Sygnals Monthly Bulletin – June 2025

Art of the deal: Trump and the dollar

Global markets showed signs of recovery in May, and the US dollar strengthened following announcements of key trade agreements.

- UK: The US will maintain a 10% baseline tariff on UK exports.

- China: China agreed to cut tariffs on US goods to 10% for 90 days, while the US reduced tariffs on Chinese goods to 30%.

- Middle East: President Trump accepted a luxury Boeing 747-8 aircraft valued at approximately $400 million from Qatar’s royal family, raising constitutional questions.

- European Union (EU): The stakes have risen in the EU, with Trump stating that decisions were “going nowhere” and threatening 50% tariffs from 1 June. After a call with Ursula von der Leyen this was delayed until 9 July.

- Japan: Japan is also pushing for a more comprehensive deal, seeking the complete removal of the 25% tariff on Japanese car imports.

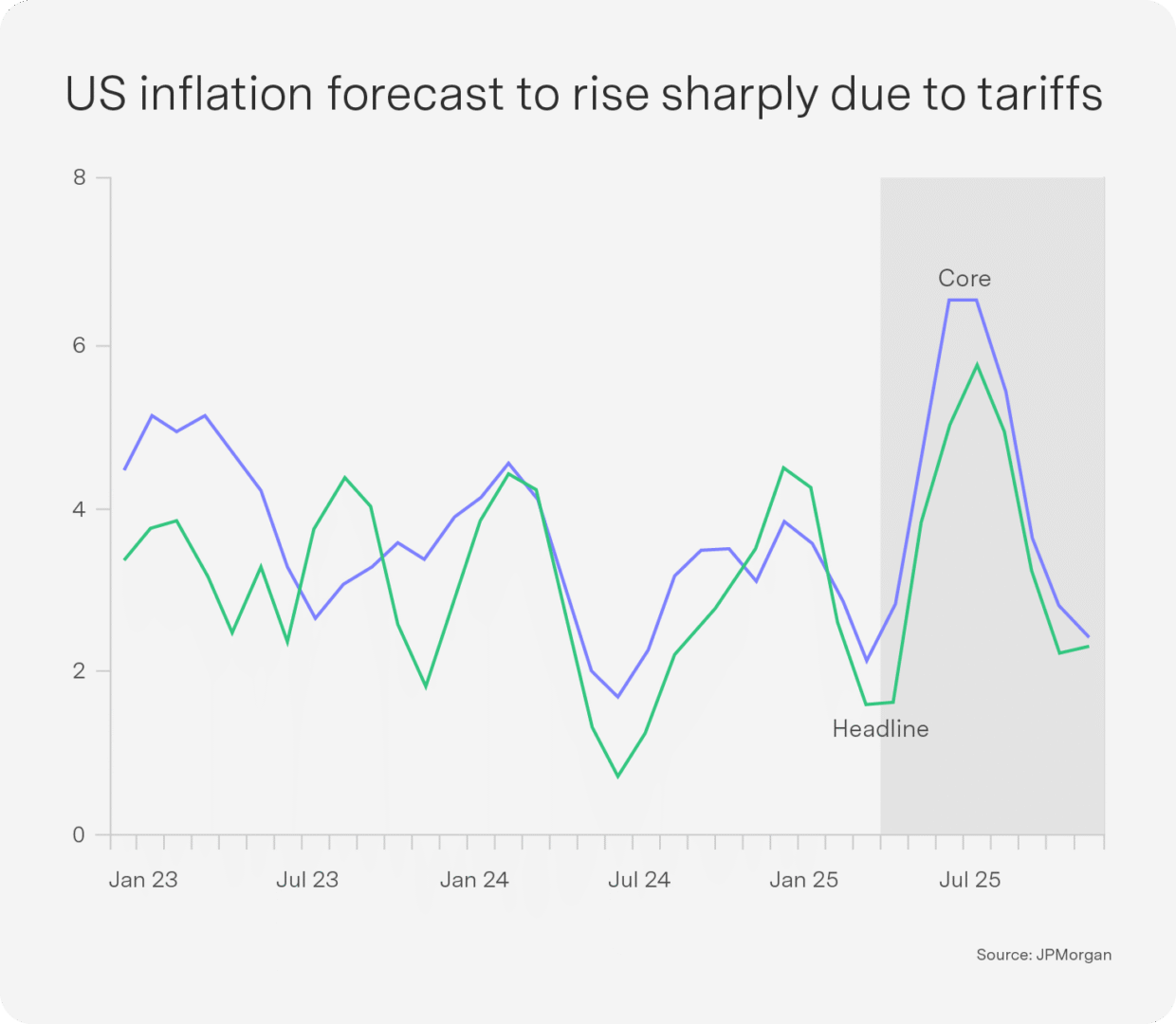

Even with the temporary tariff pause between the US and China and excluding EU tariffs of 50%, the average effective US tariff rate stands at about 13%. JPMorgan forecasts that core inflation (CPI) could rise to 7% in the coming months.

Tariffs alone are insufficient to revive US manufacturing, which now accounts for less than 10% of GDP and offers wages below the national average. A weaker US dollar would be an easier path, as it would make the US more competitive, reduce the trade deficit and stimulate growth. Bessent supports a stronger dollar but has criticised other countries for artificially weakening their currencies. There have been rumours of a Mar-a-Lago Accord, under which Trump would endorse a weaker dollar.

