The numbers are in: Tax-free trumps short- and long-term investment switching

Failing to include tax-free investments in your portfolio mix is a huge mistake, writes Wessel Brand, Portfolio Manager at Sygnia Asset Management – and he’s got the numbers to prove it.

Tax-free investments were introduced in South Africa on 1 March 2015, but the take-up of this golden opportunity has been slower than expected – surprisingly, even from market-savvy investors.

My advice to such investors: omit tax-free savings accounts (TFSAs) from your long-term investment portfolio at your peril.

I’ve crunched the numbers, and they don’t lie: investing your total tax-free allocation into a TFSA will deliver between 22 and 42% more growth over a 30-year period than two common non-tax-free investment strategies.

Let’s drill down on those calculations.

The current TFSA limit is R36 000 per annum, to a maximum of R500 000 over an investor’s lifetime. I wanted to compare how investing this maximum tax-free allocation in a TFSA would perform against the same amount invested according to two other investment strategies over the same period (30 years) and using the same baseline assumptions.*

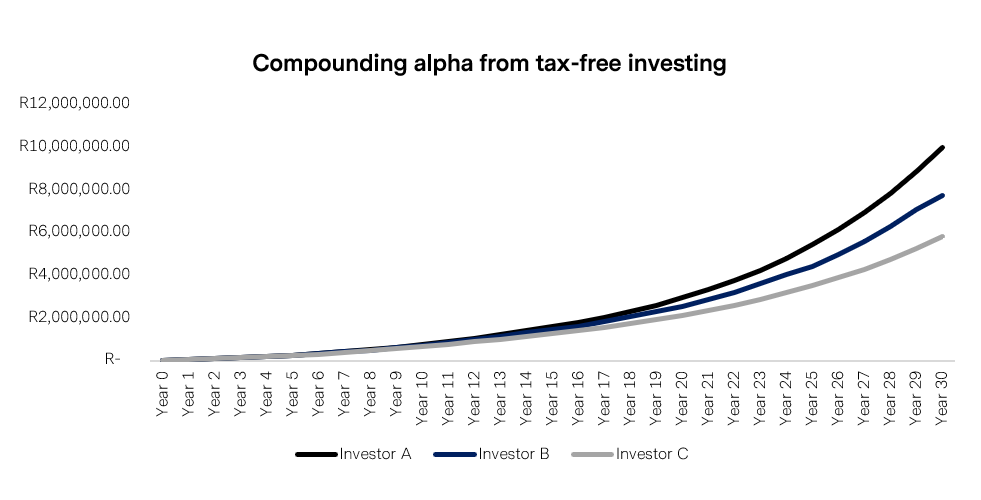

Investor A: TFSA all the way

Investor A is a long-term investor who invests their full annual allocation of R36 000 into a TFSA, hitting the lifetime contribution limit of R500 000 in year 14.

Investor A will never pay taxes on profits when switching between underlying investments in their TFSA and will also never lose out to dividend withholding tax.

Investor B: The market opportunist

Investor B is also a longer-term investor but switches underlying investments once every five years to take advantage of market opportunities.

This results in Investor B having to pay capital gains taxes on their realised gains. Investor B will also be liable for dividend withholding tax (20% on all dividends received).

Investor C: The ditcher-and-switcher

Investor C is an active short-term investor who aims to time the market and pick big winners, switching the allocation of their underlying investments at least once a year.

Investor C must include all realised gains as income in their personal annual income tax submission to the South African Revenue Service (SARS).

For my calculations, I used the lowest tax bracket for a natural person (18%), which comes into effect when a natural person has annual taxable income over R87 300. To be 100% accurate, I included the primary tax rebate for natural persons (R157 14 for the 2022 financial year).

The results

Investor C is an active short-term investor who aims to time the market and pick big winners, switching the allocation of their underlying investments at least once a year.

Investor C must include all realised gains as income in their personal annual income tax submission to the South African Revenue Service (SARS).

For my calculations, I used the lowest tax bracket for a natural person (18%), which comes into effect when a natural person has annual taxable income over R87 300. To be 100% accurate, I included the primary tax rebate for natural persons (R157 14 for the 2022 financial year).