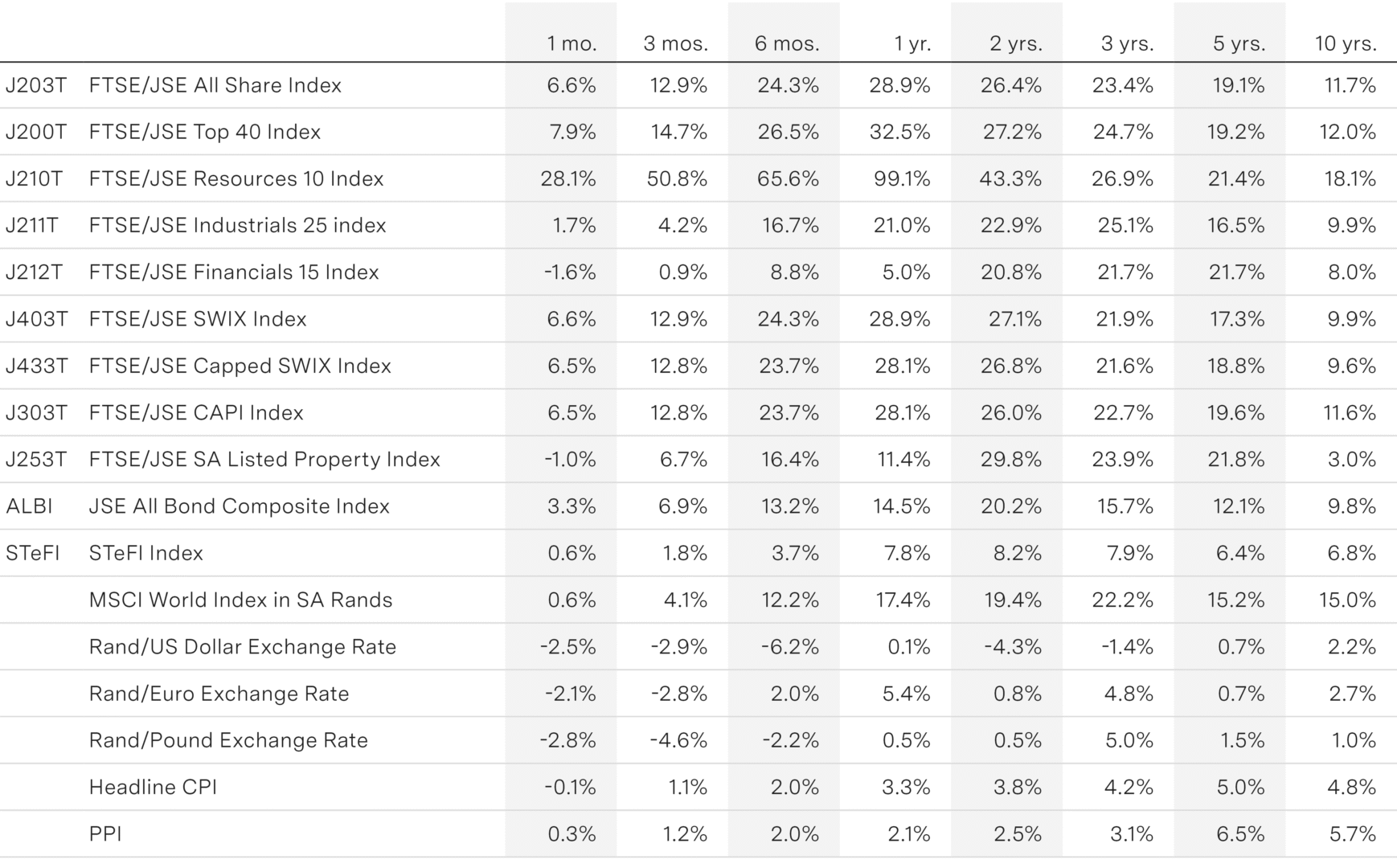

Gold rockets to record highs amidst looming US shutdown

The gold price surged more than 10% in September, pushing the real (inflation-adjusted) gold price to an all-time high, surpassing its 1980s peak. Gold’s weighting has reached 15% of the JSE All Share Index, nearly three times its 2006 peak; including platinum group metals, total precious metals now account for 22% of the SA equity market, pushing the South African resources sector to more than double year to date.