Moody’s joined Fitch (2023) and S&P (2011) in lowering the US from its top triple-A status. The downgrade cited declining fiscal metrics despite economic strengths. Part of the fiscal concern is Trump’s “big, beautiful” tax bill, estimated to add $3.8 trillion to public debt over the next decade. Unlike the 2011 S&P downgrade, which led investors to flock to US Treasuries and supported stocks and lowered bond yields, the current environment has seen a weakening dollar and rising bond yields.

Rising inflation, falling growth, aggressive fiscal policy and credit downgrades have pushed bond yields higher and weakened the dollar. While Trump may not explicitly (or even secretly) want a weaker dollar, his actions are creating one.

Budget 3.0: Here we go again

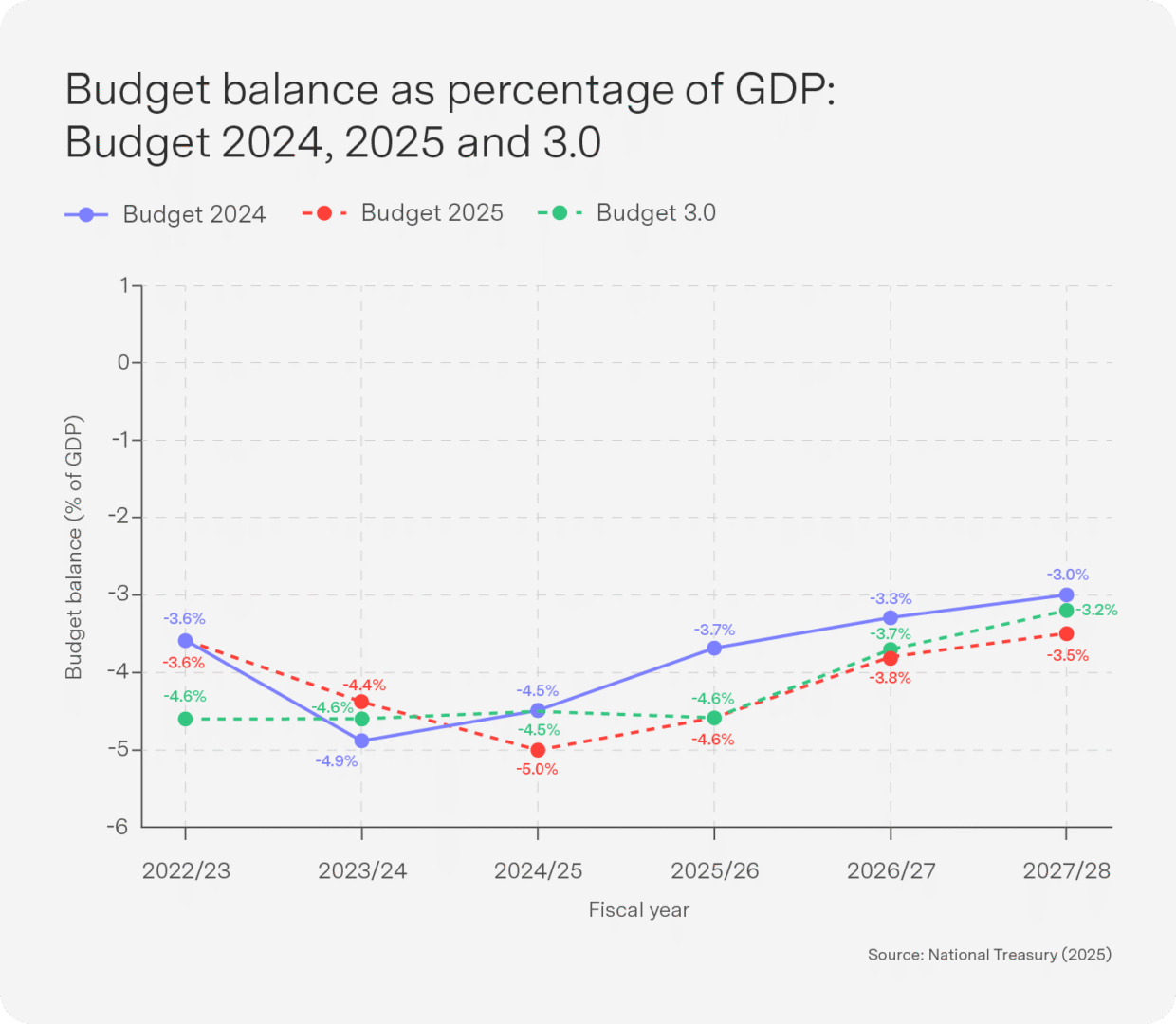

It feels like this has been a Budget year, not a Budget month! So here we are, trying to decipher how the Minister has dealt with the scrapping of the VAT increase after the two previous proposed hikes were roundly rejected by the Government of National Unity – including ANC MPs. In my view, however, the more important driver of these new budget figures has been the downward revision of our economic growth estimates for 2025–2026. National Treasury has projected a GDP growth rate of 1.4% in Budget 3.0 – a significant reduction from the 1.9% in the original Budget.

This material change, a whopping 26% reduction in the expected growth rate for 2025, inevitably translates into reduced revenues and rising debt levels – assuming no material changes in expenditure. The true driver of the changes in our revised Budget has actually been the deteriorating economic outlook. This is of course manifest in the new global norm of higher tariffs and the promise of price pressures and tighter monetary policy, which have conspired to reduce global and regional economic growth estimates. So how did Budget 3.0 respond to this changing environment?

