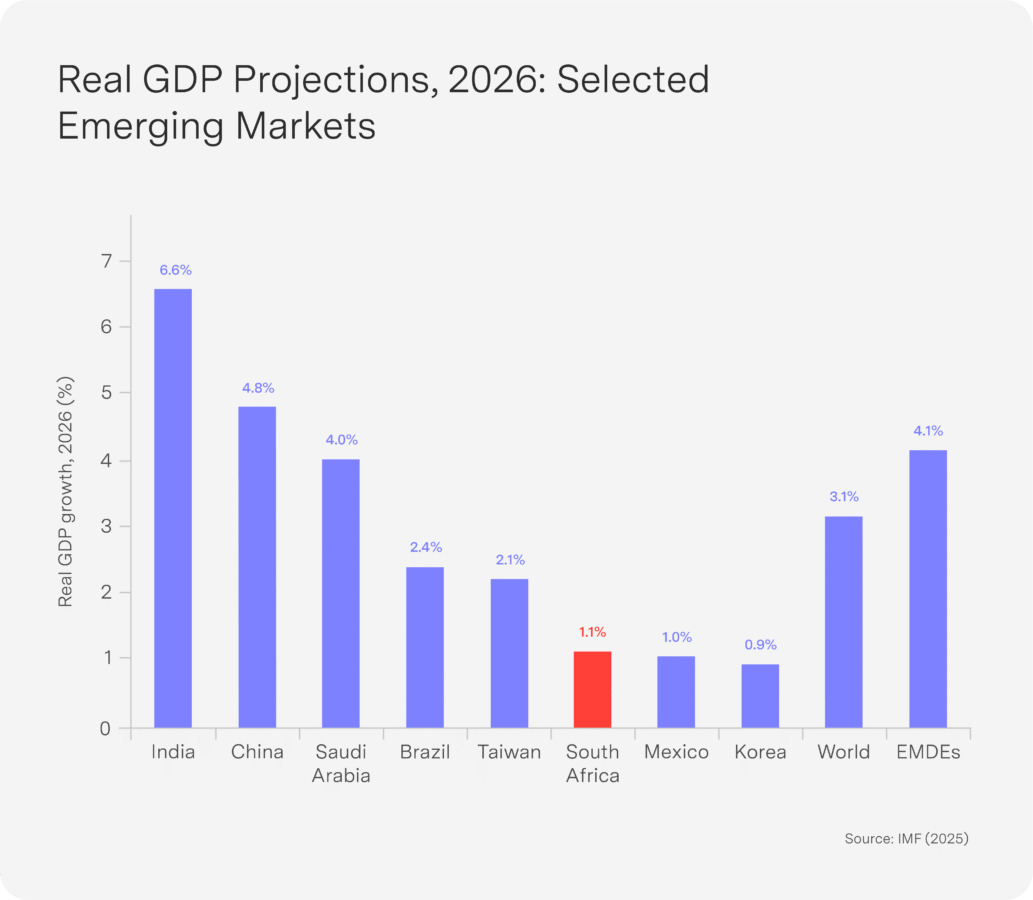

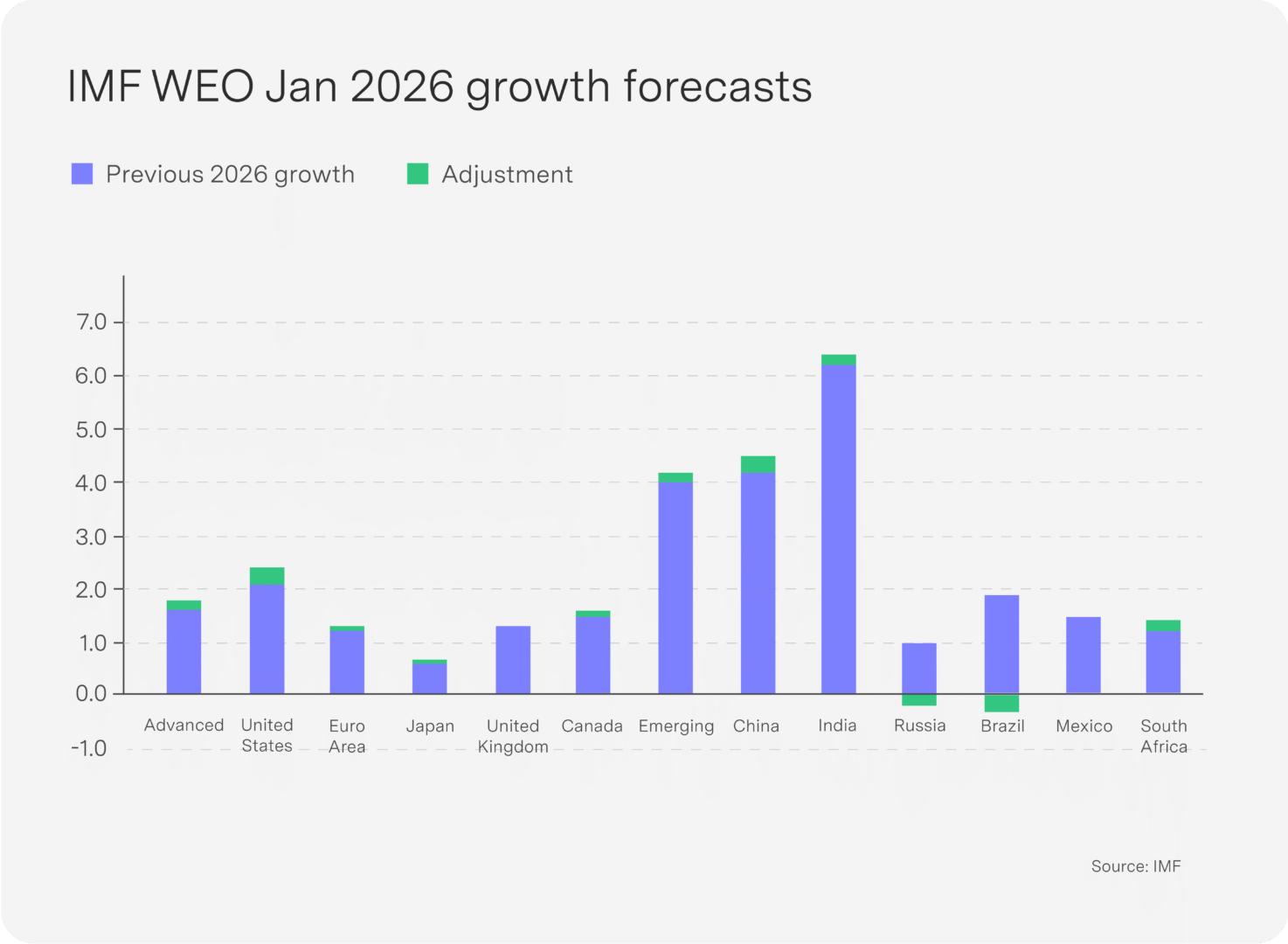

Estimates across different models for 2026 suggest moderate GDP expansion in the 1.1–1.5% range. Notably, however, the International Monetary Fund (see Chart) reports that we are growing slower than our emerging market comparators. Brazil is expected to post 2026 GDP growth rates more than double those of South Africa’s, while the overall mean growth rate for emerging markets and developing economies is four times South Africa’s. This lower relative growth has always been a South African feature but has worsened post- Covid and more broadly in the wake of the Zuma presidency. Our growth prospects are not helped by Europe’s – and to some extent the US’s – economic struggles, while China’s previous double-digit growth rates look to have moderated in the short term. Our major trading partners will have to grow faster to kick-start South Africa’s own GDP prospects. The continued weakness of the dollar is good for import-intensive industries and may add to domestic price moderation. Although the US House of Representatives has approved a three year extension to the African Growth and Opportunity Act (until 2028), separate bills proposing South Africa’s exclusion are subject to a debate in the US Senate.