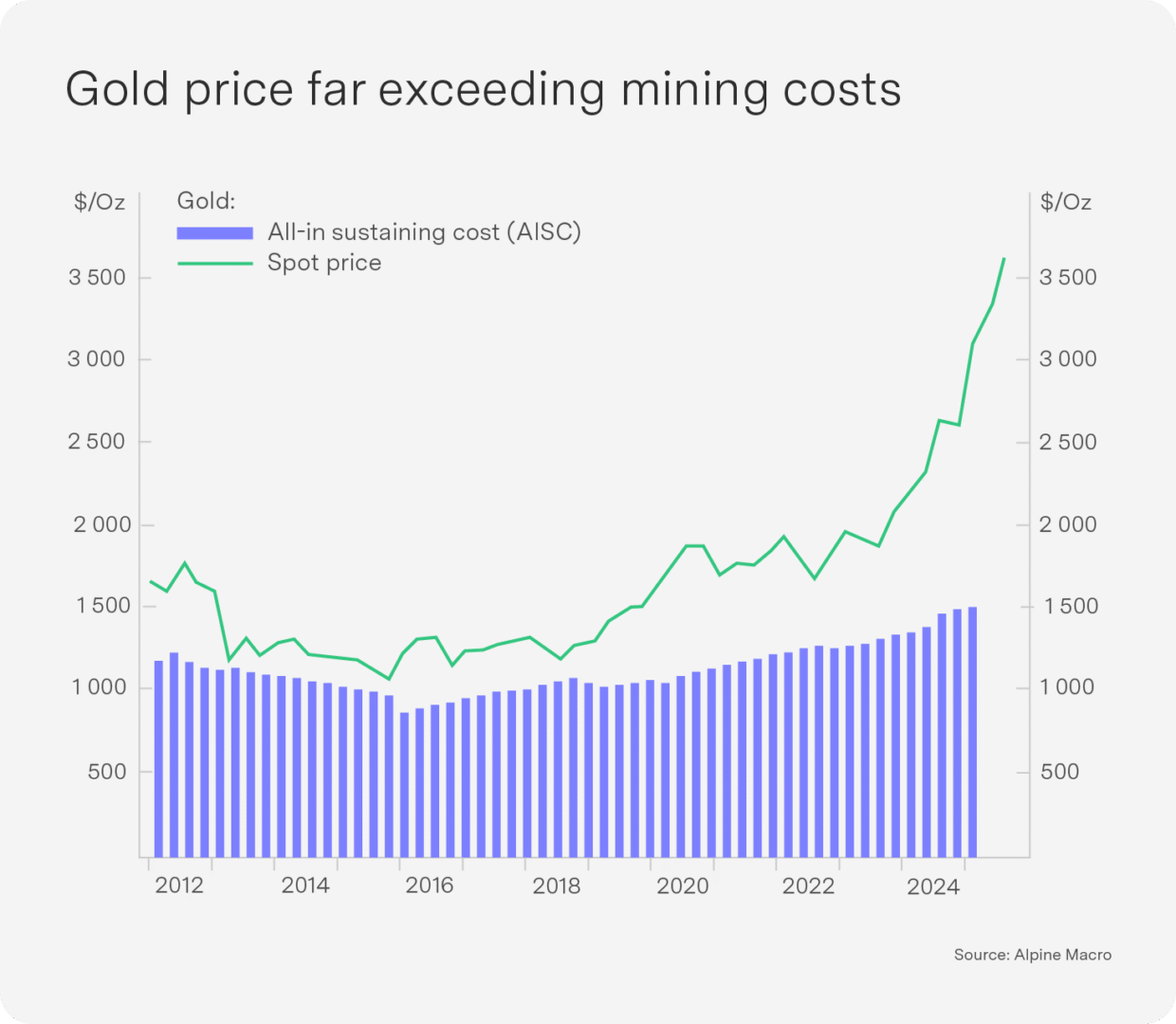

So what is driving the gold price? Traditionally seen as an inflation hedge, gold’s link with consumer price index (CPI) inflation has weakened and even turned negative since the 1990s. Gold’s anti-dollar correlation also broke down after 2018, surging alongside a strengthening dollar. Similarly, its historically inverse relationship with real bond yields vanished post-2022, with real yields rising sharply even as gold prices kept climbing. While geopolitical tensions and trade policy uncertainty remain high, pushing gold up as a defensive hedge, gold prices have outpaced over the last six months despite these uncertainty measures peaking in April this year. Another potential anchor to the gold price is mining costs, but at around $1 500 an ounce, these are 60% below the spot price (see chart), suggesting that in the long term, mine expansions and a recycling of secondary inventories will increase supply. Monetary factors have also traditionally played a critical role in the gold price, but even the gold-to-money supply ratio has reached levels that historically precede sharp corrections.

Gold’s remarkable rally has been driven by a shift to a polarised world and currency debasement fears as US President Trump shapes a new economic reality. Price-insensitive central bank gold purchases by member nations of BRICS and the Gulf Cooperation Countries have skyrocketed since the Russia-Ukraine war, and specifically since the freezing of Russia’s dollar reserves by the West. These central banks hold only about 7% of their reserves in gold (compared to 25% globally), reflecting potential for more buying. Meanwhile, global investors are growing increasingly concerned about dollar debasement as pressure mounts on the Federal Reserve to accept higher inflation amidst rising debt levels.

The Federal Open Market Committee’s (FOMC’s) implicit acceptance of a higher inflation target appears to be weakening the independence of the Fed. The Trump administration’s suggestion to fund the rapidly expanding additional government debt through short-term government paper (a strategy known as fiscal dominance) has further weakened credibility. This has driven global exchange traded fund investment holdings of gold to a year to date high of 96.7 million ounces. Net speculative positioning is also a bullish extreme.