Firstly, and perhaps not sufficiently appreciated in the press, there is actually a slightly improved outlook for the budget deficit. Not only has the primary surplus been maintained, but the Medium Term Expenditure Framework (MTEF) projects a slightly better deficit-to-GDP ratio in the outer years: 3.7% and 3.2% compared to 3.8% and 3.5% in the original Budget. However, the real casualty of lower growth estimates has been South Africa’s debt-to-GDP profile over the next decade. While more extensive expenditure cuts would have mitigated this impact, either political will or timing has prevented the expenditure cuts at the scale necessary to seriously reduce our debt-to-GDP ratios. As shown below, South Africa’s debt-to-GDP levels are now projected to be higher than reported in March. For this fiscal year, debt levels are projected to be 1.2 percentage points higher, increasing from 76.2 to 77.4%. Over the full period, the cost of lower economic growth will on average increase our debt levels by 1.3 percentage points per year. The more subtle point is that the interest on debt payments in South Africa is consistently higher than economic growth rates – the golden macro ratio of (r-g) is unfortunately positive. Our interest burden is outstripping the higher revenues we would get from sufficiently high growth rates. South Africa is effectively in a fiscal trap that is being reinforced by our long-term low-growth malaise.

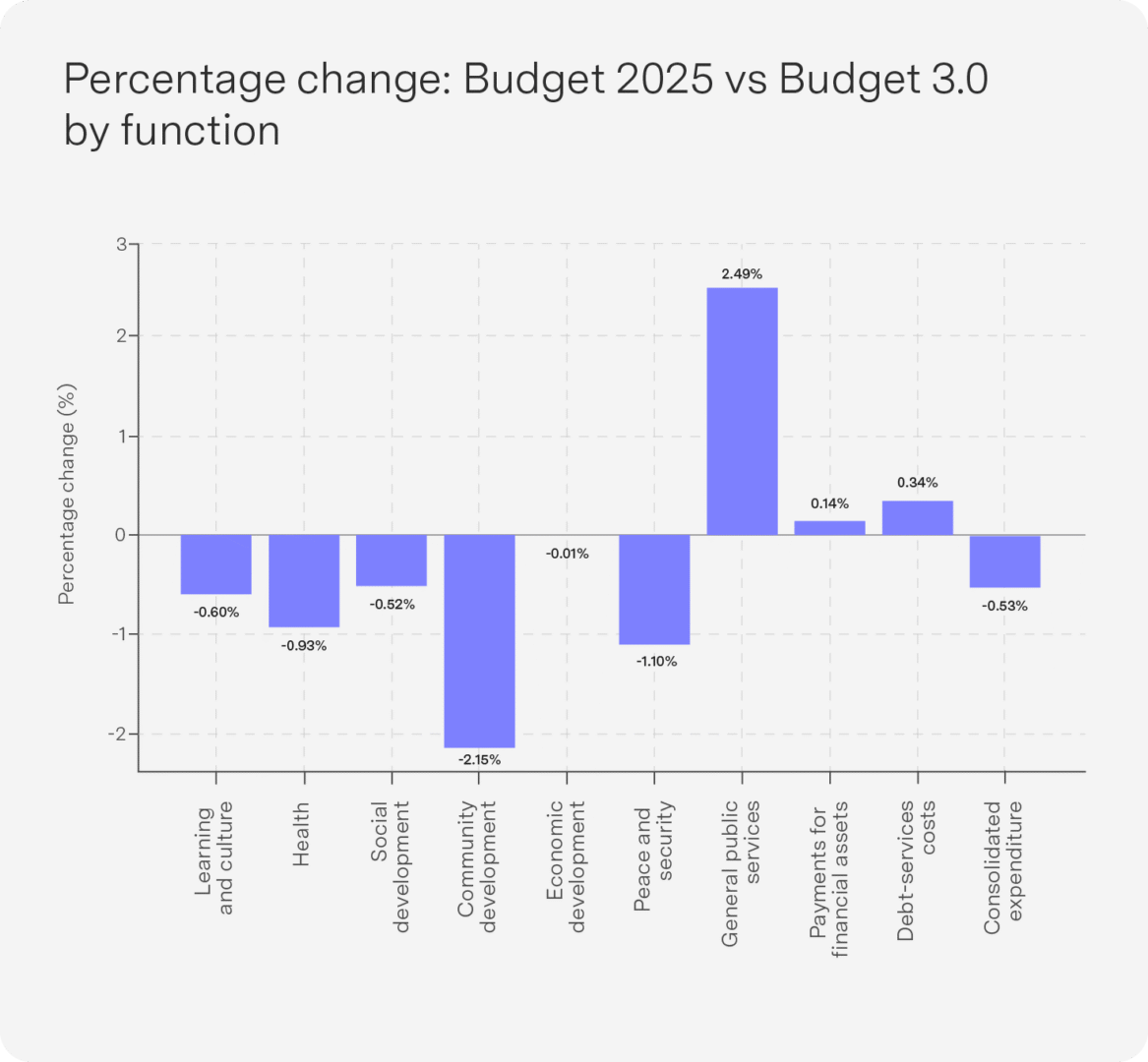

National Treasury has, however, been very aware of the threat of rising debt and interest costs in a low-growth environment, and expenditure cuts have been applied across all line items of the Budget. Consistent with declining cumulative revenue of over R40 billion over the MTEF period, expenditure will contract by at least R75 billion. Expenditure reduction is thus leading revenue reduction, albeit marginally so. Where was the rationing? This mild form of austerity is being applied across the board, affecting health, social development, education and safety and security.