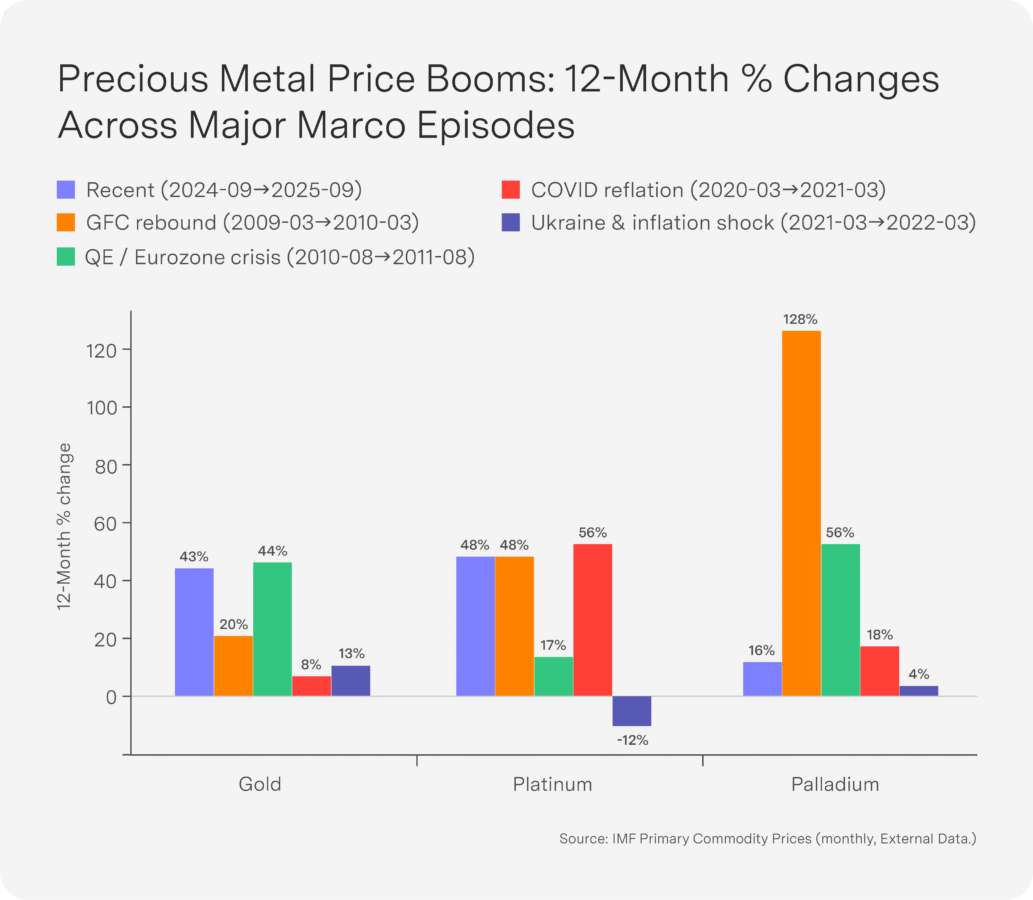

But in uncertainty, opportunities arise – and nowhere is this more true than in the commodities market. As a key exporter of gold, platinum and palladium, the surge in these metal prices is positive for resources equities, the Johannesburg Stock Exchange and South Africa’s real economy. Increased metals production will have downstream economy-wide effects and will remain a crucial underpin for our growth prospects in 2026. This price surge is like others we have seen in recent times (see Chart ), though the gold price surge is noteworthy. The uncertainty around US monetary policy, tariff adjustments (which will raise metals prices for US importers) and demand for new hybrid vehicles are all likely to continue into 2026. Add already high levels of geopolitical uncertainty, and commodities demand and prices are likely to remain elevated in 2026. While gold will play a role here, South Africa’s true gains at the real economy level will be in its holdings of 78% of global reserves of platinum group metals and 90% of rhodium reserves. The commodities boom will not be sufficient to elevate growth above 1.5%, however.

Monetary policy is doing its part for macroeconomic stability and growth prospects, and we enter the first full financial year with a lower inflation target of 3% with a ±1% tolerance band, which will serve us well in terms of wage moderation, consumer well-being and foreign investor sentiment. Inflation dynamics do still run the risk of being driven by logistics bottlenecks, administered prices, disease outbreaks and ever-present but unpredictable climate-related shocks. Inflationary expectations going into 2026 are well anchored, harkening back to the early years of our democracy when we were top of our class in macro stability!

The improved debt outlook (in terms of both stock of debt-to- GDP and servicing costs), a lid on the public sector wage bill and exiting the Financial Action Task Force’s grey list have improved our sovereign ratings outlook, providing more positive momentum into 2026. However, this frugal fiscal environment will deprive the domestic economy of much needed public capital expenditure, compounded by very high levels of public consumption and socialservices- related expenditure. This skewed ratio of consumption relative to capital expenditure by government remains a brake on higher levels of supply-side driven growth. Only higher growth can resolve this low public investment conundrum, and government will have to focus on its policy reform package around, for example: deregulating the business environment for small and medium enterprises; taking the positive Eskom momentum of 2025 into infrastructure areas such as water and transport; maintaining the focus on anti-corruption and good governance; and ensuring that trade-related negotiations protect local industries in key job-generating industries such as agriculture, automobiles and telecommunications.

Late 2026 is also an election year, and the ANC has generated clear election-related momentum around service delivery since the beginning of the year. The recent Presidency announcement of over R1 billion capital expenditure on service delivery and infrastructure investments is evidence of a search for broader-based economic growth and development that can only be a boon to economic growth and development prospects. South Africa is on track for positive but low growth in 2026. The global uncertainty that is driving a weak dollar, commodity price hikes and possibly even equity price weakness in developed markets signals stronger opportunities for economic growth in South Africa. As long as our domestic factors – many of which are controllable – are complementary, GDP growth may even surprise on the upside this year.