Gold performed well in the 2018/2019 US shutdown, and the short term the rise in gold has likely been driven by investors seeking safe-haven. Beyond the shutdown, emerging market (EM) central banks are likely to continue to buy gold and Trump will continue his attacks on the Fed, so gold’s rally is likely to continue, further boosting South African equities. However, the stretched price of gold has raised the risk of a short-term reversal. The dollar may be nearing a bottom, with expectations for Fed rate cuts looking overstated, and US fiscal concerns could ease somewhat due to tariff revenues running at an annualised $375 billion. Additionally, newly appointed Fed member Stephen Miran has flagged the Fed’s third mandate, a long-forgotten clause that requires the Fed to “maintain moderate long-term interest rates”, which may reduce the extent to which the US government tries to indirectly manipulate the Fed. While gold is likely in bubble territory (and bitcoin as digital gold), we remain overweight SA equities due to gold’s momentum but are maintaining a tight stop loss.

Are economic policy reforms on track?

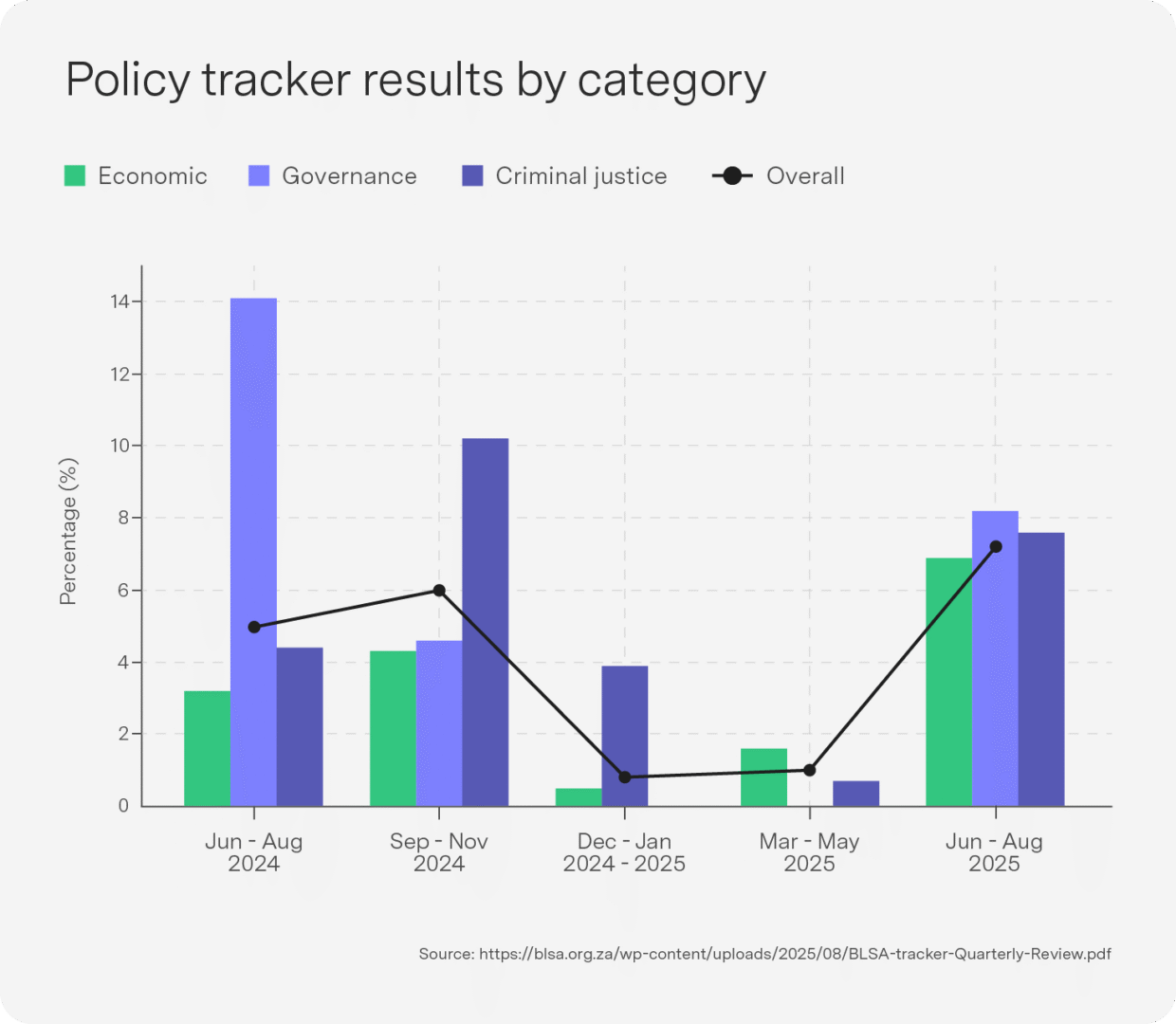

It can be difficult to track the policy reforms government implements to kick-start much needed economic growth in the country. To assess whether policy changes around ports, electricity, crime and so on are not only appropriate but evolve rather than stall, the recently released policy tracker by Business Unity South Africa (BUSA) is particularly useful in condensing the different strands of economic policy into a single measurable index of progress. The tracker provides a systematic assessment of reform implementation in areas such as electricity, rail & ports operation, crime and more by evaluating deliverables across four detailed stages of policy implementation: agenda setting, planning, action and effectiveness. This allows for a granular understanding of how reforms evolve, where they stall and how their outcomes affect the wider economy.