Notably, the additional items included in the original Budget – ranging from early retirement provisions for public sector workers to social grant inflation top-ups and infrastructure – have all contracted in Budget 3.0. The decline in infrastructure spending is a particular concern given that government has starved the economy of much needed capital investment over the last decade. Additional infrastructure allocations fell by close to 30% over the MTEF period.

Apart from the VAT increase, the majority of new revenue proposals revolved around bracket-creep increases in the original Budget. No inflationary adjustments to tax brackets put more individuals each year (at higher inflation-adjusted wages – but same real wages) into higher tax brackets. In Budget 3.0, the net adjustments from revenue proposals have fallen from R28 billion to R18 billion – in part reflecting the removal of the VAT increase. The relief offer in the fuel levy has now also been scrapped, thus increasing pressure on consumers. Also note that the burden of the smaller tax adjustment falls almost completely (86%) on bracket creep. This is the true hidden tax adjustment to raise revenue – arguably far more pervasive in its negative economic effect than the VAT increase. But that is a debate for another day!

Ultimately, then, this unique Budget process has delivered a VAT-free increase while presumably also setting the tone for more deliberate and careful Budget consultations within the GNU for next year. South Africa’s elevated debt profile is now a bit too close to the 80% debt-to-GDP ratio we would like to avoid. It is clear that National Treasury is in no mood to spend liberally, though, as witnessed by the cuts across line departments. The lack of fiscal space for capital spending and a government that yields too much wastage remain two areas for long-term fiscal policy consideration.

Top-performing Sygnia funds

1-month absolute performance as at 29 May 2025

- Sygnia Itrix FANG.AI Actively Managed ETF 7.3%

- Sygnia FANG.AI Equity Fund 7.1%

- Sygnia Divi Index Fund 4.9%

- Sygnia Itrix 4th Industrial Revolution Global Equity Actively Managed ETF 4.0%

- Sygnia Top 40 Index Fund 3.8%

US funds took up the majority of the top positions in May after US markets rallied on the temporary China/US trade deal. Technology stocks led the rebound, pushing the FANG and 4IR funds into the top positions. One local thematic fund made it into the top 5 – the Divi fund, which is a value-oriented fund.

FANG has retained its hold in the top 5 over 12 months, but the big winners over the last year were South African equities and properties. SA stocks continued to do well as commodity prices and China tech rallied and the GNU found some stability.

12-month absolute performance as at 29 May 2025

- Sygnia Itrix Top 40 ETF 29.1%

- Sygnia Listed Property Index Fund 29.0%

- Sygnia Top 40 Index Fund 26.4%

- Sygnia Itrix FANG.AI Actively Managed ETF 22.2%

- Sygnia FANG.AI Equity Fund 22.1%

US: Softening as expected but likely to avoid a recession

April’s US economic data painted a picture of a softening economy:

- Small business optimism declined and retail sales turned negative.

- Factory production fell for the first time in six months.

- The Conference Board’s Leading Economic Index fell sharply, continuing a six-month decline, but has not reached levels that typically signal recession.

- University of Michigan Consumer Sentiment plunged to its second-lowest reading on record.

- Year-ahead inflation expectations surged to 7.3%, the highest level since 1981.

Despite these headwinds, recession fears remain contained. The Conference Board’s confidence index had the biggest monthly gain in four years, driven by the delay in tariff policy. The US fiscal outlook, while unresolved, includes a House plan projecting nearly 1% of GDP in stimulus for 2026, which should provide a growth buffer. The labour market remains resilient for now, with steady employment and moderating wage growth easing inflationary pressures. Fed Chair Jerome Powell’s recent remarks emphasised patience and flexibility, leaving room for rate cuts if economic conditions warrant them.