Top-performing Sygnia funds

South Africa is rallying alongside the other emerging markets, supported by a weaker dollar and strong commodity prices. South African equities dominated over one month and one year. The Top 40 Fund is in top place over 12 months with its large exposure to gold and platinum stocks. The Transnational Fund is also producing great returns but is lagging the Top 40 due to its more diversified resource portfolio.

1-month absolute performance

- Sygnia Top 40 Index Fund 9.4%

- Sygnia Itrix MSCI Emerging Markets 50 ETF 8.9%

- Sygnia Itrix Top 40 ETF 7.5%

- Sygnia Divi Index Fund 7.2%

- Sygnia Transnational Equities Fund 5.4%

12-month absolute performance

- Sygnia Top 40 Index Fund 55.5%

- Sygnia Itrix Top 40 ETF 53.1%

- Sygnia Itrix MSCI Emerging Markets 50 ETF 35.3%

- Sygnia Listed Property Index Fund 35.0%

- Sygnia Transnational Equities Fund 33.2%

US dollar: Strong fundamentals despite political turbulence

President Trump commented that “the dollar’s doing great” when it hit a 4-year low in January. Markets interpreted this as confirmation that he wants a weaker dollar, which led to further dollar weakness and strength in gold prices. However, the dollar strengthened on news that Kevin Warsh is the favourite to replace Jerome Powell as Fed Chair, as markets view him as a prudent choice favouring tighter policy. Political noise aside, productivity growth, favourable yield spreads and improving inflation dynamics support a stable to stronger dollar through 2026.

Productivity growth supports dollar strength: US labour productivity surged 4.9% in Q3 2025 and is projected above 2% for Q4. These productivity gains are more than offsetting weaker employment growth. When the US has enjoyed superior productivity growth relative to other countries in the past, like the 1990s internet boom, this has translated into higher real incomes, a stronger real exchange rate or both.