The headline result based on the latest evidence for the period up to August 2025 is that we have witnessed the strongest reform momentum since tracking began in the areas of economic policy, governance and criminal justice. Positive news, then! Specifically, of the deliverables being monitored and measured, the majority were completed at least a year ago, with the most visible progress in the energy sector. The end of regular load shedding in March 2024, achieved through reforms such as the removal of licensing thresholds for private generation and improved Eskom maintenance, represents a major success. However, the tracker highlights the layered onion problem, as each achievement exposes further challenges. For example, long-term energy security is dependent on building 56 GW of new capacity and 14 000 km of transmission lines – much of which will require private investment under the newly created National Transmission Company. So as we exit regular loadshedding, we may face new obstacles around green energy generation. In addition, municipal debt continues to compromise energy reforms, with R94.6bn owed to Eskom by early 2025 despite debt-relief programmes. This debt is a core liability on the fiscus.

Transport reforms have been slower, though institutional restructuring is underway. The unbundling of Transnet into an infrastructure manager and a freight operating company, combined with new frameworks for private participation, signals a shift to a more competitive logistics system. Nevertheless, operational failures – from idle locomotives to persistent cable theft – continue to undermine efficiency. Port performance remains among the worst globally, with South African facilities ranked near the bottom of international indices. Without tariff clarity and stable financing, the promise of logistics reform could stall. Transport reforms are thus steady but show slow progress.

Climate and environmental policy have also built momentum. The Climate Change Act came into effect in 2025, embedding net-zero commitments into law, while new Nationally Determined Contributions propose emissions reductions to 320–380 MtCO2e by 2035. International partners nevertheless remain concerned that South Africa’s targets will fall short of Paris Agreement goals, while the disbursement of pledged Just Energy Transition funding has been limited. This could be problematic should South Africa, for example, fail to meet new trade requirements on climate change in its key markets – most notably in the European Union.