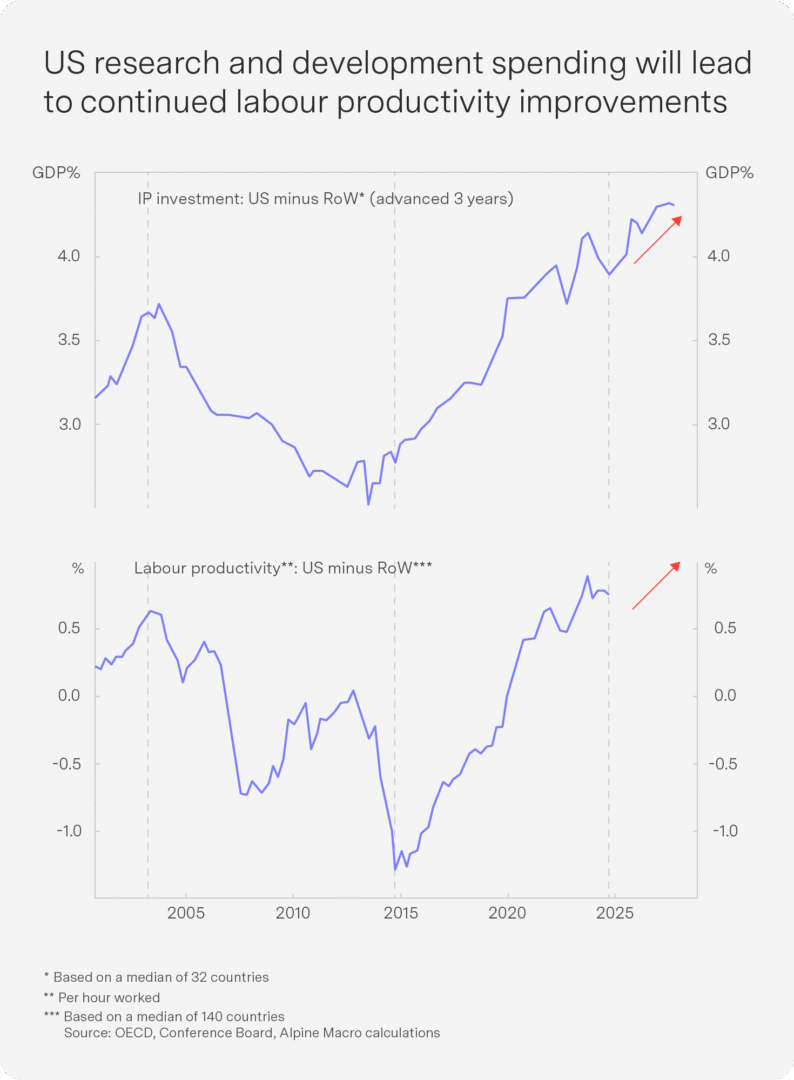

Even if political factors challenge the notion of US economic exceptionalism, corporate America continues to demonstrate exceptional quality. US companies benefit from sustainable growth, strong pricing power and the ability to reinvest cash flows into innovation and expansion. The US leads globally in productivity drivers, particularly intellectual property (IP) investment, which has reached a 30-year peak at over 4% of GDP.

This high IP investment has fuelled research and development and operational efficiencies, underpinning strong labour productivity, which in turn has led to a doubling of corporate profit margins over the past four decades. The concern is whether these companies can grow faster than the dollar weakens, especially if Trump targets them – like the recent 25% tariff on Apple’s iPhones made outside the US. We have gone neutral US for now. Foreign holdings of US equities are now close to double those of treasuries, so if foreigners sell it will further weaken the dollar.

China: Growth recovers under continued government support

China’s economic recovery is gaining traction, supported by proactive government stimulus measures, even as external headwinds from slowing global growth and tariffs weigh on exports. The new export orders purchasing managers’ index (PMI) dropped to 44.7 in April, its lowest level in three years, but key domestic indicators are showing signs of improvement. New credit issuance rose sharply by 28.3% year-on-year in the first four months of 2025, while housing and infrastructure investment also picked up, supporting broader economic activity.