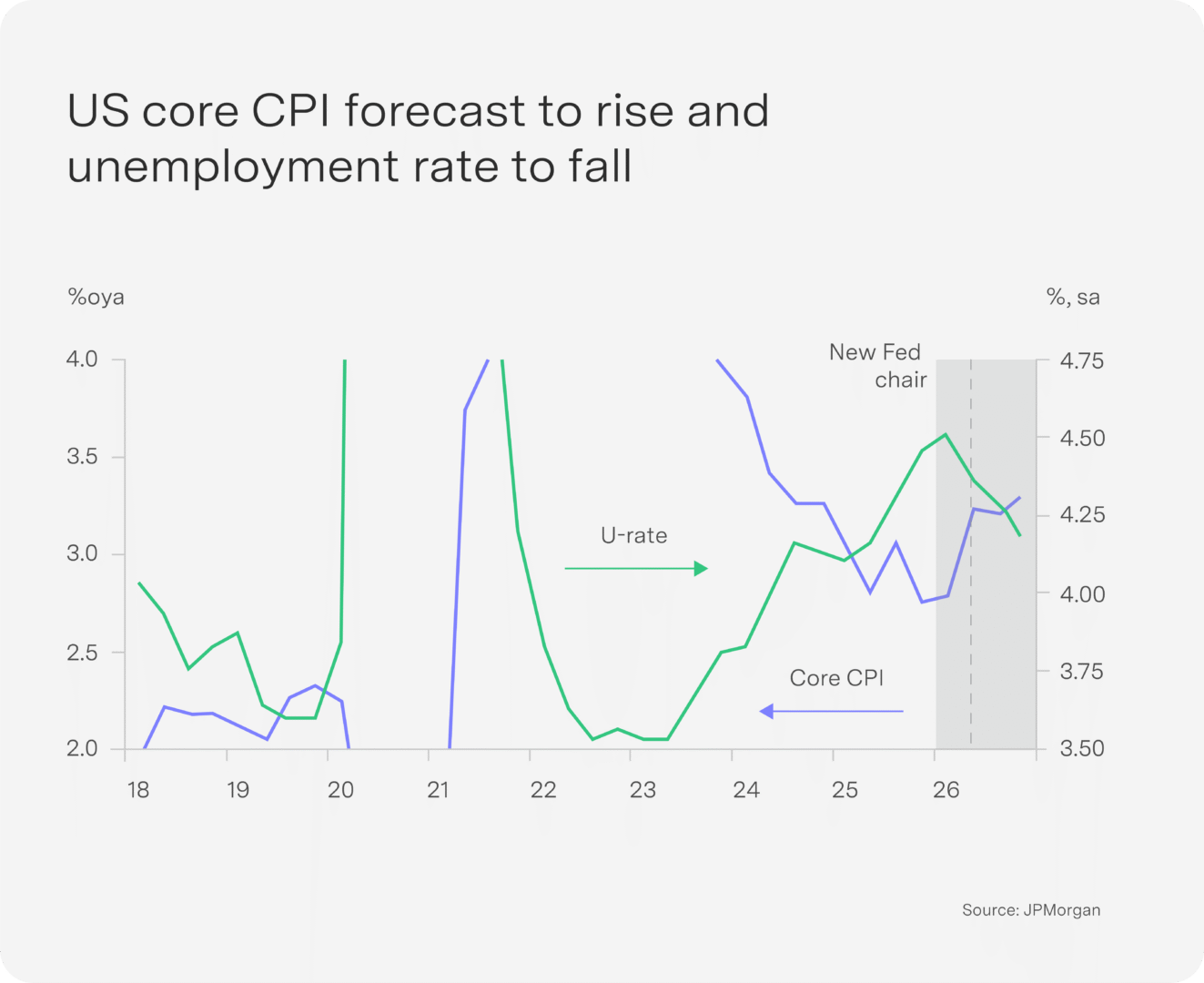

Bond yields signal an undervalued dollar: Short-term bond yield spreads between the US and Germany suggest the euro should trade near $1.12–1.13, but it is currently closer to $1.18. For the dollar to weaken meaningfully, US monetary policy would need to become far more dovish – unlikely in the first half of 2026. Employment data may be stronger than initially thought after December’s unemployment rate dropped to 4.4%, beating expectations. The Fed paused interest cuts in January. As employment growth recovers alongside strong economic growth, the Fed pause could extend, particularly as tariff-driven inflation will take time to unwind. JPMorgan estimates core CPI will rise to 3.4% by May 2026.

Longer-term inflation relief ahead: Beyond the first half of 2026, productivity gains could reduce inflation pressures. AI is a labour-saving technology, enabling firms to produce equal or greater output with fewer workers. While challenging for employment, this benefits inflation control. Additional inflation relief may come from housing costs. Owners’ equivalent rent has declined sharply in recent months. This would give the Fed scope to cut later in 2026.

China: Export strength masks weak domestic demand

China’s economy slowed further in Q4, with GDP expanding by 4.5% year-on-year, down from 4.8% year-on-year in Q3. Despite this moderation, full-year GDP growth reached 5.0%, aligning with the government’s target. However, this achievement relied heavily on exports as domestic demand remained weak.

China’s export sector remains resilient despite trade tensions, with exports rising 6.1% and imports increasing just 0.5%. This represents a remarkably strong performance given that exports to the US fell 20%. China compensated by diversifying its export markets, particularly in Asia and Europe. Exports to the latter surged 8.4%, which will likely increase deflationary pressure on European economies.

Private-sector investment as a share of economic activity has declined sharply in recent years and has triggered widespread job losses and weaker household consumption, creating a negative feedback loop. Fortunately, corporate hiring intentions have begun to improve, offering hope of reversing the downward spiral. Declining investment suggests that additional policy support is likely.

Market outlook: Bull market intact but entering mature phase

The International Monetary Fund lifted its global growth forecast for 2026 to 3.3% (from 3.1% in its October World Economic Outlook (WEO) update) due to stronger-than-expected AI tech investments. The biggest 2026 growth increase in developed markets was for the US, where growth was upgraded by 0.3% to 2.4%. The biggest emerging market increase was for China, which saw its growth upgraded by 0.3% to 4.5%. The South African GDP growth forecast was lifted by 0.2% for 2026 to 1.4%.

Above-trend global GDP growth should persist in the first half of 2026 as recovering business sentiment boosts job gains and non-tech business spending. The consumer provides the foundation, having maintained steady spending despite last year’s near-stall in job growth. With improving global growth, the equity bull market is continuing, but it is no longer in its early stages. Increased volatility and sharp corrections are likely in the first half of 2026, with a broadening rally expected as monetary easing and AI applications expand beyond the tech sector.

Geopolitical threats will add short-term market volatility and support commodity prices. The US violation of international law in Venezuela puts an interesting light on the China/Taiwan dispute and Russia/Ukraine war, with The Trump administration indicating that US security guarantees are likely to be contingent on Kyiv agreeing to a peace deal that cedes the Donbas region to Russia.

Escalating weather events are also affecting commodity prices, with US natural gas jumping 20% on the recent arctic storms. Commodity prices are overbought and risk a pullback, but they will drive inflation higher if they remain elevated – which would create a challenging environment for central banks seeking to ease policy and for markets relying on low interest rates.

Key indicators