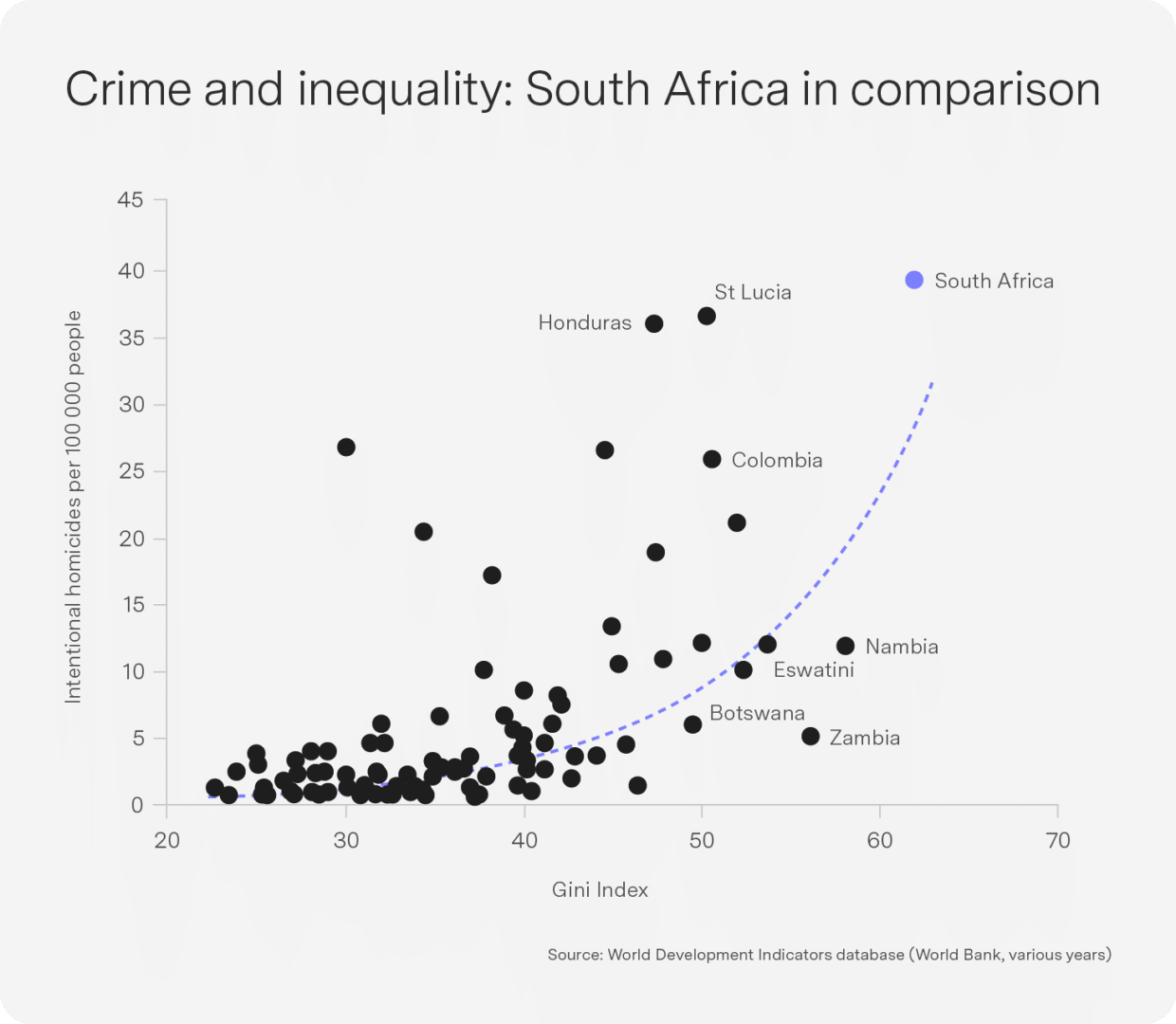

The BUSA tracker shows that criminal justice reforms have been strongly shaped by South Africa’s response to the Financial Action Task Force (FATF) grey listing. By June 2025, the government had completed all 22 action items required for compliance, including strengthening the Financial Intelligence Centre, improving beneficial ownership transparency and enhancing supervisory and prosecutorial capacity. This represents a significant milestone in restoring international financial credibility and could lead to the country’s removal from the grey list by October 2025. This significant achievement will ensure that a core determinant of the cost of doing business in South Africa is under control. Perhaps the most important obstacle to growth in this area, however, is the continued inability of the relevant authorities to fight violent and non-violent crime. As the figure below reminds us, South Africa stands out as one of the most criminally violent countries in the world, even among other highly unequal economies. It would be beneficial were the BUSA tracker to track reform progress in this arena as well.

While we cannot claim to be living in a “failed state”, state capacity is still struggling to recover from the vestiges of the state capture era. The BUSA tracker confirms that governance reforms have had the least momentum: Cadre deployment remains unaddressed and implementation is very slow, despite proposals informed by the Zondo Commission to professionalise the public service through merit-based recruitment and reduced political interference. Lifestyle audits and enforcement are expanding, though their deterrent effect is unproven. On the positive side, immigration reform has advanced rapidly after years of inertia: Home Affairs has cleared about 90% of its visa backlog, introduced a points-based system for critical skills, implemented a digital nomad visa and expanded e-visas, better aligning policy with business and tourism – evidence that progress follows when political will meets capacity.

Overall, the August 2025 BUSA policy tracker allows us, with some data intelligence, to be cautiously optimistic about reform and progress in areas such as immigration, energy and financial regulation. Key constraints include state capacity, rail & ports and crime management. Perhaps underemphasised by the tracker is the looming crisis of municipal debt and general municipal governance failures. As always, many of the needed reforms are feasible provided the political commitment is there.

Top-performing Sygnia funds

Technology investment in AI continues to be the primary driver of global markets, specifically China’s stock market, where the technology index is rapidly catching up to US tech after announcements of stronger-than-expected AI investment from Alibaba and technology progress from Baidu, both up almost 50% in September.

1-month absolute performance as at 29 September 2025

- Sygnia Itrix MSCI Emerging Markets 50 ETF 8.9%

- Sygnia Top 40 Index Fund 7.4%

- Sygnia Itrix Top 40 ETF 7.1%

- Sygnia Itrix MSCI China Feeder ETF 6.0%

- Sygnia Enhanced All Bond Fund 3.7%

Technology companies in Taiwan and Korea drove EMs to the 5th fund position in the 12-month table, but US FANG.AI stocks remain ahead of EMs.

12-month absolute performance as at 29 September 2025

- Sygnia FANG.AI Equity Fund 37.0%

- Sygnia Itrix FANG.AI Actively Managed ETF 36.6%

- Sygnia Itrix Top 40 ETF 31.2%

- Sygnia Top 40 Index Fund 30.5%

- Sygnia Itrix MSCI Emerging Markets 50 ETF 29.4%

US: Federal Reserve implicitly targets 2.8% inflation

The Fed lowered interest rates by 25 basis points, marking its first rate cut in 2025 amid emerging signs of a softening in the labour market. However, the Fed’s Summary of Economic Projections (SEP) for 2026 showed an upgrade in growth expectations, raising GDP growth from 1.6% to 1.8%, increasing core personal consumption expenditure (PCE) inflation forecasts from 2.4% to 2.6% and lowering the unemployment rate from 4.5% to 4.4%. The combination of a rate cut alongside upgraded growth and inflation forecasts has raised investor concerns about Fed credibility and dollar debasement.

Fed Chair Jerome Powell described September’s rate cut as “risk management”, but Bloomberg Economics suggests political pressure may have influenced the decision. The SEP and Fed rate cut forecasts suggest a Fed inflation target around 2.8%, higher than the Fed’s official 2% target, raising the risk that this implicit inflation bias could shift even higher as the composition of the FOMC changes under Trump.

The market’s expectation of two further interest rate cuts this year and three more next year seems unlikely, as several factors underpin the resilience of the economy. Interest rates have started to fall, the US dollar has weakened and oil prices remain well below recent highs. Corporate earnings are positive, and the ISM Services New Orders Index surged to 56 in August – its highest level in a year. Expectations of banking and energy deregulation, improved productivity and fiscal stimulus from the One Big Beautiful Bill Act support growth entering 2026. Retail sales remain strong, but stable growth also means inflationary pressures will persist. The ISM Services Prices Paid Index stayed above 69 for the second consecutive month in August, with 14 tariff mentions, historically a three-month leading indicator for CPI. August’s headline inflation surprised on the upside and food prices hit their highest level since January 2023, adding to concerns about rising consumer inflation expectations. Household surveys confirm that long-term inflation expectations are climbing.