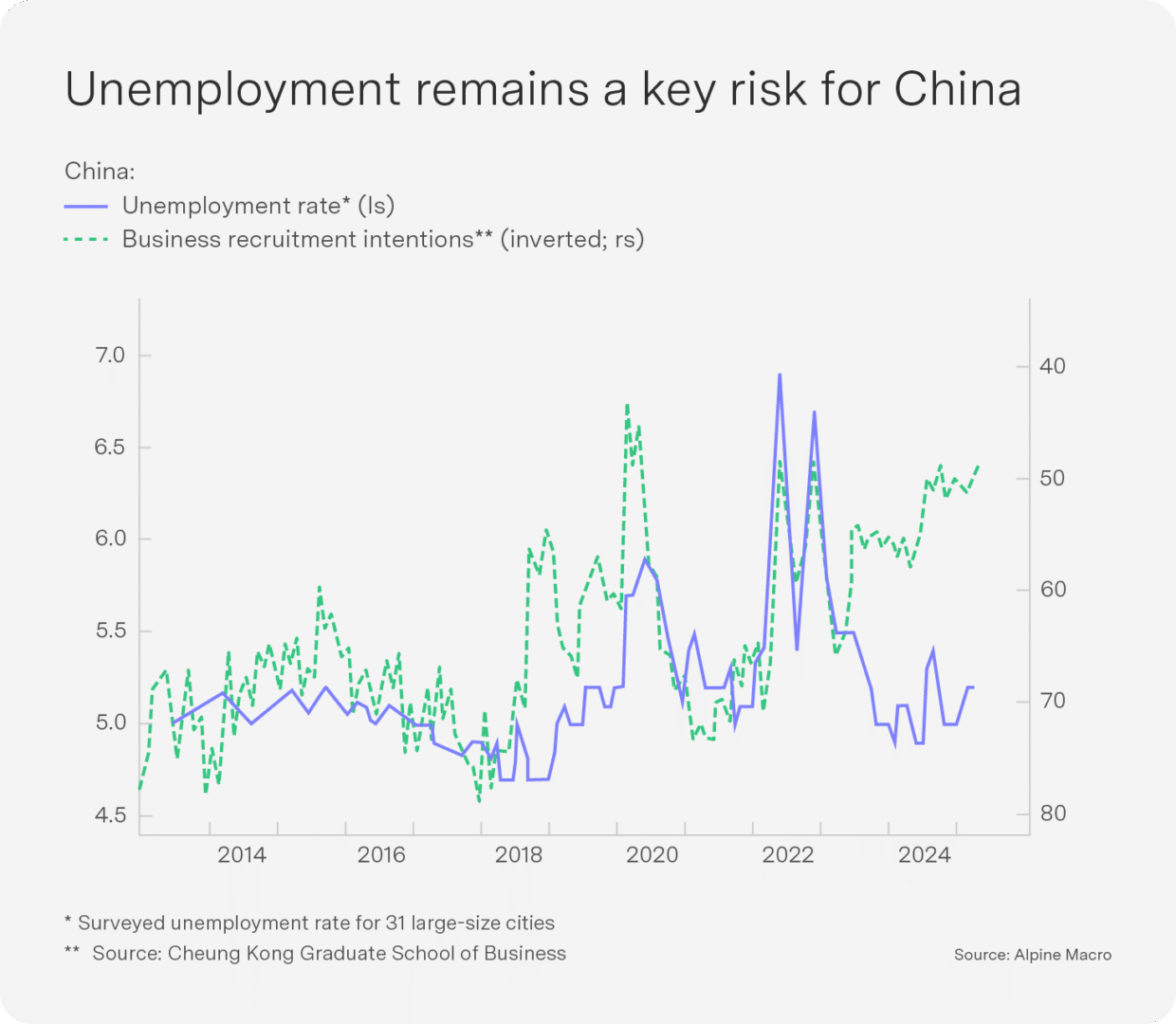

Chinese domestic consumption, which currently accounts for less than 40% of GDP, has significant room to grow. For comparison, domestic consumption represents close to 70% of GDP in the US and over 60% in India. The labour market remains soft, with urban unemployment steady at around 5.1%, posing a potential risk to political stability. This softness is likely to prompt further government stimulus to support employment and social stability. The People’s Bank of China (PBOC) continued to ease monetary policy, delivering a 10-basis-point cut to both the 1-year- and 5-year-loan prime rates – the eighth such cut since October 2024 – and announced a 50-basis-point cut to the required reserve ratio.

We are neutral emerging markets, which are sensitive to global growth, but a weaker dollar, rising commodity prices and momentum in China’s credit and business cycles should provide support.

Oil market update: Low prices help offset tariff inflation

OPEC+ surprised markets by confirming a second consecutive monthly production increase, of 411 000 barrels per day (bpd) for June, as part of a broader plan to raise total production by 2.2 million bpd by November 2026, well ahead of its original schedule.

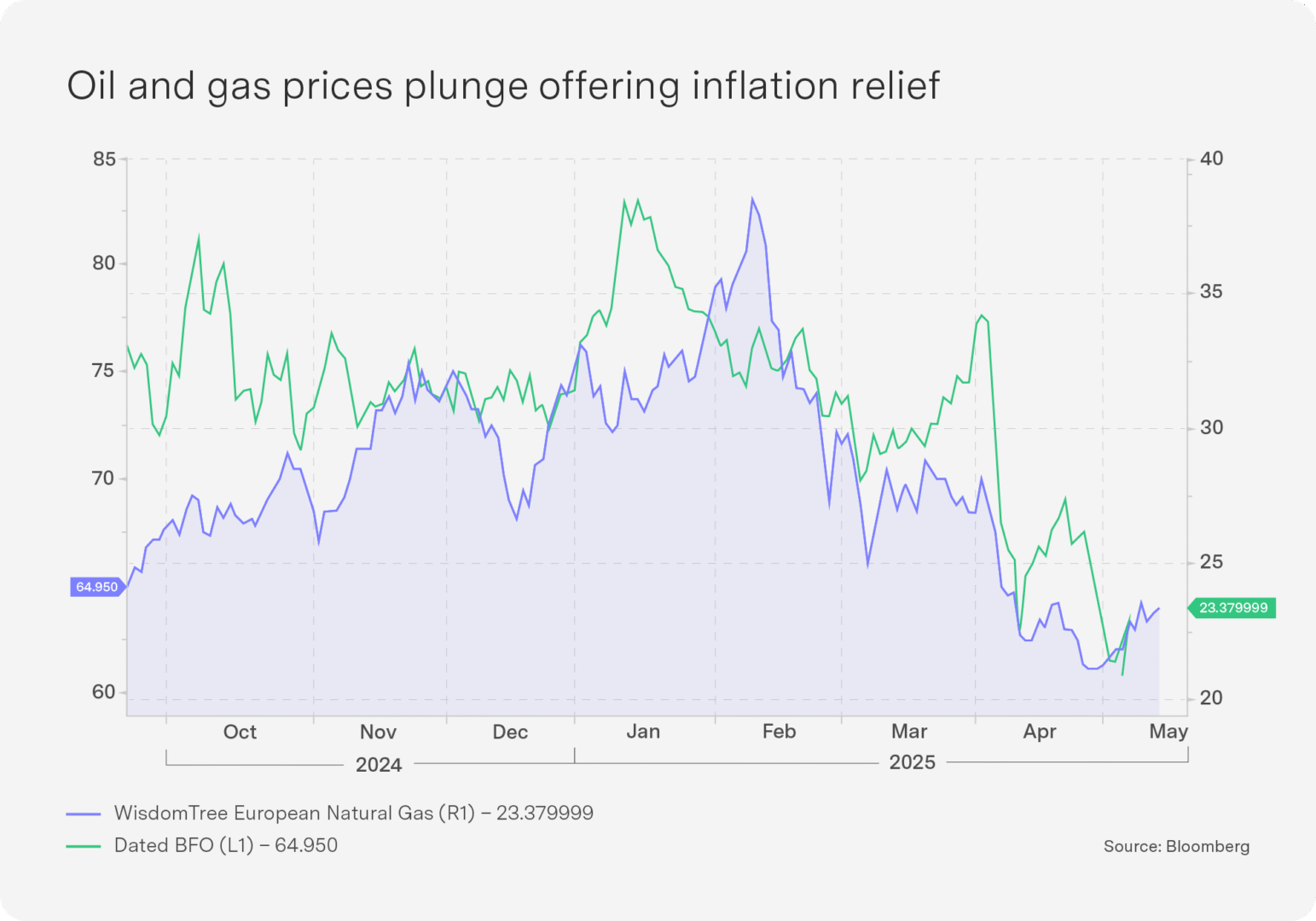

The production boost has deepened the global oil supply surplus, and oil prices have fallen below $60 per barrel, reaching a four-year low in April. Some analysts speculate that these production increases may be influenced by ongoing negotiations with the Trump administration, which has publicly urged OPEC+ to raise output ahead of the US president’s visit to Saudi Arabia.