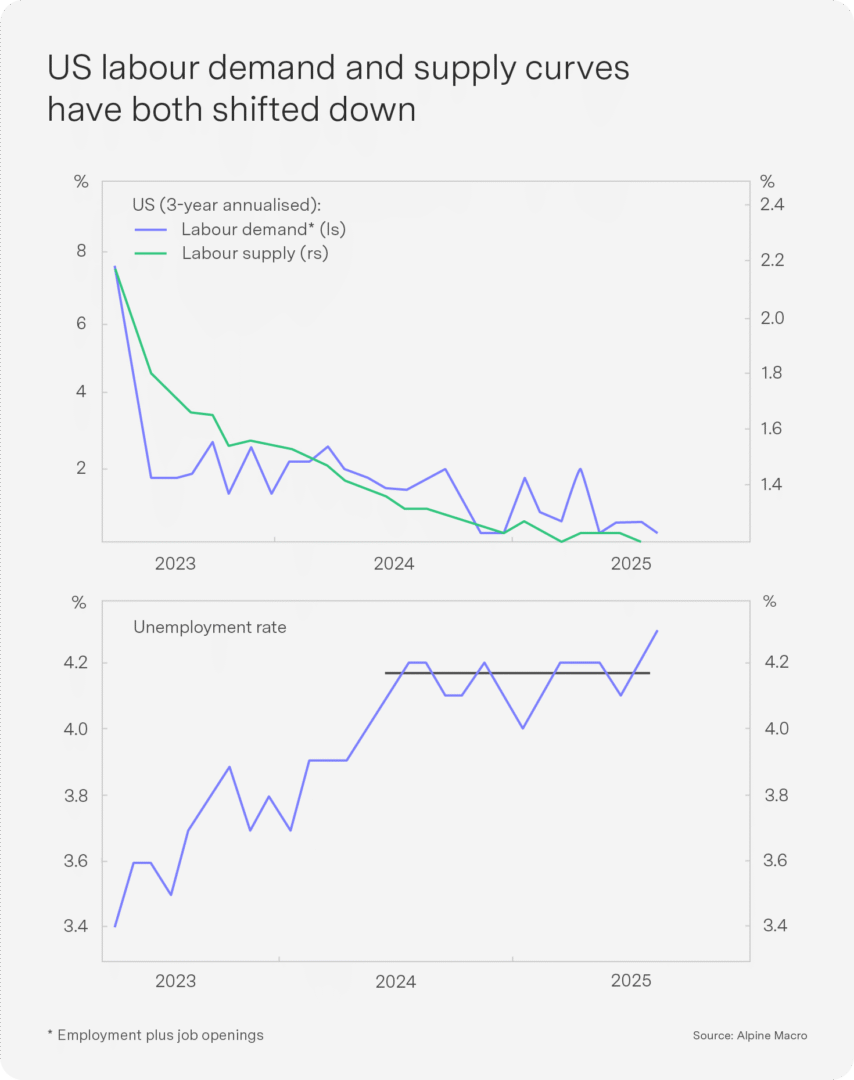

Finally, although the 5 September payroll report showed a significant drop in employment growth, the unemployment rate only ticked up slightly, to 4.3%. This is because breakeven payroll gains (jobs needed to keep unemployment stable) have dropped as a result of a shrinking labour force caused by lower participation and the increased deportation of undocumented workers (see chart).

China: Xi pushes for a bipolar world while maintaining negotiations with the US

Chinese President Xi Jinping hosted a two-day summit in China, where he called on regional powers, including Russia, North Korea and India, to join China in leveraging their economic influence to counterbalance the West.

Soon afterwards, Xi and Trump apparently made progress on several bilateral issues, including trade, fentanyl, the conflict between Russia and Ukraine and a TikTok deal. Trump approved a framework to keep TikTok operational in the US by addressing ownership concerns, with officials working towards final approval from Beijing. Xi urged the US to avoid unilateral trade restrictions and to maintain a fair business environment for Chinese companies. China is also pushing for a harsher stance from the US on Taiwan, but the US has not yet responded.