Lower oil prices have positive ripple effects beyond the energy sector. The strong euro magnified gains from lower energy prices, contributing to a 20% year-to-date drop in oil prices and a 30% decline in natural gas prices across the EU, easing energy cost pressures for the region.

Risks remain, however, as oil prices climbed on a report that Israel is preparing to strike Iran’s nuclear facilities.

Outlook

A US recession now appears unlikely. Goldman Sachs has raised its year-end S&P 500 target to 6 200 and JPMorgan has reduced its US recession probability from 60% to 40%.

- The recent agreement between the US and China to roll back tariffs marks a significant de-escalation in trade tensions.

- Energy prices remain low, supporting consumer and business spending.

- US fiscal support is likely to increase next year.

Uncertainty remains at an all-time high. One day after the US Court of International Trade ruled that President Trump’s “Liberation Day” tariffs were illegal and exceeded his authority, a federal appeals court temporarily reinstated the tariffs. Even if the appeals court ultimately upholds the ruling, the government can still rely on other legal statutes to impose tariffs, maintaining the unsettled status quo. Markets are likely to face headwinds despite growth upgrades:

- The Euro area’s PMI has dropped to a six-month low, signalling slowing economic momentum. Additionally, the implementation of much-needed structural reforms faces material risks due to rising populist political pressures.

- The current US tariff rate of 13.4% represents a substantial drag on trade, with estimates suggesting global GDP could be reduced by 0.5%.

- Downside risks persist, particularly if countries retaliate with a new round of tariffs. The EU tariff announcement on 23 May reminded markets that the tariff threat remains and will be used spontaneously; policy uncertainty remains elevated.

- Growth will slow naturally into the middle of the year as global trade (which was front-loaded ahead of US tariffs) normalises, while heightened uncertainty has caused businesses to slow hiring and investment, which will lead to consumer caution as prices rise.