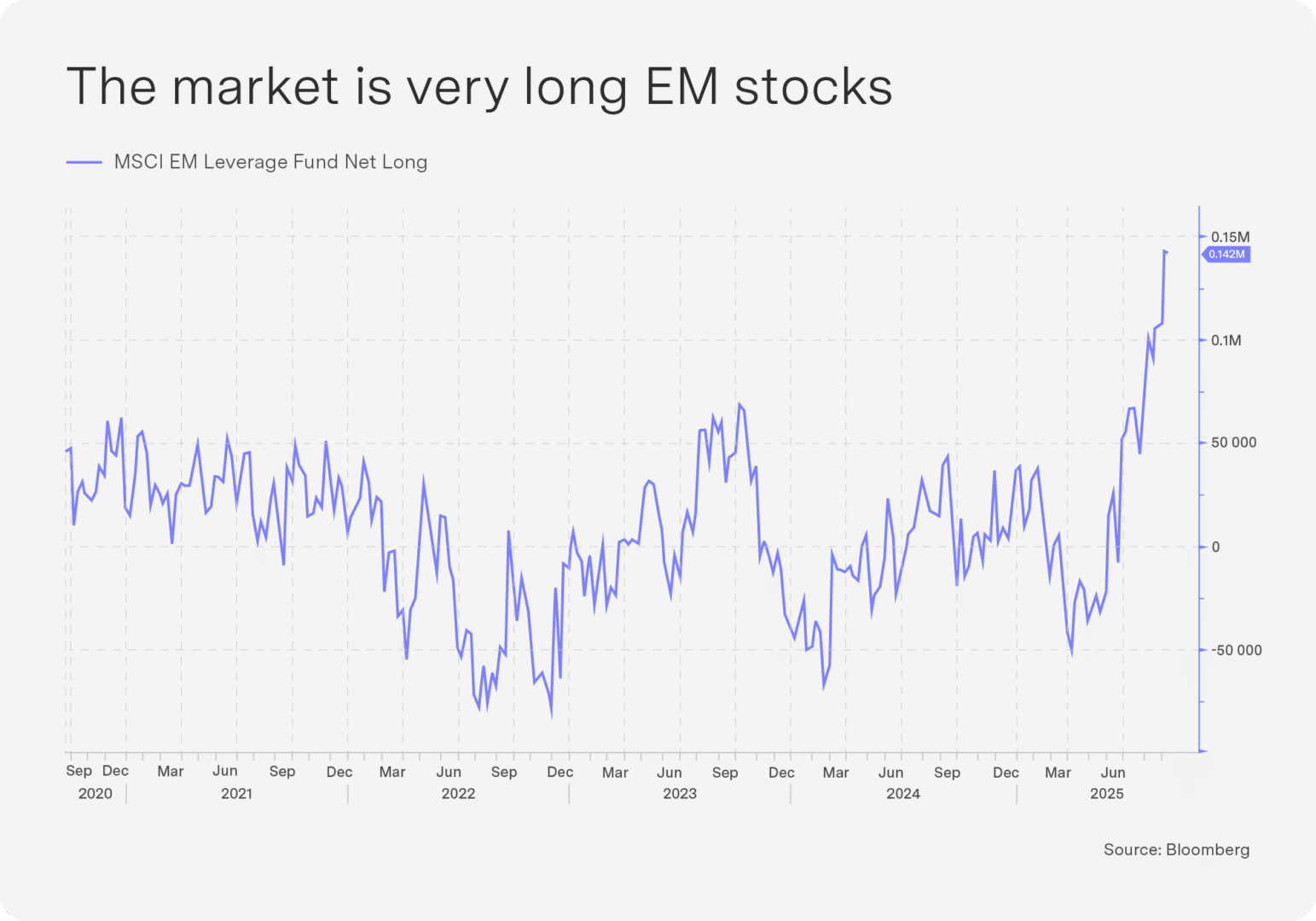

EM performance has been excellent this year, with EM equities up 27% in dollars year to date and EM local currency bonds up 15%. This is due to EM technology exposure, particularly around semi-conductors in Taiwan, Korea and China, and stronger EM currencies due to lower EM inflation, allowing EM central banks to cut interest rates. However, the market has become very long EM stocks based on futures holdings (see chart).

Geopolitical noise and risks remain high

The oil price spiked after US President Trump reversed his stance on Ukraine, writing on social media: “I think Ukraine, with the support of the European Union, is in a position to fight and WIN all of Ukraine back in its original form.” At a separate meeting with France’s President Emmanuel Macron, Trump said “Russia should have stopped” the war in Ukraine. He also called on NATO nations to shoot down Russian aircraft that violate sovereign airspace and called on European economies to stop purchasing oil from Russia.

Poland shot down 19 Russian drones that entered its airspace during a massive Kremlin airstrike on Ukraine, calling the trespass an “act of aggression”. Polish Prime Minister Donald Tusk subsequently invoked NATO’s Article 4 to consult allies on collective defence measures.

Lithuanian President Gitanas Nausėda warned Russia over the recent entry of three armed Russian fighter jets into Estonian airspace and a series of incursions along the Eastern part of the NATO alliance countries.

Japanese Prime Minister Shigeru Ishiba has resigned after his party’s election loss. The ruling party must find a new leader to arrest declining voter support and reassure investors.

French Prime Minister Francois Bayrou lost a confidence vote in parliament, prompting his third government change in just over a year and raising doubts about France’s ability to manage its growing debt burden.

Israel launched an unprecedented attack on Qatar, a US ally hosting major military bases, shortly after alerting the White House. The attack, targeting senior Hamas officials, has further complicated efforts to end the Gaza conflict.

Outlook: Bad news is good news, but for how long?

This year’s upside growth surprise is due to tariff hikes occurring more gradually than expected, with the observed US tariff rate only reaching 9.7% in July. This slower rise encouraged the extended front-loading of US goods imports. As a result, there has been strong investment growth despite weak hiring, possibly because companies are investing in new productivity-enhancing technologies to manage inflation costs.

However, as front-loading spending in the US slows, this shift in business productivity will affect labour income. A weakening of labour income will occur just as tariffs squeeze purchasing power, with the effective tariff rate expected to reach 19% by year end. US real labour income is thus projected to decline in the coming months. Although households usually smooth out temporary income fluctuations, the impact could be greater than anticipated. For now, the adage “bad news is good news” is holding true for stocks. Weakening US employment data are broadly seen as paving the way for more Fed rate cuts, which should reduce business costs and encourage another upswing in the economic cycle.

However, inflationary pressures from tariffs and immigration-driven wage increases pose significant risks that could prematurely end the Fed’s rate cut cycle. Additional large and rapid rate cuts should only be necessary if the economy is on the verge of recession.

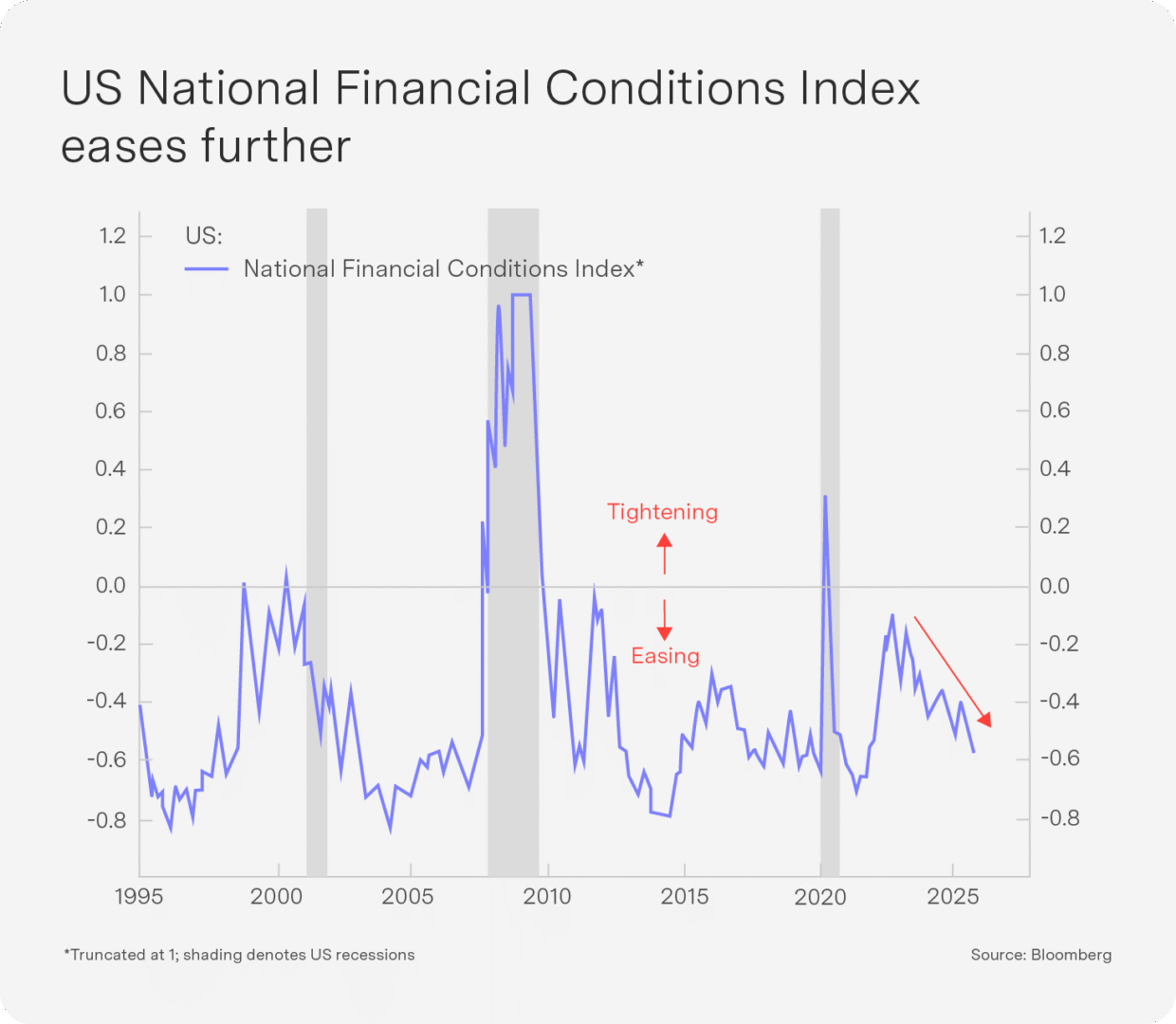

The Atlanta Fed’s GDPNow model is spiking, suggesting GDP growth could reaccelerate to 3.3% in Q3. Similarly, the National Financial Conditions Index is loose and easing (see chart). Cheaper energy, a weaker dollar, lower equity earnings yields and narrowing credit spreads are stimulative for business activity. There are multiple reasons for the Fed not to deliver five additional cuts over the next nine months, but these could be outweighed by political pressure.

Markets are very stretched and pullbacks are likely due to geopolitical risks or inflation. At this stage, however, the Fed continues to provide liquidity, and fiscal stimulus is much stronger than it should be at this point in the economic cycle, suggesting any pullbacks will be shallow.

Key indicators