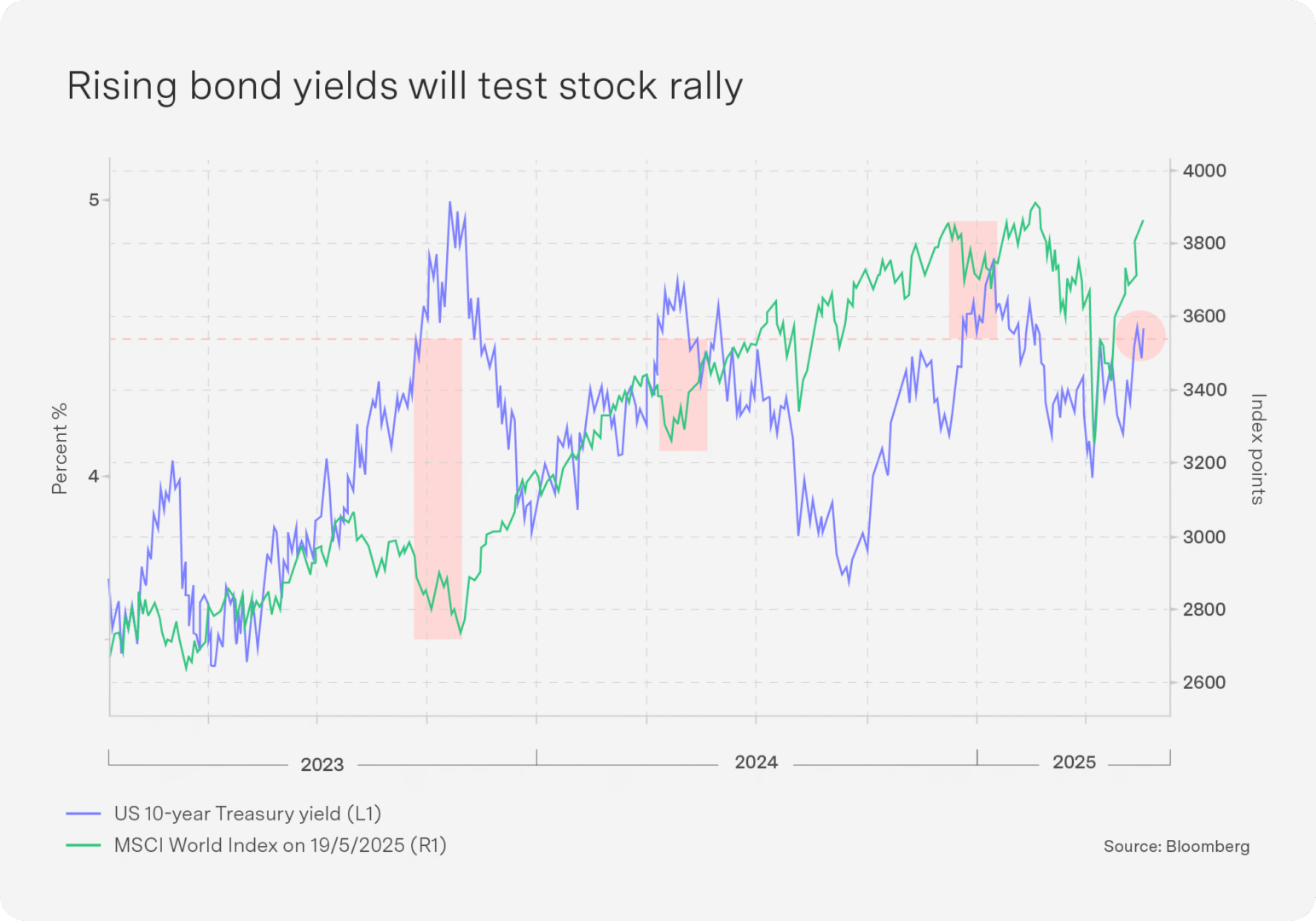

- US CPI is predicted to hit 7% on best-case tariff outlooks, pushing up bond yields. Bond yields are also rising following a US credit downgrade. Rising yields create a challenging environment for stocks, as higher yields affect valuations and investor sentiment. US bond yields at 4.5% have been a pain threshold for stocks in the past two years, and bond yields are now higher than when Trump blinked.

- While turning optimistic earlier in the month on tariff delays, we have again turned cautious.

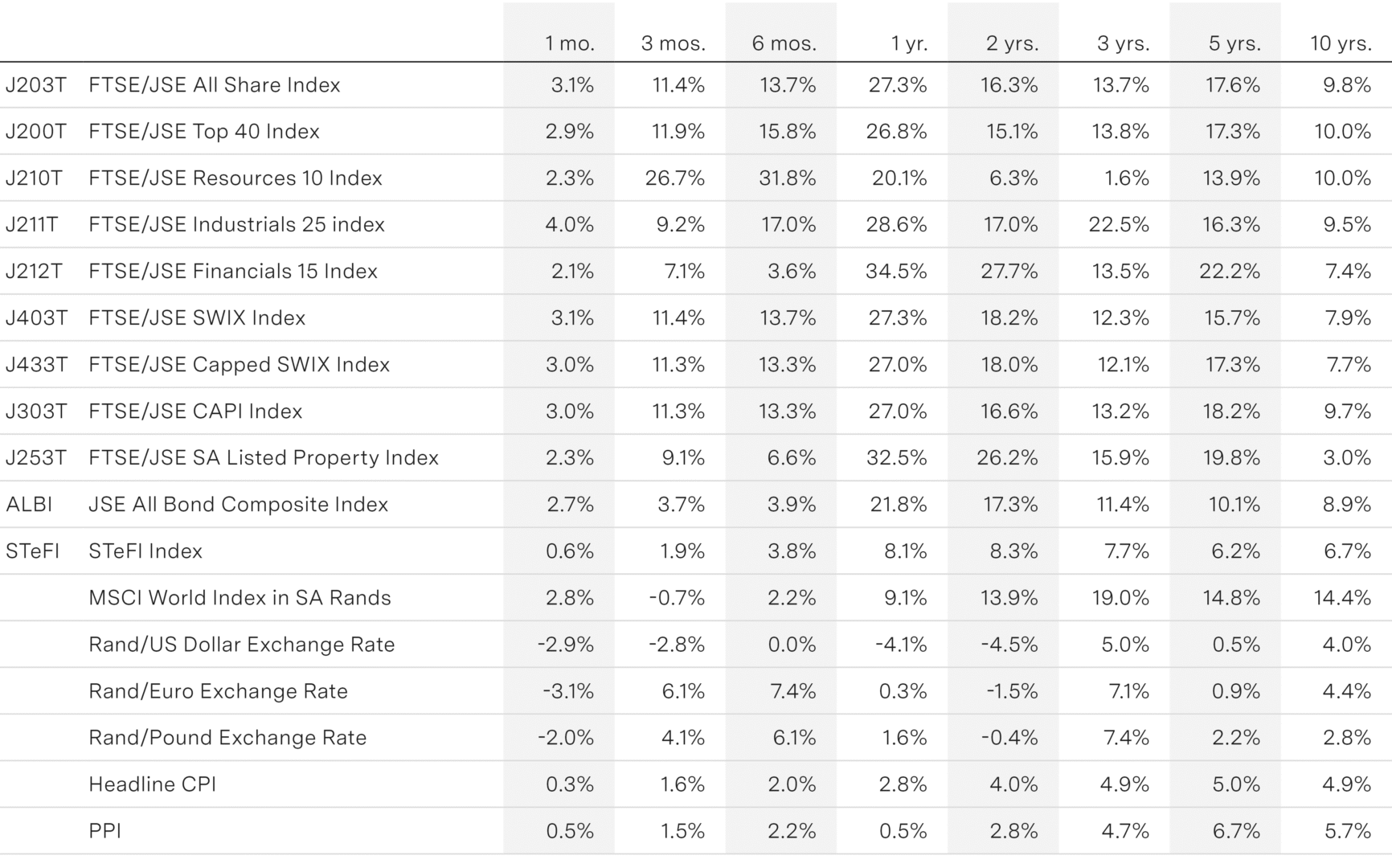

Key indicators